CHAPTER V

Chapter 4

APPLICATIONS OF

MONEY-TIME

RELATIONSHIPS

1

Learning Objectives

• To evaluate the economic profitability and liquidity of a single project

• Equivalent measures of a project’s profitability

– Present Worth (PW)

– Future Worth (FW)

– Annual Worth (AW)

– Internal Rate of Return

• Measures of liquidity

– Simple Payback Method

– Discounted Payback Method

2

M

inimum

A

ttractive

R

ate of

R

eturn

• Firms will set a minimum interest rate that all projects should earn it in order to be considered for funding

• Once established by the firm is termed the Minimum

Attractive Rate of Return (MARR)

• Numerous models exist to aid engineering managers in estimating what this rate should be in a given time period

• Personal Example:

• Assume you want to purchase a new computer

• Assume you have a charge card that carries a 18% per year interest rate.

• If you charge the purchase, YOUR cost of capital is the 18%

3 interest rate

Cost to a Firm

• Firm’s raise capital from the following sources

• Equity – using the owner’s funds (retained earnings, cash on hand) belongs to the owners

• Debt – the firm borrows from outside the firm and pays an interest rate on the borrowed funds

• Once this “cost” is approximated, then, new project MUST return at least the cost of the funds used in the project PLUS some additional percent return

4

Setting the MARR

• First, start with a “safe” investment possibility

• A firm could always invest in a short term CD paying around 4-5% (But investors will expect more than that!)

• The firm should compute it’s current weighted average cost of capital (Assume the weighted average cost of capital (WACC) is 10.25%)

•

Certainly, the MARR must be greater than the firms cost of capital in order to earn a “profit” or “return” that satisfies the owners!

• Thus, some additional “buffer” must be provided to account for risk and uncertainty

5

Opportunity Forgone

• Assume a firm’s MARR = 12% with 2 projects, A and B

• A costs $400,000 with an estimated return of 13%/year

• B cost $100,000 with an estimated return of 14.5%/year

• What if the firm has a budget of say $150,000

• A cannot be funded – not sufficient funds!

• B is funded and earns 14.5% return or more

• A is not funded, hence, the firm looses the OPPORTUNITY to earn 13%

• Changes as the amount of investment capital changes over time

6

Present Worth (PW) Method

1. Compute the present equivalent of the estimated cash flows using the MARR as the interest rate

2. If PW(MARR)

0, then the project is profitable

If PW(MARR) < 0, then the project is not profitable

• Example: Cost/Revenue Estimates

– Initial Investment: $50,000

– Annual Revenues: 20,000

– Annual Operating Costs: 2,500

– Salvage Value @ EOY 5: 10,000

– Study Period: 5 years

– MARR 20% per year

• Draw CFD

7

Solution

• PW(20%) =-50,000 + (20,000 –2,500)(P|A,20%,5) +

10,000(P|F,20%,5)= $6,354.50

• PW = $6,354.50 tells us

– We have recovered our entire $50,000 investment,

– We have earned our desired 20% on this investment,

– We have made a lump sum equivalent profit of

$6,354.50 beyond what was expected (required)

8

Present Worth of Bonds

• Treasury bonds

– Issued by Federal Government

– Full backing of the Government

– 1 year or less; 2-10 year issues; and 10-30 year issues

• State and Municipal Bonds

– Issued by states and local governments

– Generally tax exempt by the Federal Government

– Used to finance state and local projects

• Mortgage Bonds

– Issued by Corporations

– Secured by the firm’s assets

– Money received by the firm is used to fund projects

– Buyers of these bonds are not owners – they are lenders to the

9 firm

Present Worth of A Bond

• For a bond, let

Z = face, or par value

C = redemption or disposal price (usually Z ) r = bond rate (nominal interest) per interest period

N = number of periods before redemption i = bond yield (redemption ) rate per period

V

N

= value (price) of the bond N interest periods prior to redemption -- PW measure of merit

VN = C ( P / F, i%, N ) + rZ ( P / A, i %, N )

• Periodic interest payments to owner = rZ for N periods

• When bond is sold, receive single payment (C), based on the price and the bond yield rate ( i )

10

Present Worth of A Bond-Cont.

• Example

Z = $5,000 (face value) r = 4.5% per year paid semiannually

N = 10 years

• The interest the firm would pay to the current bond holder is rZ=$5000(0.045/2)=$ 112.5 per …

• The bond holder, buys the bond and will receive

$112.50 every … months for the life of the bond

• How much will you consider this bond if you can earn

8%/yr c.q.?

11

Present Worth of A Bond-Cont.

• What is fixed?

– The future interest payments are fixed (rZ)

– The future face value of the bond in fixed (Z)

• What can vary?

– The purchase price such that you earn at least the 8%/yr c.q.

• Draw CFD

• PW (2%) =$112.50 (P/A,4.04%,20) +$5,000

(P/F,2%,40) =$3788

• IF the buyer can buy this bond for $3,788 or less, he/she will earn at least the 8% c.q. rate.

12

Future Worth (FW) Method

• Compute the future equivalent of the estimated cash flows using the MARR as the interest rate

• If FW(MARR) >0, then the project is profitable

• If FW(MARR)<0, then the project is not profitable

• Previous Example – FW Method

• FW(20%) =-50,000(F|P,20%,5)+(20,000-

2,500)(F|A,20%,5)+10,000= $15,813

• Since FW(20%)>0, the project is profitable

13

Section 4.5 Annual Worth (AW) Method

• Popular with some managers who tend to thing in terms of

“$/year, $/months, etc.

• Easily understood-results are reported in $/time period

• AW(i%) = R - E - CR(i%)

(Eqn. 4.4)

R = annual equivalent revenues

E = annual equivalent expenses

CR = annual equivalent capital recovery cost

• CR is the equivalent uniform annual cost of capital invested

• CR(i%) = I (A/P,i%,N) - S (A/F,i%,N) (Eqn. 4-5)

– CR(20%) = $50,000(A|P,20%,5) - $10,000(A|F,20%,5)= $15,376

– AW(20%) = R – E – CR(20%), or

– AW(20%) = $20,000 - $2,500 - $15,376 = $2,124

• Since AW(20%)

0, project is profitable 14

Equivalent Worth Methods

• Note: PW, FW, and AW are equivalent measures of profitability

• If PW>0, then FW>0 and AW>0

• From our example,

PW = $6,354.50 therefore,

FW = 6,354.50(F|P, 20%,5) = $15,812 and

AW = 6,354.50(A|P, 20%,5) = $2125

15

Section 4.6 Effect of Compounding

• Benjamin Franklin, according to the American Bankers

Association, left $5,000 to the residents of Boston in 1791, with the understanding that it should be allowed to accumulate for a hundred years. By 1891 the $5,000 had grown to $322,000. A school was built, and $92,000 was set aside for a second hundred years of growth. In 1960, this second century fund had reached

$1,400,000. As Franklin put it, in anticipation: "Money makes money and the money that money makes, makes more money."

• Question: What average interest rate per year was earned from

1791 to 1891?

• Given: P = $5,000, n = 100, F = $322,000 , Find: i'% per year

• F = P(F|P, i'%, 100) or $322,000 = $5000(F|P, i'%, 100)

• F = P(1+i') n or 64.4 = (1+i') 100 or i' = 4.25% per year

16

Section 4.6 IRR Method

• The Internal Rate of Return (IRR) method solves for the interest rate that equates the equivalent worth of a project's cash outflows (expenditures) to the equivalent worth of cash inflows (receipts or savings)

• In other words, the IRR is the interest rate that makes the

PW, AW, and FW of a project's estimated cash flows equal to zero, or

PW(i') of cash inflow = PW(i') of cash outflow

• We commonly denote the IRR by i’, and use PW(i' %) =

0, AW(i' %) = 0, or FW(i' %) = 0

• In general, we must solve for i' by trial and error (unless we use an equation solver)

17

Evaluating Projects with the IRR

• Once we know the value of the IRR for a project, we compare it to the MARR to determine whether or not the project is acceptable with respect to profitability

IRR = i'

MARR project is acceptable

IRR = i' < MARR project is unacceptable (reject)

• Difficulties with the IRR Method:

– The IRR Method assumes that recovered funds are reinvested at the IRR rather than the MARR

– Possible multiple IRRs

• Why should you learn the IRR Method?

• The majority of U.S. companies favor the IRR method for evaluating capital investment projects

18

Example Continued – IRR method

• Find i'% such that the PW(i'%) = 0

• 0 = -$50,000 + $17,500(P|A, i'%,5) + $10,000(P|F, i'%,5)

PW (20%) = 6354.50 tells us that i' > 20%

PW (25%) = 339.75 > 0, tells us that i'% > 25%

PW (30%) = -4,684.24 < 0, tells us that i'% < 30%

25% < i' < 30%

• Use linear interpolation to estimate i'%

• i' =25.3%>MARR

19

IRR – Installment Financing Example

• An individual approaches the Loan Shark Agency for $1,000 to be repaid in 24 monthly installments. The agency advertises an interest rate of 1.5% per month. They proceed to calculate a monthly payment in the following manner:

Amount you leave with

Credit investigation

$1,000

25

Credit risk insurance

Total

5

$1,030

Interest:

Total owed:

($1,030)(24)(0.015) = $371

$1,030 + ... = ...

Payment: $1,401/24 = $58.50 per month

• What effective annual interest rate is the individual paying?

20

IRR – Installment Financing Example

• Step 2 – Solve for i'

• PW(inflows @ i' %) - PW(outflows @ i' %) = 0

• $58.50 (P/A, i' %,24) - $1,000 = 0 or (P/A, i' %,24) =

17.0940

• From table … < i' < ...

• Using linear interpolation, we find that i' = … per month

• From equation 3-3 with r/M = 0.0292, the effective annual interest rate being charged is (1.0292) 12 - 1 =

0.4125 or 41.25% per year

21

Section 4.6 Installment Financing

• In 1555 King Henry VIII borrowed money from his bankers on the condition that he pay 5% of the loan every 3 months, until a total of 40 payments were made.

Then the loan would be considered repaid. What effective annual interest did King Henry pay?

• Solution:

• … = … (P/A,i'%,40); therefore, (P/A,i'%,40) = 20, or i'

= 3.94% per quarter

• i/yr. = (1.0394) 4 - 1

0.1672 (or 16.72%)

22

Section 4.6 Installment Financing

• $7,500 loan repaid in 24 monthly payments of $350 each

• Step 1: Draw a CFD

• Step 2: Find i'/month that establishes equivalence between cash outflows and cash inflows

0 =-$7,500 + $350 (P/A,i',24 months), i'

0.93% /month

• Step 3: Find i' per year, i'/year = (1.0093) 12 - 1 12%=…

23

Section 4.8 Measures of Liquidity

• Simple Payback Period - how many years it takes to recover the investment (ignoring the time value of money)

• Discounted Payback Period - how many years it takes to recover the investment (including the time value of money)

• Previous Example

EOY Simple Payback Cumulative PW(0%) Discounted Payback Cumulative PW(20%)

-----------------------------------------------------------------------------------

0 -$50,000 -$50,000

1

2

3

4

5

-32,500

-15,000

+2,500

+20,000

+47,500

PBP= 3 years

-35,417

-23,264

-13,137

-4,697

+6,354.50

PBP= 5 years

Discounted Payback:

@k=1, PW = -50,000 + 17,500(P|F, 20%, 1) = -35,417

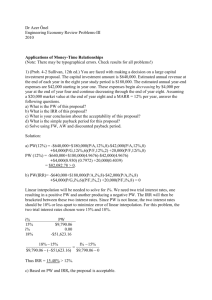

Example: Problem 4-5 (page 178)

Investment $40,000

Annual Expenses

Annual Revenues (next year)

$3,000 decreasing by $500/year thereafter to Yr.10 $10,000

Study Period 5 years

Market Value @ Yr. 5 $15,000

MARR (per Year) 12%

•

Use the PW, FW, AW, and PBP method to evaluate this investment

PW(12%)= -$40,000 + $7,000 (P/A,12%,5) - $500(P/G,12%,5) - 15,000

(P/F,12%,5)= -$9455 < 0 Reject

FW(12%)= -$40,000 (F/P,12%,5) + $7,000 (F/A,12%,5) - $500

(A/G,12%,5)(F/A,12%,5)+ $15,000= -$16,660 < 0 Reject

AW(i%) = R - E - CR(i%) where CR(i%) = I (A/P,i%,N) - S (A/F,i%,N)

25

Solution: Problem 4-5 (page 178)

• PW(12%)= -$40,000 + $7,000 (P/A,12%,5) -

$500(P/G,12%,5) - 15,000 (P/F,12%,5)= -$9455 < 0

FW(12%)= -$40,000 (F/P,12%,5) + $7,000 (F/A,12%,5)

- $500 (A/G,12%,5)(F/A,12%,5)+ $15,000= -$16,660 <0

•

AW(i%) = R - E - CR(i%) where

CR(i%) = I (A/P,i%,N) - S (A/F,i%,N) or

CR(12%) = $40,000 (A/P,12%,5) - $15,000 (A/F,12%,5)

=$8,735

•

AW(12%) = $10,000 - $500(A/G,12%,5) - $3,000 -

$8,735= -$2,620 < 0 Reject

26

Solution: Problem 4-5 (page 178)

EOY Cumulative PW(i=0%) Cumulative PW(i=12%)

0

1

2

3

4

5

-$40,000

-33,000

-26,500

-20,500

-15,000

+5,000

Simple PBP=5

-$40,000

-33,750

-28,568

-24,297

-20,802

-9,454

Discounted PBP>5

27

Payback Method

• Avoid using this method as a primary analysis technique for selection projects

• Does not employ the time value of money (simple)

• If used, can lead to conflicting selections when compared to more technically correct methods like present worth!

• Disregards all cash flows past the payback time period

28