MAJOR TREND INDEX - The Leuthold Group

advertisement

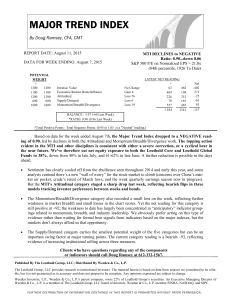

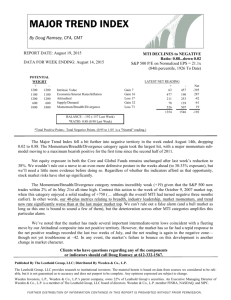

MAJOR TREND INDEX By Doug Ramsey, CFA, CMT REPORT DATE: January 27, 2016 DATA FOR WEEK ENDING: January 22, 2016 PO TENTIAL WEIGHT + 1200 1200 1100 1100 1200 1200 600 600 1800 1800 Intrinsic Value Economic/Interest Rates/Inflation Attitudinal Supply/Demand Momentum/Breadth/Divergence Status: Negative Ratio: 0.80...Up 0.07 S&P 500 P/E on Normalized EPS = 19.1x (65th percentile, 1926 To Date) Gain 36 Loss 4 Gain 115 Loss 8 Gain 2 LAT EST NET READING + 78 288 467 129 400 148 116 156 204 868 1265 1589 Net -210 338 252 -40 -664 -324 BALANCE : -324 (-465 Last Week) *RAT IO: 0.80 (0.73 Last Week) *T otal Positive Points : T otal Negative Points. (0.95 to 1.05 is a "Neutral" reading.) Based on data through last Friday, the Major Trend Index rose 0.07 points to a ratio of 0.80. It benefited from a huge jump (115-points) in the Attitudinal category and a solid gain in the Intrinsic Value work. Steady improvement in these countertrend categories, combined with deeply negative readings in the Momentum/Breadth/ Divergence work, is characteristic of an ongoing cyclical bear market; the body of evidence suggests it’s still too early to hit a major low in equities. Following last week’s equity hedge reduction of about 5%, both the Leuthold Core and Global Funds are now positioned with net equity exposure of 37%. While we expect considerably more downside before stocks find a bottom, we are encouraged by developments in the Intrinsic Value category during the bear’s most recent downleg. The current net reading of –210 compares with three peak readings of –415 in the weeks surrounding the June 23, 2015 all-time highs in the S&P MidCap 400 and Russell 2000. Charts 1 & 2 show the sizable valuation adjustments for the Leuthold 3000 Universe and the Leuthold Small Cap Universe (1200 stocks) in particular; both measures now reside in their broad “fair value” ranges, which we define as historical percentile readings between 30 and 70. If U.S. blue chips meet even the minimum bear market decline threshold of 20%, look for readings on Charts 1 & 2 to move into the undervaluation zones. The week’s improvement in the Attitudinal category was broad, though we’re still mystified as to why the VIX has registered so little panic during the decline. Mutual fund timers, however, did panic last week, sending the Rydex Ratio down to a level that coincides with the late September market lows. These developments are encouraging, but should be expected given the horrid price action YTD; however, they are certainly not enough on which to build a longer term bullish case (yet). Clients who have questions regarding any of the components or indicators should contact Doug Ramsey 612-332-1567, dramsey@LWCM.com Published By The Leuthold Group, LLC The Leuthold Group, LLC, provides research to institutional investors. The material herein is based on data from sources we considered to be reliable, but it is not guaranteed as to accuracy and does not purport to be complete. Any opinions expressed are subject to change. FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION. MAJOR TREND INDEX (continued) REPORT DATE: January 27, 2016 Unweighted (or median) stock valuations are no longer dangerously high. The odds are good that the median stock in our Leuthold 3000 Universe will move into its undervaluation zone (below the 30th percentile) during this decline. Chart 1 33 32 31 Leuthold 3000 Median Normalized P/E 33 (Based on 5-Yr. Normalized EPS) 32 31 30 30 29 29 28 28 27 27 26 26 25 25 70th percentile = 24.0x 24 24 23 23 22 22 21 21 Jan 22 21.2x 20 30th percentile = 19.7x 19 20 19 18 18 17 17 16 16 15 15 14 14 13 13 12 12 11 11 10 10 © 2016 The Leuthold Group 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Chart 2 © 2016 The Leuthold Group September 19, 1997 30.3x December 27, 2013 29.8x June 1, 2007 29.2x January 22, 2016 21.8x Leuthold Small Cap Universe Median P/E on 5-Yr. Normalized EPS (Leuthold Small Cap Universe = Deciles 5-8 of Leuthold 3000) 1980 1990 2000 10.6x March 6, 2009 31 30 29 28 27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 2010 Published By The Leuthold Group, LLC The Leuthold Group, LLC, provides research to institutional investors. The material herein is based on data from sources we considered to be reliable, but it is not guaranteed as to accuracy and does not purport to be complete. Any opinions expressed are subject to change. FURTHER DISTRIBUTION OF INFORMATION CONTAINED IN THIS REPORT IS PROHIBITED WITHOUT PRIOR PERMISSION.