274314563-Leuthold-Group-From-August-2015

advertisement

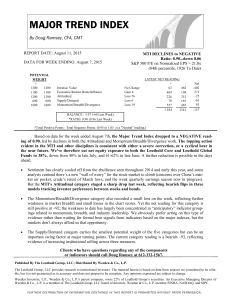

INSIDE THE STOCK MARKET ...trends, cross-currents, and outlook Prepared by: Doug Ramsey, unless otherwise noted http://leuth.us/stock-market Major Trend Index Holds Just Above Negative Zone For the first time in two years, the MTI’s Attitudinal category moved into positive territory at the end of July. Both the June and July Green Books pointed out that, in the past, the same development coincided with several important short and intermediate-term stock market lows. Too Many Highs, Too Many Lows The High/Low Logic Index, developed by market analyst Norman Fosback in the 1970s, provides one way to assess whether internal market disparities have become dangerously extreme. Valuation Gap In Chinese Equity Market A-shares are overvalued relative to Chinese companies listed in Hong Kong and the U.S. These overseas issues are still the better bet for investors bullish on China’s long-term outlook. On High Alert August is “National Eye Exam Month,” but this is the rare year we can confidently recommend that you skip it. Warnings of stock market trouble have become clearer to see without thick lenses or squinting. We can, just barely, make out the “big E” at the top of the eye chart, and suspect it means to “Exit.” We made another move in that direction in late July, cutting net equity exposure in tactical funds to 48%, from 55% in early July, and down from 61% six weeks ago. The Major Trend Index (MTI), along with related disciplines we look to for substantiation and reinforcement, are on the brink of negative signals. The table has already been set. Stock market valuations have been dangerous for at least a couple of years, and the Fed is slowly pulling away from its reckless experimentation—a good thing in the long term, but not for stocks in the intermediate term. Current stock market breadth, leadership, and momentum are all characteristic of a very late stage bull market. The smallest amount of additional “confirmation” will send us to an even more defensive posture—but we recognize the hazards of waiting for too much evidence to fall into place. • If the seasonal pattern of the past quarter century holds sway, that bearish signal should arrive this month. Yet another year we’ll have to miss out on the Hamptons… MSCI World Index: Average Monthy Performance, 1988 To Date 3.0 © 2015 The Leuthold Group 2.0 1.0 0.0 -1.0 -2.0 Jan Feb Mar The Leuthold Group—August 2015 Apr May Jun Jul 3 Aug Sep Oct Nov Dec http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Stock Market Observations The U.S. stock market has largely shrugged off the latest round of worries related to China’s stock market collapse, the new down-leg in crude oil, a more hawkish tone in Fed-speak, and sizable second-quarter declines in S&P 500 sales and earnings. Investors have had a more difficult time shrugging off those concerns, however. For the first time in two years, the MTI’s Attitudinal category moved into positive territory at the end of July. Both the June and July Green Books pointed out that, in the past, the same development coincided with several important short and intermediate-term stock market lows. Should contrarians gear up for a late summer rally? We don’t think so. The improvement in sentiment is encouraging, but not sufficient to trump the deterioration seen elsewhere in the MTI and related stock market tools. In particular, our market action work (i.e., the Momentum/Breadth/Divergence category) has sunk to its lowest level since the immediate aftermath of the severe 2011 market decline. For what seems like forever, we’ve been willing to downplay legitimate overvaluation concerns by explaining that, technically, valuations could become even more inflated, so long as the stock market continued to be “in gear.” (Or “uniform,” “egalitarian,” “cohesive” or other jargon meant to provide some variation on a trend that obviously outlived our vocabulary.) But, we can’t make that argument any longer. For what seems like forever, we’ve published the accompanying chart—we even devised a simple “Red Flag Indicator” around it a few months ago. The bulls point out that “not all of the red flags are flying.” However, while the Russell 2000 and S&P Financials did not confirm the May 21st high in the S&P 500, both have subsequently recorded new cycle highs. The broader picture (look at the chart from an arm’s length) is now clearly one of “fracturing” (or “divergence,” “distribution,” “bifurcation”). Fortunately, the market topping process is now so advanced that our readers shouldn’t have to suffer through these tortured descriptions for much longer. The next big move in stocks should be down. Consequently, we’re significantly more defensive than two months ago (48% net equity exposure versus 61% six weeks ago), and we expect to get more so as our disciplines allow. The Leuthold Group—August 2015 May 21, 2015 latest S&P 500 bull market high S&P 500 2000 2000 1800 1800 Dow Jones 65 Composite 6500 6500 6000 6000 5500 5500 Dow Jones Transports 9000 9000 8500 8500 8000 8000 7500 7500 7000 7000 650 650 Dow Jones Utilities 600 600 550 550 500 500 1300 1300 Russell 2000 1200 1200 1100 1100 S&P 500 Financials 300 300 S&P 500 Cyclical Sector Index* 460 440 460 440 420 420 400 400 380 380 NYSE Advance/Decline Line 46000 46000 44000 44000 42000 42000 © 2015 The Leuthold Group x10 x10 2014 M A M J J A S O N D 2015 M A M J J A *Equal-weighted composite of Consumer Discretionary, Industrials & Materials sectors. 4 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Weakening Foundation Over the last few months, we’ve presented a couple of simple quantitative studies meant to encapsulate the factors driving our Major Trend Index to the brink of bear territory. The chart and table might provide the best summary yet. • Leadership (Dow Jones Transportation and Utility Averages), breadth (NYSE Weekly Advance/ Decline Line), and corporate credit (DJ Corporate Bond Index) have all staged intermediateterm breakdowns by falling below their respective 40-week moving averages. But the S&P 500 has, through early August, remained impervious to this underlying trouble, holding above its own 40-week average and within 1-2% of a new cyclical high. • The bull market has ground on for so long that it’s tempting to ignore these internal warnings. After all, the chart shows several intermittent periods of weakness in Transports, Utilities, NYSE breadth and/or corporate bonds since the 2009 low. But the past six weeks represent the first period since 2008-2009 that all four series have simultaneously been in 40-week downtrends. The accompanying performance table shows that average S&P 500 annualized returns have been about zero under identical scenarios… but those “average returns” include significant pieces of the 1990, 2000-2002, and 2007-2009 bear markets. © 2015 The Leuthold Group 2000 2000 S&P 500 (weekly) 1500 1500 1000 1000 Dow Jones Transportation Average 5000 5000 Dow Jones Utility Average 600 500 600 500 400 400 300 4500 300 4500 Market Status Transports, Utilities, NYSE Breadth & Bonds above 40-wk moving avg. Three of four series above 40-wk moving average Two of four series above 40-wk moving average One of four series above 40-wk moving average None of four series above 40-wk moving average S&P 500 Ann. Gain Pct. Of Time +15.3% 35% +6.8% 22% +7.5% 16% -3.3% 11% -0.1% 16% Results for period April 1941 to date. 4000 NYSE Weekly Advance/Decline Line 4000 120 120 110 110 Dow Jones Corporate Bond Index 100 90 100 90 © 2015 The Leuthold Group 2007 2008 2009 2010 2011 2012 2013 2014 2015 All series shown with their 40-week moving averages. The Leuthold Group—August 2015 5 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Fed Watching For The 21st Century We’ve become a bit self-conscious about the extent to which “market action” analysis has grown to be a larger share of our commentary in the last few years (Charts 1, 2). But, such analysis is a critical piece of our broader allocation work—and one that (we think) grows in importance during the later innings of a bull market, when even sell-side market strategists are struggling to make a valuation case for stocks. Measures conventionally disChart 1 missed/dissed as purely technical, in fact, help us S&P 500, MidCap 400 & 2100 1700 gauge the liquidity backdrop for stocks. For inSmallCap 600 500 2000 stance, in light of the preponderance of NYSE(right scale) 1600 Indexes listed issues that are interest rate sensitive, we’ve 1900 argued for years that analysis of market breadth 1500 is simply an alternative (or perhaps complemen400 1800 (left scale) tary) approach to the more gentlemanly pursuit of 1400 Fed watching. 1700 1300 The Fed’s “creativity” during the post2008 period has been lauded, but it has undermined several fundamental relationships we once considered reliable. (We wrote an “Of Special Interest” piece on this topic in 2011 that’s overdue for an update.) For example, the rate of change in short-term interest rates “explodes” when rates are at zero. This is a stock market indicator first proposed at least a hundred years ago. Quantitative Easing compromised the once-revered message of the money supply measures, and a few years back, the Fed expunged a large set of valuable bank reserve data in a manner that would make Lois Lerner blush. These developments have increasingly forced us to monitor Fed policy in a sort of “second derivative” fashion—i.e., by monitoring movements in the asset markets themselves. 700 650 650 © 2015 The Leuthold Group 600 2014 M A M J J A S O N D 2015 M A M J J 600 A Chart 2 S&P 500, 400 & 600 Daily A/D Lines Dec 29th 500 500 500 450 450 May 18th 400 400 400 Jun 23rd 350 The sudden struggle of equal-weighted stock market indexes might well reflect the impact of tightening that’s either already occurred (the lagged impact of seven QE tapering moves), or that is still to come. Several of these equalweighted indexes have gone into relative strength free-falls over the past six weeks (Chart 3), and the Guggenheim Russell 2000 Equal Weight ETF (EWRS) has already suffered an “official,” CNBC-approved correction of –10% into its July 27th low. 350 600 © 2015 The Leuthold Group 2014 M A M J J A S O N D 2015 M A M J J A Chart 3 160 S&P 500, 400 & 600: Equal/Cap-Wtd RS Ratios 160 158 158 500 156 156 82.0 81.5 81.0 80.5 80.0 79.5 In sum, deteriorating stock market breadth and worrisome leadership trends both suggest liquidity has already tightened; whether the Fed follows suit in September may now be just a formality. The Leuthold Group—August 2015 700 600 600 125 124 123 122 121 120 119 © 2015 The Leuthold Group 2014 6 82.0 81.5 81.0 80.5 80.0 79.5 400 M A M J J A S O N D 2015 M A M J J 125 124 123 122 121 120 119 A http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Too Many Highs, Too Many Lows We’ve detailed the growing degree of stock market bifurcation, but the problem for would-be bears is that such bifurcation can reach astonishing levels (witness 1999-2000) before the market is set to peak out. The High/Low Logic Index, developed by market analyst Norman Fosback in the 1970s, provides one way to assess whether internal market disparities have become dangerously extreme. The weekly NYSE High/ Low Logic Index is calculated as the lesser of: (1) new 52-week highs as a percentage of NYSE issues traded; or (2) new 52-week lows as a percentage of NYSE issues traded. For analytical purposes, the figure is generally smoothed with a short- to intermediate-term moving average (we use 10 weeks). High readings indicate simultaneously large numbers of stocks making highs and lows, indicating a dangerously high degree of internal divergence. Chart 1 © 2015 The Leuthold Group 2000 2000 S&P 500 NYSE new 52-week highs and lows are both at elevated levels, a sign the stock market has become internally fractured. 1500 1000 The bifurcation within the NYSE might come as no surprise, given its extreme underperformance versus the NASDAQ market in the last year. But the High/ Low Logic Index for NASDAQ (Chart 2) shows a similar level of discord; its 10-week moving average has just entered the bearish zone. Note that similar readings appeared immediately before the market collapses of 2000-2002 and 2007-2009, and did not experience the bothersome false signals issued by the NYSE version of the indicator. The Leuthold Group—August 2015 6 Above 5% - Tape is "divergent"- BEARISH 5 The High/Low Logic Index entered 2015 at a maximum bearish reading above 5% (Chart 1), and following a four-month respite, has again spiked into this danger zone. We recognize that the indicator issued a set of failed signals in the second half of 2013, but today’s bear signal occurs with a broader array of supporting bearish evidence than two years ago. 7 (10-Wk. Avg.) 6 1000 false signals NYSE High/Low Logic Index* 7 1500 5 4 4 3 3 2 2 1 1 Below 1% - Tape is "in gear"- BULLISH 0 2007 2008 2009 2010 2011 2012 2013 2014 0 2015 *Index calculated as the lesser of NYSE Weekly New Highs and New Lows as a percentage of issues traded. Chart 2 5500 5000 4500 5500 5000 4500 NASDAQ Composite 4000 4000 3500 3500 3000 3000 2500 2500 2000 2000 1500 1500 NASDAQ High/Low Logic Index* (10-Wk. Avg.) Above 6% Tape is divergent = BEARISH 7 6 5 4 3 2 1 0 7 6 5 4 3 Below 1.5% - Tape is in gear - BULLISH 99 00 01 02 03 04 05 06 07 © 2015 The Leuthold Group 08 010 10 11 12 13 14 2 1 0 15 *Index calculated as the lesser of NASDAQ Weekly New Highs and New Lows as a percentage of issues traded. 7 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Minding The Gaps We think stock market action in the next few months will provide the Fed with an excuse to skip any rate increase in 2015. But our view is a minority one, and futures’ market odds on a September increase shot up in early August. Either way, the obsession over the timing of a Fed rate hike ignores the fact that world P/E ratios are already contracting—at least on the basis of our 5-Year Normalized EPS. • Normalized P/E ratios for both the U.S. and foreign Developed markets peaked in June 2014, and the latter is down significantly (16.9x in July, down from a peak of 19.5x). Emerging Market Normalized P/E ratios are flirting with their 2001 and 2011 lows. But the declines have done nothing to close the U.S./foreign valuation gaps. 40 Normalized P/E Ratios: U.S. Vs. Rest Of World 35 35 30 30 MSCI USA Index 25 25 22.3x 20 20 16.9x (World Ex USA) 15 © 2015 The Leuthold Group 92 94 15 11.2x (Emerging Markets) 10 90 The Leuthold Group—August 2015 40 Foreign Valuation Gaps Are Still Gaping... 96 98 8 00 02 04 06 08 10 12 14 16 10 18 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Emerging Markets: A Half-Off Sale! The Chinese government’s repeated stock market intervention attempts over the past several weeks have been remarkable, and obviously antithetical to the country’s move toward a more laissez faire corporate environment. But—with the Shanghai Composite still up 66% (Chart 1) in the last 12 months—are artificial supports even necessary? …It’s akin to keeping interest rates at zero during the seventh year of a bull market and economic expansion. The July swoon drove Emerging Market equities down to relative valuation levels seen only very briefly during their (admittedly short) history. The MSCI Emerging Markets Index now trades at a 5-Year Normalized P/E of 11.15x—an exact 50% discount to the same calculation for the MSCI USA Index (Chart 2). We’ll admit the valuation gap has become so wide that we’re increasingly tempted to override our EM Allocation Model (which has presciently remained bearish for the past 4 1/2 years, Chart 3). But we fear this gap might not begin to reverse until a cyclical bear market erupts; this month’s “Of Special Interest” section reinforces our long-time argument that value-based approaches are prone to stumble during the bull’s final charge. Chart 2 Chart 1 Shanghai Composite 5200 MSCI Emerging Markets Vs. USA Relative P/E on 5-Yr. Normalized EPS 1.35 1.30 1.25 1.20 (weekly) 1.15 1.10 5000 1.05 1.00 4800 0.95 0.90 0.85 4600 0.80 0.75 4400 0.70 0.65 0.60 4200 4000 0.55 now at a 50% discount 0.50 0.45 © 2015 The Leuthold Group 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Chart 3 3800 0.50 3600 Emerging Vs. Developed Markets Allocation Model 0.45 0.45 0.40 0.35 3400 down almost a third-but still a nice gain on the year 0.30 Total Return Ratio, MSCI Emerging Markets/ MSCI World Index (USD - Monthly) February April May June July August 0.40 0.35 0.30 0.25 0.25 0.20 0.20 0.15 0.15 0.10 0.10 EM Allocation Model* 1.2 2015 LATEST SIGNAL: Switch into MSCI World Index on February 28, 2011. 3200 3000 © 2015 The Leuthold Group 0.50 1.2 1.1 1.1 1.0 1.0 0.9 0.8 0.9 © 2015 The Leuthold Group model "reiterated" a SELL signal in July 0.8 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 *Buy Emerging Markets when Total Return Ratio breaks above upper band, and remain positioned there until Ratio drops below lower band, triggering a switch into the MSCI World Index. The Leuthold Group—August 2015 9 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. The 30/30 Club! The S&P 500 Energy sector’s latest plunge puts it down by almost a third in the last 14 months, placing it among the worst “isolated” sector declines in recent history (Chart 1). In January, we noted Energy had already suffered a 20% loss outside of a broader cyclical bear market; there have been only 19 other instances of such “stand-alone” sector bear markets since 1990. But Energy now belongs to the considerably more exclusive list of sectors which have declined 30% on both an absolute basis and relative to the S&P 500—yes, the “30/30” Club! With only three prior cases to consider (Charts 2-4), we shouldn’t draw generalizations. But we can’t help it: Note that when these other stand-alone sector declines came to an end, either a broad market correction (1994) or bear Chart 1 market (2000-2002) was on the im760 740 mediate horizon. The message may 720 be that when liquidity is no longer 700 sufficient enough to float all of the S&P 500 680 sector “boats,” trouble may soon be on Energy 660 the way. Again, there’s not enough (daily) 640 history to say. 620 With Energy groups still ranking near the bottom of our GS framework (Refiners are the exception), is it time to worry about Energy joining the 40/40 Club (40% decline/40% underperformance)? Only the Consumer Staples sector has achieved that status (appropriately enough, during the peak of baseball’s steroids era from 1998 to 2000). 600 580 560 540 520 -32.8% (August 4th) © 2015 The Leuthold Group 2014 Mar Apr 500 May Jun Jul Aug Sep Oct Nov Dec 2015 Mar Apr Chart 2 May Jun Jul Aug Sep Chart 3 105 265 260 255 250 245 240 235 100 230 225 95 220 125 120 S&P 500 Health Care 115 110 1992-1993 215 90 210 205 85 200 80 -38.6% © 2015 The Leuthold Group 1992 M A N D 1992 M J J A S O 1993 M A M J N D 1993 J A 75 S O N Chart 4 170 195 190 S&P 500 Consumer Staples 185 180 175 170 1998-2000 165 160 165 155 160 155 150 -40.8% © 2015 The Leuthold Group O N D 1999 1999 M A M J 150 145 2000 M A M J A S O N D 2000 145 140 135 S&P 500 Materials 130 125 1999-2000 120 -30.0% © 2015 The Leuthold Group 1999 1999 M The Leuthold Group—August 2015 A M J J A S O N D 10 2000 M 2000 A 115 M http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. The 30/30 Club (continued) Is a severe, isolated sector decline like Energy’s apt to be followed by outperformance? Based on our tiny sample, the answer is yes. • As shown in Table 1, Health Care, Staples, and Materials sectors all reversed their “30/30” underperformance during the subsequent two years, beating the S&P 500 by an average margin of +47.6%. Table 1 The 30/30 Club: S&P 500 Sectors To Have Declined 30% On Both An Absolute And Relative Basis Outside Of A Cyclical Bear Market Pct Decline Pct Decline Rel to S&P 500 Relative Perf. Next 6 Mos. Relative Perf. Next 12 Mos. Relative Perf. Next 24 Mos. 16.3 % 57.7 % 67.7 % Sector Dates Consumer Staples November 23, 1998 - March 14, 2000 -40.8 % -55.1 % Energy June 23, 2014 - August 4, 2015 -32.8 -39.4 Health Care January 9, 1992 - August 12, 1993 -38.6 -46.1 9.4 16.1 37.9 Materials May 6, 1999 - March 7, 2000 -30.0 -31.8 -11.3 23.1 37.3 Average -35.5 % -43.1 % 32.3 % 47.6 % *Cyclical Bear Markets in the S&P 500: July 16, 1990 - October 11, 1990 July 17, 1998 - August 31, 1998 March 24, 2000 - October 9, 2002 October 9, 2007 - March 9, 2009 April 29, 2011 - October 3, 2011 4.8 % After the decline ended, forward sector relative returns from this tiny sample were excellent. © 2015 The Leuthold Group Chart 5 • • With our focus (and, for that matter, most everyone’s) on the S&P 500 lately, we nearly overlooked some of the incredible stats being put up these days in the minor leagues. Think the 30/30 Club is a big deal? There’s a Small Cap sector that’s just joined the 60/60 Club! Yes, the S&P SmallCap 600 Energy sector had declined 64.0% into its August 4th low (Chart 5), underperforming the S&P SmallCap 600 by –67.8% since June 30, 2014. Again, Energy groups (save for the Refiners) rate poorly in our Group Selection (GS) model, and we don’t have a separate framework to handle the Small Cap groups. But this chart finally smacks of capitulation… The Leuthold Group—August 2015 S&P SmallCap 600 Energy Sector 2000 1900 1800 1700 1600 1500 1400 1300 1200 1100 1000 900 800 -64.0% © 2015 The Leuthold Group 2011 11 2012 700 (August 4th) 2013 2014 2015 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. Avoiding Gold The vast majority of recent gold commentary centers on its extremely oversold technical condition and the related washout in all sorts of sentiment indicators, ranging from trader surveys to futures and options positioning. Maybe these conditions will produce a short-term bounce, but we’re going to stand with the message of our bearish longer-term work. Chart 1 “Oversold” is in the eye of the beholder. Gold’s four-year decline of around 40% does not look all that cathartic on a monthly chart, especially one that’s logarithmically scaled like the accompanying Chart 1. Bullion would need to drop another 40% to reach its median long-term ratio versus the Consumer Price Index. And the ratio’s many years of levitation above its median raises the odds of an overshoot, when and if that median is crossed. (We’ve expressed the same concern over crude oil, which— for all the carnage its collapse has triggered—has merely returned to an average level on a CPI-adjusted basis.) Gold Futures 2000 (monthly) 1800 1600 Gold's 40% decline still looks muted on a logarithmic scale... 1400 1200 1000 800 $693 Implied target if the Gold/CPI Ratio falls to its 1970to-date median. Gold’s action has historically been a pretty good harbinger of near-term price trends for industrial commodities, although the relationship has weakened since the onset of the Great Recession. Historically, the 12-month rate of change in gold has led the 12month rate of change in the CRB Raw Industrials by about six months (Chart 2). Based on that trend, gold’s 12-month decline of 15% suggests further near term weakness in the CRB (even though the latter also looks oversold in price and washed out on the basis of most sentiment measures). 600 400 © 2015 The Leuthold Group 2000 2010 Chart 2 200 © 2015 The Leuthold Group Gold's Action Points To Even Lower Prices For Industrial Commodities 150 200 150 100 100 12-Mo. Pct. Chg. In Spot Gold, Advanced 6 Months 50 50 0 0 12-Mo. Pct. Chg. In CRB Raw Industrials -50 -50 70 72 74 76 78 The Leuthold Group—August 2015 80 82 84 86 88 90 92 94 12 96 98 00 02 04 06 08 10 12 14 16 18 http://leuth.us/stock-market FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION.