word

advertisement

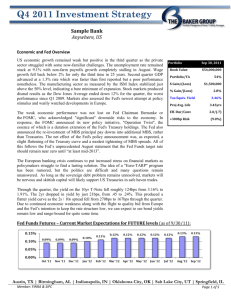

Q4 2013 Investment Strategy Sample Bank Anywhere, US Economic and Fed Overview As we begin the fourth quarter of the year, the US economy continues to maintain a growth pace well below average. Most economists and analysts have lowered their GDP projections for 2013. At this point it will be difficult to meet even a 2% all-in growth rate for the year. Meanwhile, various measures of inflation also remain weak, sitting at levels well below the Fed’s 2% target. Importantly, political dysfunction has rendered fiscal policy an unpredictable negative for the economic outlook. This makes the Fed’s job even tougher as they try to maintain an appropriate monetary policy. The FOMC decision in September to delay the “tapering” of asset purchases was unexpected by financial markets. Chairman Bernanke emphasized that the Fed’s intentions have always been conditional, guided by economic data and an outlook that is subject to change. Still, the Fed has struggled with clarity in communicating their policy intentions, surprising the markets on two separate occasions this year. First with the announcement of their tapering intentions (which many thought would begin in September), and then with the decision to wait. The latter decision was based on concerns about the health of the labor market, the jump in mortgage rates, and restraints on growth from “federal fiscal retrenchment”. Fed members also reinforced the idea that tapering, whenever it occurs, is not tightening. The Fed Funds rate should remain low until 2015, perhaps longer. Portfolio Book Value Portfolio/TA $ Gain/(Loss) % Gain/(Loss) Tax Equiv. Yield Sept 30, 2013 $54,000,000 54% ($459,000) (0.85%) 2.73% Proj Avg. Life 4.80yrs Eff. Dur/Conv 2.71/(0.56) +300bp Risk (10.6%) Bond yields during the quarter were buffeted by the back-and-forth Fed as well as mixed signals about the economy. The 10yr T-Note yield ranged from 2.47% in early July to a high of 3% during the first week of September. Subsequent to the Fed, however, the benchmark yield dropped to 2.61% by the quarter-end. More interesting was the behavior of the 2yr which, after reaching a high of .52% before the FOMC, dropped sharply to .32% by September 30, lower than when the quarter began. The yield curve steepened even further, giving banks a welcome opportunity to boost net interest margin. Going forward, markets are expected to focus more than usual on fiscal policy developments in Washington since those outcomes will weigh heavily on the Fed. New economic data on employment and inflation trends will also play a key role in monetary policy decisions. A new Fed Chairman may soon be in place as well. The likely range for the 10yr yield will be 2.4% - 3% for the remainder of the year. 2014 will produce more conviction for Fed policy if the economy can shift to higher gear, inflation stabilizes or rises, and if fiscal policy prudence returns to Washington. At this time, however, none of those things is certain. Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 1 of 8 Q4 2013 Investment Strategy March 2016 Fed Funds Futures – Current Market Expectations for FUTURE levels (as of 9/30/13): 0.200% 0.100% 0.000% 0.165% 0.180% 0.145% 0.150% 0.125% 0.140% 0.120% 0.115% 0.090% 0.105% 0.100% 0.105% Oct '13 Nov '13 Dec '13 Jan '14 Feb '14 Mar '14 Apr '14 May '14 Jun '14 Jul '14 Aug '14 Sep '14 Current Portfolio Position and Strategy The 3rd quarter saw the 10-year Treasury yield rise as high as 3.0% (+50bp since June 30th) before retracing nearly all of that move and finishing the quarter +12bp. At one point during the quarter, the 10-year was +140bp since May 1st, +160bp from the July 2012 low and at its highest level since July 2011. Those higher market rates have presented both challenges and opportunities to the Bank. On the downside, the rise in market yields caused the value of bond holdings to fall and the portfolio is now at a 0.8% unrealized loss, up from 0.2% at the end of the 2nd quarter. The Bank has worked hard to build a conservative portfolio and resisted the urge to “chase yield” in higher risk assets, so we are confident the drop in the value of our portfolio has been less than what other higher risk portfolios have experienced. One example of this has been the emphasis on higher coupon MBS which have depreciated 1/5th as much as lower coupon MBS in the recent selloff. More importantly, the rise in rates has led to the single largest increase in monthly yields in at least the last 10 years (since we have been tracking monthly portfolio changes). The portfolio yield saw a modest increase to 2.73%. The increase in portfolio yield is primarily due to two reasons: reinvesting cashflows at higher market yields and a slowdown in MBS/CMO prepayments. The Bank’s investment strategy has been focused on building a portfolio of stable cash flow and the higher yields available today are the perfect opportunity to continue deploying some of that cash flow to increase portfolio income and fight margin erosion. Sector Distribution CMO, 8% MBS/ CMO FL, 7% Other, 3% Agency, 13% Muni, 30% MBS, 35% Tax Muni, 4% One negative effect of rising yields is an extension of average life and duration. As less callable agencies are called and fewer homeowners are projected to refinance their mortgages, the portfolio’s average life extended another 0.2yrs to 4.8yrs. Duration has also extended to an above neutral 2.7, the highest duration since the fall of 2008. Just as the Bank had to work hard to keep portfolio duration from contracting too much when rates were at a record low, the Bank must now work hard to keep the duration from extending too much as rates rise. For this reason, the current strategy will be to reduce duration toward neutral from its current above neutral position. The 140bp rise in the 10-year Treasury yield from May to September is a “real world rate shock” and the Bank will evaluate the portfolio’s performance to determine what worked and what didn’t. If the cashflow or price volatility of the portfolio (or a particular sector) was greater than anticipated or outside of tolerance levels, the Bank will use any yield retracements to make adjustments. Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 2 of 8 Q4 2013 Investment Strategy March 2016 The Bank will continue to build a cash flow barbell with a short-to-intermediate range ladder of taxables combined with longer maturity tax-exempt municipals. In order to achieve the goal of reducing portfolio duration towards neutral, the Bank will increase its allocation of shorter duration options including higher coupon MBS, high cash flow CMOs, Hybrid ARMs, floaters and shorter 1X callable agencies. Despite the desire to reduce duration to neutral, the relative value in longer municipals is the best it’s been in years and the Bank will look for opportunities to add longer municipals to increase and stabilize portfolio yield. Portfolio allocations will continue to be managed based on anticipated needs for liquidity, cash flow and earnings. With an understanding that the worst bonds are normally purchased at peaks and troughs in interest rates, security selection has never been more critical and the Bank will avoid high risk securities. Purchase decisions will be focused on structure, credit, loan attributes, cash flow volatility, price risk and optimal relative value between and among sectors. Historical U.S. Treasury Yield Curves 3.8% 3.3% 2.8% 2.3% 1.8% 1.3% 12/31/2012 3/31/2013 6/30/2013 0.8% 9/30/2013 0.3% -0.3% Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 3 of 8 Q4 2013 Investment Strategy March 2016 Sector Strategies Agencies The agency yield curve steepened relative to the treasury curve in Q3, with spreads tightening on the short end and widening in the intermediate and long end. 2-year bullet agencies are +3 basis points to treasuries and 5-years are +25 basis points. The Bank will continue to moderate sector duration by primarily purchasing securities with 3- to 7-year maturities. Favored structures will continue to be premium one-time callable securities with at least one year of call protection. The bank will continue to purchase deeply discounted callables that offer decent spread to bullets to maturity and significant yield kicks if called. Stepups with 1x-call, 1x-step structures will also be utilized when the step coupon provides sufficient probability of call. The Bank will also look to add multi-step structures with mid-term maturities when the step coupon schedule provides ample cushion and the yield pickups warrant. The Bank will avoid chasing yield in the form of long-maturity step-ups in favor of shorter maturity 1x-step and 1xcallable bonds with higher back-end coupons. The Bank will continue to look for opportunities to sell short maturities and deploy the proceeds on the intermediate portion of the curve. In general, the Bank will look to take advantage of market fluctuations by adding slightly longer duration instruments (discounted callables and intermediate-maturity bullets) when rates rise, and focusing on premium 1xcalls in the lower part of the trading range. Agency % Curr/Last Target 13%/13% 10-25% Eff. Duration / Convexity Curr/Last Target 2.9/(0.8) 2.6/(0.9) 1.5-2.5 /(0.5)(1.0) CDs The bank’s CD sector remains quite small. With the agency yield curve and spreads to treasuries changing rather dramatically over short time periods, it is important for the bank to focus on buying only CDs that offer significant spreads to bullet agencies. Which currently will have the bank focusing on CDs with 1- to 7-year maturities. The Bank will buy only marketable FDIC-insured CDs, where it can expect to pick up 15-45 bps to bullet agencies in the desired maturity range. Like agencies, the Bank will avoid longer-maturity, option-heavy structures. FDIC insurance covers up to $250,000 per issuer, including accrued interest. The bank will limit holdings of CDs under these constraints per issuer. The supply of unique issuers remains limited, so the Bank will look to take advantage quickly when new opportunities arise. Municipals Municipals continued to be attractive to investors during the third quarter as demand outpaced issuance. During the end of the third quarter, municipals were under pressure from mutual fund redemptions and the treasury sell off. The Bank will deploy funds in the 7 to 15 year range taking advantage of the market sell off. As a percentage of treasuries, municipals continue to be 90 to 120% along the curve. The historical percentage has been around 75 to 80%. The Bank has made an extensive effort to analyze and monitor the credit metrics of all municipal holdings and will be diligent in reviewing the creditworthiness of all future purchases. Given prudent credit analysis, the environment continues to offer excellent opportunities to add to the Municipal sector. As the Bank continues to CD % Curr/Last Target 2%/2% 0-5% Eff. Duration / Convexity Curr/Last Target 1.3/(0.3) 1.3/(0.3) 1.52.5/(0.5)(1.0) Municipal % Curr/Last Target 30%/29% 25-35% Eff. Duration / Convexity Curr/Last Target 3.6/(0.3) 3.6/(0.3) 3.5-4.0/0-(0.5) Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 4 of 8 Q4 2013 Investment Strategy March 2016 employ a barbell strategy, the Bank will maximize longer municipal holdings and explore opportunities to swap out of shorter maturities and deploy the proceeds out on the preferred range of the curve. The Bank will continue to buy general obligation municipals and will purchase essential-purpose revenue municipals with a minimum of 1.25x coverage and preferring a 1.5x or higher coverage. The Bank will also purchase taxables with 510 year maturities, preferring shorter maturities because they do not have the same reduced duration benefit as the tax-free issues. The Bank will carefully review the creditworthiness of all municipal issuers in addition to assessing the strength of the bond insurer. Preferred insurers of municipal holdings will be the Texas PSF, State Aid Withholding, Qualified School Bond Funds, and issues rated A or better on their own. The Bank will purchase municipals with AGM, Assured Guaranty or Build America Mutual insurance that have an A or better underlying rating. MBS The mortgage market experienced a great deal of volatility over the 3rd quarter of 2013. Optimistic forecasts from the Fed, coupled with “transparent” statements by Federal Reserve Chairman Bernanke indicating that any reduction of QE3 would be data dependent, led the market to believe a taper of purchases may occur as early as the September FOMC meeting. The fallout was a bond market that reacted violently, pushing 30 Year mortgage rates from under 3.5% on May 1st to a 2 year high of 4.7% in early September. However, Chairman Bernanke and committee surprised the market at the September 18th meeting by letting the nation know the Federal Reserve would not taper purchases and continue to execute open-ended quantitative easing measures (QE3) in full by investing $40 Billion per month in Treasury and agency MBS securities, while also continuing to reinvest portfolio cash flows ($5Billion per month) into the MBS sector. Mortgage rates subsequently rallied 40bp to stand at 4.3%. The overall 100bp rise in mortgage rates is beginning to have a dramatic impact to a reduction in prepayments. After peaking at just over 5,200 on May 3rd, the Mortgage Bankers Association refinancing index has dropped over 60% and stands below 1,900. Overall, agency 30-year MBS have slowed 40% from the peak in April 2013and are projected to slow another 30% given current rates and shrinking mortgage capacity. Media reports show large mortgage banking departments laying off mortgage related personnel on a regular basis during the past 60 days. Taxable Municipal % Curr/Last Target 4%/4% 0-10% Eff. Duration / Convexity Curr/Last Target 5.4/(0.1) 5.4/(0.1) 5.0-7.0/0.3-(0.3) MBS % Curr/Prev Target 35%/35% 30-45% Eff. Duration / Convexity Curr/Prev Target 2.2/(0.7) 2.1/(0.9) 1.5-2.0/ (0.7)-(1.3) The HARP 2 program has continued to be very successful in allowing eligible homeowners to take advantage of a tremendous opportunity to obtain an artificially low cost mortgage. The program was originally set to expire at the end of 2013 and will now be in place through Dec 31, 2015. Specifically, borrowers with loans packaged into FNMA or FHLMC MBS experiencing no delinquencies over the past 12 months and an underwater loan (>80LTV) originated before June 1, 2009, have the opportunity to streamline refinance, with very low costs. The program has shown little sign of burning out and the FHFA has launched a marketing campaign focused on borrower awareness to encourage eligible borrowers to take action. In fact, given mortgage rates and fewer overall borrowers having economic benefit from refinancing, many analysts believe HARP Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 5 of 8 Q4 2013 Investment Strategy March 2016 eligible borrowers will be targeted by mortgage bankers and prepayments in this sector may not subside prior to the end of the year. In GNMA space, the FHA streamline program continues to provide incentives to refinance for borrowers with loans also originated prior to June 1, 2009. These pre-June 2009 FHA loans are grandfathered from having to pay the higher current annual Mortgage Insurance Premiums (Grandfathered MIP = 55pb vs. 130-135bp currently) and the upfront premium is only 1 basis point (vs. 1.75% for non-grandfathered loans). The role of the MBS portfolio continues to provide steady front-end cash flow while maximizing risk/reward benefits. The rapid 100 basis point rise in mortgage rates from near record lows observed on May 1st and sustained Fed buying (so far) of MBS reinforces our strategy to balance both contraction and extension risk in all mortgage related investments. During the 3rd quarter, the sector held steady with a 35% allocation and the effective duration extended slightly from 2.1 to 2.2. The Bank continues to review all holdings in the MBS portfolio and will continue to evaluate the benefits of liquidating securities negatively impacted by Government refinance programs or those that underperformed in the back-up in rates. Rate volatility over the past several months reinforces the Banks mantra of striving to hold securities that provide consistent prepay protection while offering more defensive price volatility characteristics. The #1 loan attribute to curtail fast prepayments, and also provide higher base case turnover rates, continues to be pools comprised of lower loan balance mortgages. These loan holders have less economic incentive to refinance into lower rates when they are low but have increased mobility due to smaller loan sizes when rates are higher. To balance extension and prepayment risks, the Bank will continue to focus on shorter-term (<=20yr) and relatively higher coupon (>=3.5%) specified agency MBS pools. 10year MBS pools would be the exception to the coupon parameters, in that the shorter final maturity and high scheduled principal cash flow reduces the need for a higher coupon. Pools will be selected with one or more of the following loan characteristics that should provide prepay protection: 1) low loan balance, 2) investor and vacation properties, 3) NY, TX, NJ, FL geographic concentrations, 4) Higher LTV (>90%), and 5) FHA Loans (GNMAs) originated after June 1, 2009 and prior to April 2011. Although the prepay protection may not be needed if rates continue to rise, the current cost for attaining these attributes has dropped significantly and would be good insurance should the economy falter and we experience a drop in rates. Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 6 of 8 Q4 2013 Investment Strategy March 2016 ARM/Float The Bank reinvested very little cash flow into the ARM sector over the 3rd quarter, resulting in the portfolio allocation falling to just over 6%. As the portfolio duration is approaching the upper end of the Banks target level, the Bank will continue to search for opportunities to enhance future rate sensitivity with minimal yield give up. Since the beginning of 2012, the Bank added newer GNMA 3x1 and 5x1 Hybrid ARMs with 2.0% to 3.5% coupons. Due to record low rates, a very steep yield curve and aggressive refinancing this sector has prepaid faster than anticipated. However, an almost 100bp increase in 5x1 borrowing rates coupled with the increase in FHA Mortgage insurance Premiums should cause prepayments in this sector to decline significantly over the coming months. In this relatively higher rate environment, the Bank will more aggressively search for opportunities in lower coupon (lower premium) FNMA and FHLMC 5x1, 7x1 and 10x1 hybrid ARMS with 2% annual collars. As opportunities present, an additional focus for the sector will be seasoned post-reset ARMS. These loans will have originations prior to 2007 and currently have annual resets of less than 12 months. ARM/Float % Curr / Prev Target 6%/7% 0-10% Eff. Duration / Convexity Current / Prev Target 0.7/(0.6) 0.9 / (0.5) 0.8-1.5/ (0.3)-(0.8) CMO The CMO portfolio continues to spin off measurable cash flow. With little reinvestment of cash flows, the CMO sector allocation has continued to decline and has fallen to below 8% (from 10%) of the total portfolio. As rates have jumped quickly and dramatically, all CMO structures have been reviewed as to potential extension risk and those identified have been targeted for liquidation. The Bank will look to take advantage of higher rates and a steeper yield curve by pursuing CMO structures that have 2-5 year projected average lives with limited extension risk. Additionally, very short average life CMOs (1-2yrs) will be utilized when available to provide a spread to cash alternatives over the next 24-30 months while the Fed keeps short-term rates anchored. To diversify mortgage prepayment exposure and take advantage of the more stable prepayment characteristics, 30 year GNMA MBS (post June1, 2009 origination) will be the preferred CMO collateral. Foremost, FHA loans originated after June 1, 2009 are not eligible to refinance under the FHA HARP program. FHA loans originated prior to April 2011 (and after June 1, 2009) have provided excellent prepayment protection as the FHA has increased the annual Mortgage Insurance Premium by 80bps. The increased premium results in an additional rate incentive needed for an FHA borrower to achieve the required 5% Net Tangible Benefit to refinance. Furthermore, GNMA collateral can offer superior extension protection as base case turnover should remain brisk due to ongoing buyouts of lesser credit FHA borrowers. Preferred FNMA/FHLMC collateral will have underlying loan attributes as stressed in the MBS sector (low loan balance, investor and vacation properties, NY, TX, NJ, FL geographic concentrations, higher LTV MHA loans, etc.) that should provide prepay protection. Additionally, the Bank will begin to search for opportunities in FNMA and FHLMC Commercial mortgage products. These instruments have very stable intermediate cash flows with shorter final maturities CMO % Curr/Prev Target 8%/10% 5-15% Eff. Duration / Convexity Current/Prev Target 2.1/(0.9) 2.0/(0.7) 1.2-2.0/ (0.5)-(1.2) Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 7 of 8 Q4 2013 Investment Strategy March 2016 and could provide and prudent instrument for balancing extension and contraction risks. We continue to see a significant number of CMO securities being liquidated at depressed levels because they have experience a large increase in prepayments as a result of the FNMA/FHLMC HARP II or the FHA Streamline programs. The Bank will evaluate and consider those CMO structures that may have elevated cash flows, but are now trading and much lower premiums and may well be on the cusp of slowing down significantly. All CMO’s will be prudently analyzed and continually monitored for both extension and call risks and will be managed to maximize risk/reward benefits. Austin, TX | Birmingham, AL | Indianapolis, IN | Oklahoma City, OK | Salt Lake City, UT | Springfield, IL Member: FINRA & SIPC Page 8 of 8