My bullishness is fading along with the Major Trend Index. While we

advertisement

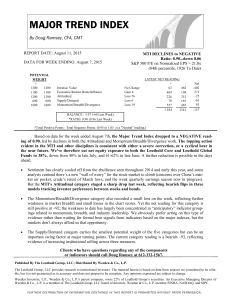

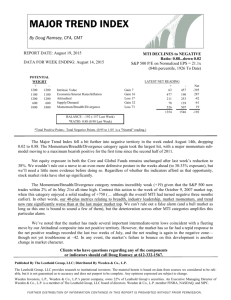

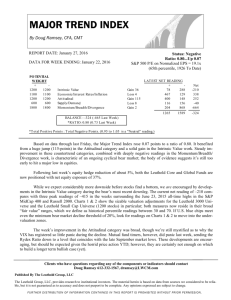

My bullishness is fading along with the Major Trend Index. While we’re both still positive, the contrarian in me has some nagging doubts. Yes, it’s Thermal Pollution Time again. Will 2011 Be Investor Hell or Heaven? My annual predictions for the Economy, U.S. Interest Rates, the Stock Market, and U.S. Inflation. A Look In The Rear View Mirror: I critically review my performance, prognostications and predictions for 2010. All in all, not too bad (but I’d like to revisit those interest rate predictions!) The Vikings hopes for the playoffs have deflated faster than the Metrodome, but you’ll have to wait for my Super Bowl picks! As readers may have noticed, I am now on a rather irregular publication schedule with “View From The North Country.” My commentary frequency is not dictated by the calendar as has been the case since 1969. I now will write when I really have something to say and my guess is this will be about six times a year, more or less. However, my current portfolio management responsibilities will essentially continue to be full time, as well as contributions to the Major Trend Index disciplines. MY BULLISHNESS IS FADING For the U.S. stock market I have been tactically constructive since September when our market disciplines edged back on the Positive side. In the October issue of “View,” my S&P 500 objective in the 4th quarter was 1260, exceeding the April 2010 peak. Smaller caps were expected to outperform as they have. Some readers may recall that a year ago, in the annual crystal ball gazing ritual (which you will find in this issue), I had visualized this year’s peak S&P 500 zone as 1300-1350. From today’s 1230 level, this now seems an improbable longshot even if a strong seasonal Santa Claus rally is in store. Actually, the Santa Claus rally itself may be improbable. 2010’s market has been a hostile year for seasonal biases. In 2010, investors and traders employing seasonal and calendar history in their strategies prove to be mostly out of synch with the market. “Sell in May and Go Away” took you out at a market low while missing out on the strong market recovery that kicked off in August. At the same time September (the worst performing month) proved to be the best month of the year (+12%). So what about the “Santa Claus Rally?” I give little or no importance to these historical bias’ (unlike CNBC) because other factors like the kind noted on the next page, can be much more significant. Published By The Leuthold Group, LLC December 2010 Vol. 3 No. 9 Distributed By Weeden & Co., L.P. Member FINRA, NASDAQ And SIPC FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. CURRENT FACTORS OF SIGNIFICANCE MAJOR TREND INDEX: I find the recent deterioration in the Major Trend Index somewhat disturbing. After edging back into positive territory in September, the ratio of positives to negatives peaked at 1.36 in late October. The ratio has deteriorated at an accelerated rate in the last three weeks to 1.11, even as the market moved higher. However, this is still a positive reading (above 1.05), and I might add that most of this deterioration occurred in our Attitudinal (sentiment) measures which are now the most negative of our MTI subsets. Investors, professionals and individuals became increasingly bullish in late November and early December (anticipating a year-end Santa Claus rally?). From a contrarian’s standpoint this is not a good sign. THE BLAST OFF THAT WASN’T: On Tuesday, December 7 (Pearl Harbor Day) the market gapped up and exploded on the upside with the news that President Obama was willing to compromise and extend all of the Bush tax rate reductions. This seemed to be viewed by investors as great news. But by the close that day, all the momentary market gains had evaporated regardless of the prospects that tax rates would likely remain at current levels, including capital gains and dividend tax rates. It also appeared that year end selling to take advantage of the current 15% capital gains rate would no longer be a negative factor if the 15% rate were extended through 2011-2012. Immediately the financial media talking heads jumped on the bullish bandwagon, concluding that the December late year market rally was off and running. So why did the market give back all of its initial December 7 gains by the end of Tuesday? It is obvious to me that at least some big time investors and traders viewed this momentary burst of market enthusiasm as a “liquidity opportunity” that Old timers refer to as “distribution,” with stocks moving from strong hands to weak hands. My guess is much of this selling was foreign-based, from Europe and Asia. For many foreign and some big U.S. investors Obama’s compromise was ominous. It meant a large potential revenue loss for the U.S. government combined with a large increase in the outlays proposed. The move in the direction towards U.S. fiscal responsibility seemed to be evaporating. “Let’s hope the Chinese have the money to pay for all this, because we don’t.” -Dale McFeatters, Scripps Howard News Service SURPRISE! INTEREST RATES ARE RISING: It’s not supposed to be this way. The Fed’s new $600 billion print money/buy Treasuries program was activated over a month ago. The 10 year maturity, the important benchmark for U.S. consumer and corporate borrowings was probably the critical target. The Fed’s buy program is a manipulative effort to keep yields low and thus stimulate the U.S. economy. But it does not appear to be working. Back in early October the 10 year’s low yield of 2.33% was recorded, rising to about 2.60% in early November as the Fed’s new program got underway. Subsequently, 10 year yields continued to rise, surging in recent days to a high of 3.33% on December 8 as the Treasury auctioned a new $21 billion load of 10 year bonds. 30 year T bonds, often the benchmark for residential mortgages, have behaved in much the same contrary manner. From a low yield of around 3.55% in August, yields rose to 4% as the new print money/ buy treasuries program got underway. Subsequently yields have move higher, particularly in the last two weeks (now 4.45%). A new $13 billion issue is coming this week. So what’s going on? Why isn’t QEII working to stabilize, or even bring down, rates? In The Wall Street Journal’s Credit Markets column, Min Zang observed the extension of the Bush tax cut sparked alarm about a rise in the budget deficit, as well as probably stimulating the economy and thus driving up the market. But as I see it, it’s more than this. Rates have been rising since the Fed’s buy program began. The Leuthold Group—December 2010 2 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. I think the print money/buy Treasuries program has spooked investors, particularly foreign investors. The U.S. is moving farther along the road to monetary debasement inflation (printing press inflation). Selling pressure from existing Treasury holders may now be overwhelming the Fed’s print and buy efforts. It is the classic case of more sellers than buyers, even though today’s big buyer is being supplied funds by a printing press, I would not be surprised to find sovereign funds now reducing U.S. Treasuries. The Fed’s buying has provided an unexpected “liquidity opportunity.” CONCLUSION Strange things are happening. Democrats in Congress are attacking their leader and his compromise proposal. What was viewed as a done deal, now may be radically altered, sticking the rich with a rise in tax rates, and loading up the legislation with additional spending and more “down home earmarks.” Will the lame duck Congress produce any passable legislation by year end? If not, Santa Claus and his traditional year end market rally will never show up. “THERMAL POLLUTION TIME” Yes, it is thermal pollution time again. It’s soon the new year, the time when prognosticators and investment pundits produce large volumes of hot air, probably contributing to global warming, but not here in frigid Minnesota. The annual ritual, attempting to divine, predict and guess what the new year will bring, is relatively harmless… assuming clients consider it as entertainment rather than investment advice. The only real crystal balls in our business were found prior to 2009 on those elegant bull figurines that once decorated some now defunct firms such as Bear Stearns and Lehman. As I state each year: My predictions are mostly for show, while the coming year’s ongoing portfolio shifts are for dough. The real value of our work is in the mid-course adjustments made as the new year’s conditions warrant. For it is the markets themselves that always seem to provide both unexpected opportunities and unanticipated risks. I should point out that the predictions I make herein are mine and mine alone. They do not represent a group consensus. At one time we presented my New Year’s predictions in a detailed Special Research Study including charts, tables, and graphs. Frankly, it seems to me this may have been much ado about not very much. However, as I reviewed my predictions of a year ago, I was actually on target with some, including a few that were close to bulls-eyes. (See “A Look In The Rearview Mirror.”) The Leuthold Group—December 2010 3 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. 2011… INVESTOR HELL OR HEAVEN? THE ECONOMY IN 2011 I am not an economist, but my economic prognostications were right on the mark in 2007, 2008, 2009, and very close to the mark in 2010 (though unemployment remained higher than expected). Sometimes I think it pays to not be an economist! The current economic expansion that emerged from the doldrums of the second quarter of 2009 should carry well into 2012. I base this on the average duration of historical U.S. economic expansions, 1854 to date (3.5 years). True, the three expansions since 1982 were longer (averaged 7.7 years), but considering today’s political quagmire and massive government liabilities, I think an extended expansion of that length is most unlikely. We may see a couple of 4%+ quarters of GDP real growth in 2011 (perhaps close to 4% in Q4 2010), but economic growth for the entire expansion may average 3%, lagging far behind economic growth in emerging and lesser developed countries, and also lagging (by a lesser margin) overall global economic growth. U.S. employment should continue to grow modestly in 2011. The stubbornly high unemployment rate will turn down as employer confidence improves as government policy becomes less obscure. My current guess is an unemployment rate of 8% by year end 2011. I expect corporate earnings will rise, but not as dramatically as the 2010 earnings recovery. The S&P 500 reported earnings may challenge the $90 mark (my guess is $87), with operating earnings approaching $100 (my guess is $95). Both calculations are expected to exceed previous fourth quarter high water marks of $84.92 (reported) and $91.47 (operating). Profit margins for the S&P Industrials (excludes Financials) are currently historically fat at about 7% (est.). The 55 year median is 5.5%. I expect margins will shrink some in 2011 as employment levels pick up and material costs rise, but only partially passed on. The reality is that the U.S economy is now a mature economy and the possibility of rebuilding this country’s manufacturing base is increasingly remote. While wage differentials with a number of other countries are narrowing or, in some cases, moving to our advantage (Japan, Germany, France), there remains plenty of cheap labor available in frontier and new emerging economies. Yes, we could develop dynamic new industries in the U.S., but in areas such as energy alternatives and clean technology, China is moving ahead of the U.S. “How long can the World’s Biggest Borrower remain the World’s Biggest Power?” -Larry Summers Before he entered government The Leuthold Group—December 2010 4 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. THE U.S. STOCK MARKET IN 2011 Normally with earnings expected to rise, the economy growing and valuations not excessive, 2011 should be a good stock market year. Under normal circumstances my upside target would be 14001450 for the S&P 500. It’s true the S&P 500 is up 81% from the 2009 lows, and this about matches the 83% median gain of the last 17 bull markets (1926 to date). In addition, today’s 81% gain was recorded in only 21 months, while it took the previous 17 bull markets 32 months to post their median 83% gain. Thus, it would seem logical to conclude the current bull market has gone too far too fast. This might be true if the current bull market had not emerged from such an undervalued level. This bull market emerged from the low quartile of our historical PE valuation studies (a very cheap market). Seven of the 17 past bull markets (1926 to date) also emerged from this bottom quartile, posting a median 158% gain over the following 2.7 years. Considering the low valuation existing at the 2009 lows, the current bull market may not have gone too far too fast. BUT THE RISK IS RISING So under normal circumstances I would be optimistic about the stock market outlook for 2011. But instead I am increasingly fearful because of the huge $13 million dollar debt, because the government continues to borrow 30 cents of every dollar it spends, and because our politicians seem incapable of having the courage to address this hugely important issue. It is increasingly possible a major deficit related crisis will occur in 2011, a crisis that may at least temporarily destroy global confidence in the fiscal integrity of the U.S. and the dollar. Those who continue to maintain that a weak dollar is good for the U.S. and for the U.S. stock market may continue to believe the weaker the better. They know not what they wish for. A major global run on the dollar, down 20% or more would, in my view, quickly knock at least 20% off the S&P 500. From current levels, that puts the S&P 500 at 1000 (or worse), with long T-bonds at 7% or higher. Maybe then, with a crisis and a new crop of fiscal realists in Congress, the U.S. will shut down the printing press and make the tough but necessary decisions that are now being made in much of Europe. That is my hope, but I have come to believe it will take a crisis. U.S. INTEREST RATES IN 2011 Yields will be higher a year from now than they are today. If a crisis develops, as discussed in the previous section, yields would be much higher at least temporarily before coming back down. This assumes the U.S. would react by taking meaningful and serious steps to address its towering deficit problem. If we muddle through the year without a crisis, yields are still expected to rise. Recent bond market action seems to indicate the Fed’s efforts to manipulate longer term bond rates is now ineffective. The sellers, be they Sovereign Funds or U.S. and foreign institutions, seem to have overrun the Fed’s efforts to keep yields low. The bond market vigilantes are back, and the Fed, even armed with a printing press, is no match. The Leuthold Group—December 2010 5 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. The following table of my yield projections are more extreme than Jim Floyd’s current “Green Book” estimates. I might add that I have been predicting higher yields for three years (except for Junk), and have been wrong for three years. “Crisis Target” on the table indicates sometime in the next 12 months…..NOT year end 2011 “Crisis Targets” is a conservative estimate and could be higher if corrective action is not taken. Leuthold’s Bond Market Target Yields 90 Day T-Bills 3 Year Treasury 5 Year Treasury 10 Year Treasury 20 Year Treasury 30 Year Treasury Current Yield 0.12% 0.92% 1.85% 3.24% 4.18% 4.45% Twelve Month Non Crisis 1.00% 2.00% 3.25% 4.25% 5.00% 5.00% Crisis Target 5.00% 5.50% 6.00% 7.00% 7.00% 7.00% U.S. Corporates 20 Year Corporate High Yield Bonds 5.60% 8.12% 6.00% 9.00% 7.50% 12.00% U.S. INFLATION IN 2011 I expect both the PPI and CPI inflation to accelerate in the next 12 months. In view of current inflation rates around the world, from China to England, the current 1.2% U.S. CPI inflation and 2.8% PPI inflation seem extraordinarily low. Some might say absurdly low. This is no place to detail the shortcomings of these two measures. I will leave that to Jim Floyd. At any rate, using these measures, here is the 2011 U.S. inflation outlook U.S. CPI up 3.5%. Ben Bernanke you can breathe a sigh of relief. There’s no deflation in sight. U.S. PPI up 5.5%. This measure is misunderstood (see comments in next section). It does not measure what producers are paying for copper, steel, cement, wheat, steel, or lumber. Rather it tracks the wholesalers’ price changes in the finished goods produced. Commodities are on fire, and it’s not just because of the weaker dollar. Less than expected crop production of sugar, cotton and corn are driving up prices. Rising ethanol production is also pushing corn prices up. China’s appetite for raw materials appears to be even stronger than many believed. …..The Leuthold Commodity Diffusion Index now shows 93% of commodities selling at levels above a year ago. Rarely has this inflation gauge been higher in its 36 year history. Other periods when our diffusion index was at an extreme reading of 90%+ (1973-74, 1978, and 2004) were all followed by accelerating inflation. …..Even when measured in a strong currency like the Swiss Franc, this commodity Diffusion Index is above the 90% level (see next page). Commodity prices are signaling significant pass-through inflation pressures building. The Leuthold Group—December 2010 6 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. COMMODITY DIFFUSION INDEX 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% (4 Week Average) NOW 90% ©THE LEUTHOLD GROUP 2010 80 82 People have become conditioned to almost automatically respond to higher commodity prices by saying that it is because of the weak U.S. dollar. That is only partly true. Commodity prices have been inflated by a lower dollar, but the Euro has also been a weak currency, so it should not be a surprise to see the extremely high reading on a Euro-denominated Diffusion Index. In order to minimize the weak currency impact, we created a Diffusion Index denominated in the Swiss Francs, one of the strongest currencies around today. 84 86 88 90 92 94 96 98 00 02 04 06 08 10 120 1.10 1.05 110 1.00 0.95 100 0.90 90 0.85 Swiss Francs per 1 U.S. Dollar (Left Hand Scale) 0.80 0.75 80 0.70 70 0.65 60 0.60 0.55 When the Diffusion Index is denominated in Swiss Francs a currency that has been strong over the past six months (up 18% against dollar), the same picture emerges. Here the Diffusion Index has been rising (to a current level of 93%) despite the stronger currency. 50 0.50 0.45 40 0.40 Leuthold's Commodity Diffusion Index In Swiss Francs (Right Hand Scale) 0.35 0.30 0.25 0.20 Clearly there’s more to the higher prices than just a weak currency. Inflation pressures are accelerating! 0 Dec-08 Jan-09 0.10 The current six month rate of change jumped back from a deflationary reading of –3.9% to a strong inflationary reading of +6.8% at present. However, the twelve month rate of change fell to +18.2% from last month’s +20.2%. PPI Crude Materials For Further Processing 100% Seasonally Adjusted October 2010: 218.0 6 Month Annualized: +6.8% 12 Month: +18.2% 75% 50% 25% 0% -25% -50% -75% Dark Line: 12 Month Rate of Change Light Line: 6 Month Rate of Change The Leuthold Group 2010 -100% 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 October’s biggest monthly increases: Corn +23% Aluminum Scrap +10% The Leuthold Group—December 2010 7 20 10 PPI Crude Materials: October Reading Soars +4.3% The PPI Crude Materials Index had a huge 4.3% gain in October. 30 The Leuthold Group Copyright © 2010 0.15 Sep-10 Oct-10 Nov-10 Dec-10 78 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 76 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 74 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Percent Of Components Higher Than Year Ago Last Now Issue Subsets: Grains (14 components) 93% 79% Foods (17 components) 82% 89% Fats & Oils (6 components) 100% 100% Fibers (2 components) 100% 100% Metals (7 components) 100% 86% Energy (16 components) 100% 94% Misc. (9 components) 100% 100% Soybeans +11% Waste Paper +9% View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. A LOOK IN THE REARVIEW MIRROR For the last 30 years, I have made it a year end ritual to critically review my previous year end predictions to see where I was right and where I was wrong. Years ago, I was probably the only institutional strategist publishing this kind of critical retrospective. But today a few other strategists and financial writers now also publicly review their failures as well as successes. This includes Byron Wien and some columnists at Barron’s. Too often we remember our successes but forget our failures. For years I have felt this kind of critical reexamination is good for the soul if not always for the ego. As a bonus, I have found that this practice builds both credibility and respect with most clients, certainly with sophisticated clients. Thus, with “View From the North Country,” I will continue to critically “look in the rearview mirror,” painful though it may sometimes be. Even an old dog can learn from his mistakes. REVIEWING LAST YEAR’S 2010 PREDICTIONS The Economy: I expected that the economic expansion would carry into 2012 with virtually no chance of a double dip. However GDP growth (2.9%?) proved to be less than the 3.5% I projected for 2010. Nevertheless, I correctly anticipated U.S. economic growth would significantly lag global growth “particularly that of emerging and lesser developed countries.” I believed employment would grow modestly in 2010, with the unemployment rate remaining “stubbornly high,” but certainly not as high as today’s 9.8%, just a tad below the cyclical peak of 10.1% (October 2009). U.S. Stock Market: I projected a peak zone of 1300-1350 for the S&P 500 in 2010. At current levels around 1240, the S&P 500 is 60 points shy of this target, but a strong Santa Claus rally (one I don’t expect, either) could possibly move this measure into the lower end of this range. A year ago I expected the 2010 market peak to be recorded in the first half of 2010 (not in December), then followed by a correction to “Battle of Hastings” level (1066). The correction’s actual low close was 1025. But I correctly anticipated a rally later in 2010 “if it appears a new cadre of fiscally responsible candidates are seated in Congress.” Earnings, U.S. Companies: I anticipated a continuing earnings recovery in 2010, but underestimated the degree of improvement. I was more optimistic than Jim Floyd’s estimate of +20% of S&P 500 reported earnings and +32% for operating earnings. But we both were too conservative. Cost controls (particularly labor costs) have served to widen profit margins. This, plus strong foreign based profits, produced earnings gains of +45% from 2009, significantly more than Jim and I anticipated. Interest Rates: I was convinced a year ago that interest rates would rise in 2010 as the economy continued to improve and with the Fed and Treasury gradually reducing yield manipulation tactics. BOY, WAS I WRONG! Even with the recent December rise in yields, 3-year Treasury yields are 0.92% compared to 1.63% a year ago, and 5-year Treasury yields are 1.85% compared to 2.68% a year ago. Longer term Treasuries are also lower than a year ago, but their differential is less. The same goes for quality 20-year corporates (down 32 bps), and certainly junk bonds, now yielding 8.12% compared to 9.20% a year ago. The only rise in the interest rate spectrum was in 90-day T-bills, which now yield a miniscule 0.12% up from 0.05% a year ago. Inflation in U.S.: I expected CPI inflation to rise to 3.5% in 2010, whereas this measure looks to be up only 1.2% for the year. Why is it that inflation is on the rise throughout the world, except here in the U.S.? I believe the U.S. CPI is grossly distorted by the 42% weight given to the Housing components, particularly the 25% weight given “Owners Equivalent Rent.” The +6% PPI 2010 projection was also wide of the mark. Our year end 2010 estimate is now +2.8% …..I currently also have doubts concerning the importance and construction of the PPI finished goods index, i.e. that it is not what it seems. Rather than producer costs, it is primarily based on wholesaler quoted prices not the prices producers must pay for materials they process. The Leuthold Group—December 2010 8 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. THE “CC” (Concentrated Core) PORTFOLIO This is a Limited Partnership with assets of almost $46 million. It is very flexible, sometimes very concentrated, and aggressive. With the help of Jim Floyd and Andy Engel, I manage this live portfolio for myself and any individuals who want to ride along in an LP format. I should add, my family foundation account employs the less aggressive Leuthold Core/Asset Allocation approach. The CC Portfolio was unchanged in terms of November performance, about in line with the S&P 500, which was also flat for the month. YTD (through December 10th), the CC Portfolio is up 2.3%, while the S&P 500 is up 13.4%. For much of 2010, this portfolio has underweighted equities. Performance for the CC Portfolio generated an impressive 32.8% gain in 2009, outpacing the S&P 500 which was up 26.5%. Asset Mix Changes Net equity exposure of 46.8% is defensive considering the still positive Major Trend Index. Back in September, when the Major Trend Index rose to positive, I initially increased equity exposure by trimming the equity short sale hedge and adding positions in long equity ETFs. However, since peaking at the end of October, the Major Trend Index has steadily moved lower, prompting my more defensive posture. …..Long equity ETFs have been eliminated, and replaced by short selling ETFs. This equity hedge now makes up a 7.7% holding in the CC Portfolio. …..The Concentrated Select Industries equity position was trimmed back by a reduction in the Wireless Infrastructure group. …..Global Clean Tech was also reduced to a 5.5% position. While I still like the long term prospects for this holding, it may be a little vulnerable near term. Concentrated Select Industries equity holdings now includes only 5 groups (in addition to the Holding Tank). Portfolio group holding are: Semiconductors (5.1% of total assets), Office Electronics (4.6%), Consumer Electronics (4.4% ), Electronic Components (1.0%), and Wireless Infrastructure (1.0%). The Hispanic Boom group was deactivated. Brazilian Bonds remain the CC Portfolio’s only Fixed Income position, and no changes are planned. There were significant changes to the Trading Futures part of the portfolio, reducing the 10-year T-note shorts and significantly increasing the Yen shorts. The initial Japanese Yen short was in early October. The substantial bet on higher interest rates via SHORT futures positions in long T-bonds and T-notes is now paying off. CC PORTFOLIO (December 10th Summary) EQUITIES EQUITY HEDGE 54.5% Best Performers In November (Net Exposure 46.8%) Concentrated Select Industries (Reduced) Foreign Focus Equity SE Asia Funds (Ex China) 11.5% Russia Funds 11.0% China Funds 9.1% Global Clean Tech (Reduced) Equity Index ETFs (Eliminated) TRADING FUTURES 5.5% 0.0% 7.7% 20.2% 49.5% Brazilian Bonds 20.2% (Nominal) SHORT Japanese Yen SHORT U.S. T-Notes SHORT Long T-Bonds 23.6% 9.9% 16.0% Gross Exposure: Available Cash: Net: The Leuthold Group—December 2010 +6% Consumer Electronics +5% Semiconductors +3% Equity Hedge 7.7% Short Selling Equity ETFs (Re-established) FIXED INCOME 17.4% 31.6% +1% SHORT Japanese Yen Worst Performers In November -5% Leuthold Clean Tech Fund -5% Wireless Infrastructure -2% Brazilian Bonds -1% SE Asia Funds 131.9% 0.0% 131.9% 9 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. SELECT INDUSTRIES PORTFOLIO: Initiating Position In Railroads Group Best performing portfolio groups in November were Semiconductors and Hypermarkets & Super Centers. The Select Industries Portfolio was in line with its benchmark for the month, +0.08% versus +0.01% for the S&P 500. Select Industries Weight Now 33% (E) 28 (E) 13 12 7 5 (U) 1 (U) 0 (U) 1 (U) 0 (U) S&P 500 Weight 11/30/2010 19% 11 11 11 11 15 4 3 12 3 DECEMBER SELECT INDUSTRIES PORTFOLIO Months Portfolio Period Holding Of Eligible Period Inclusion 17.4% Managed Health Care 13 24 14.6 Semiconductors 6 6 10.0 Hypermarkets & Super Ctr. (Increased) 4 5 9.3 Pharmaceuticals 3 17 8.4 Consumer Electronics 12 14 6.9 Deep Value 9 13 5.9 Electronic Manuf. Svcs. (Increased) 6 6 5.3 Div Financial Services 1 1 5.3 Electronic Components 4 7 4.6 Railroads (New) — 7 4.0 Office Electronics 1 3 8.3 Holding Tank (Decreased) — — Select Industries Weight Year Ago Information Technology Health Care Consumer Discretionary Consumer Staples Industrials Financial Materials Telecommunications Energy Utilities 28% 13 12 0 8 17 8 8 0 6 E = Portfolio Emphasis U = Portfolio Underweight Average: 5 Mo. 9 Mo. Buying Railroads: Initiating a small position in Railroads this month. The group has been Attractive for seven consecutive months, and is scoring very well in the Growth, Value, and Technical categories of the GS Scores. No Group Deactivations: There were no group deactivations this month, but substantially reduced the Holding Tank from 16.2% to 8.3%. Securities held in the tank are from groups we’ve previously deactivated but whose individual stocks outperformed. Once a holding tank stock underperform the benchmark in a month it is sold. …..Additional proceeds from these sales were used to increase the Hypermarkets & Super Centers and Electronic Manufacturing Services groups. MARKET CAP STRUCTURE GEOGRAPHIC EXPOSURE Select Industries Equity Portfolio: Now 12 Mo. Ago 24 Mo. Ago Dec 10 Dec 09 Dec 08 Large Cap: 60.9% 52.7% 41.8% Mid Cap: 34.4 43.3 35.6 Small Cap: 4.7 4.0 22.6 Select Industries Equity Portfolio: Now 12 Mo. Ago 24 Mo. Ago Dec 10 Dec 09 Dec 08 Domestic: 74.7% 67.5% 90.9% Developed Int’l: 18.3 20.6 5.9 Emerging Int’l: 7.0 11.9 3.2 Leuthold 3000 Stock Universe: Now 12 Mo. Ago 24 Mo. Ago Dec 09 Dec 08 Dec 10 Large Cap: 71.5% 73.8% 72.8% Mid Cap: 22.0 20.4 20.7 Small Cap: 6.5 5.8 6.5 PORTFOLIO PROFILE: Holdings: 93 stocks Weighted Median P/E: 12.1x (FY’10 est.) Weighted Median Beta: 1.10 Weighted Average Yield: 1.13% —Greg Swenson The Leuthold Group—December 2010 10 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. SPECIAL NOTE….. More Predictions Next Issue In my first issue of “View” in the new year (whenever that is) I plan to include capsule 2011 predictions for the following: U.S. Dollar Gold Crude Oil Budget Deficit Real Estate Venture Capital Industrial Metals Grains …..and the SUPER BOWL! The Leuthold Group—December 2010 11 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. The Leuthold Group, LLC provides research to institutional investors. It is also a registered investment advisor that uses its own research, along with other data, in making investment decisions for its managed accounts. As a result, The Leuthold Group, LLC may have executed transactions for its managed accounts in securities mentioned prior to this publication. The information contained in The Leuthold Group, LLC research is not, without additional data and analysis, sufficient to form the basis of an investment decision regarding any one security. The research reflects The Leuthold Group, LLC’s views as of the date of publication, which are subject to change without notice. The Leuthold Group, LLC does not undertake to give notice of any change in its views regarding a particular industry prior to publication of their next research report covering that industry in the normal course of business. The Leuthold Group, LLC may make investment decisions for its managed accounts that are inconsistent with, or contrary to, the views expressed in current Leuthold Group, LLC reports. As with any investment, there can be no assurance that any of the funds’ investment objectives will be achieved or that an investor will not lose a portion or all of his or her investment in a fund. Limited Partnerships may offer limited liquidity, may engage in speculative investment practices, may offer limited valuation information to investors and will not be registered. A prospective investor should consult its own tax advisor regarding tax consequences of an investment in a fund. This report does not constitute an offer or a solicitation of an offer to buy a security. Any offer of solicitation for Limited Partnerships must be made only by means of a delivery of a definitive private offering memorandum. The Partnership’s performance data have not been compiled, reviewed or audited by an independent accountant, and data for recent periods may be adjusted as a result of a subsequent audit of the year of which those periods are a part. Because the views expressed in Leuthold Group, LLC research relate to industry groups rather than individual securities, industry group ratings cannot be assumed to apply to each individual security within a group. Thus, if industry group “A” is ranked “Attractive,” The Leuthold Group, LLC may still decide to sell one or more of the component securities in group “A.” Weeden Investors, L.P., Weeden & Co., L.P.'s parent company, owns 22% of Leuthold Group’s voting securities. A Managing Director of Weeden & Co., L.P. is a member of The Leuthold Group, LLC board of directors. Weeden & Co., L.P. makes a market in ALGN, ALTR, AMCC, AMTD, AMZN, ASBC, ATHR, AZPN, BIDU, BRCM, CACC, CBRL, CELG, CFFN, CIEN, CMCSA, COST, CPTS, CRUS, CRZO, CSTR, CTRP, DECK, EEFT, ENDP, EQIX, ETFC, FLEX, FMER, FNFG, FOSL, FWLT, GRMN, GSIC, IBKR, INTC, IPGP, IPXL, ISBC, JOYG, LBTYA, LEAP, MCRL, MGLN, MINI, MSTR, NETL, NFLX, NIHD, NILE, NTRS, NVLS, ONNN, OXPS, PBCT, PCLN, PLXS, PNFP, PRGO, QDEL, RAIL, RFMD, SANM, SBAC, SCHW, SGMS, SIVB, SNDK, STEC, SVVS, TEVA, THQI, TMRK, TRMB, TSYS, TTMI, UFPI, UTHR, VIVO, VLTR, VPHM, VRTX , WCRX, XLNX and ZBRA. Weeden & Co., L.P. Member FINRA, NASDAQ, and SIPC. The Leuthold Group—December 2010 12 View From The North Country FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION.