CIMB-Principal Income Plus Balanced Fund Fact Sheet

advertisement

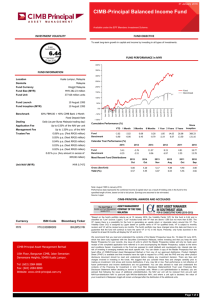

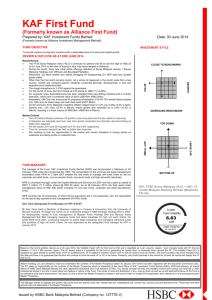

31 January 2016 CIMB-Principal Income Plus Balanced Fund A S S E T MA N A GE ME N T INVESTMENT VOLATILITY FUND OBJECTIVE To provide capital growth over the medium to long-term as well as income distributions. 3-year Fund Volatlity 3.82 Low FUND PERFORMANCE in MYR Lipper Analytcs 15 Jan 2016 290% 270% FUND INFORMATION 250% 230% Location Kuala Lumpur, Malaysia Domicile Malaysia 190% 170% Ringgit Malaysia 150% MYR 82.63 million 130% 265.61 million units 110% Fund Currency Fund Size (MYR) Fund Unit 210% Fund Benchmark 90% 70% Fund Launch 12 March 1998 50% Fund Inception (MYR) 12 March 1998 30% Dealing Application Fee Management Fee Daily (as per Bursa Malaysia trading day) Up to 5.00% of the NAV per unit 0.08% p.a. of the NAV MYR 0.3110 Unit NAV (MYR) Feb-2015 Feb-2014 Feb-2013 Feb-2012 Feb-2011 Feb-2010 Feb-2009 Feb-2008 Feb-2007 Feb-2006 Feb-2005 Feb-2004 Cumulative Performance (%) YTD 1 Month Up to 1.85% p.a of the NAV Trustee Fee Feb-2003 - 50% Feb-2002 - 30% Feb-2001 Fixed Deposit Rate - 10% Feb-2000 40% FBM100 + 60% CIMB Bank 1-Month Feb-1999 10% Benchmark Fund Benchmark -1.34 -0.51 3 Months 6 Months 0.54 0.56 -0.11 0.01 -1.34 -0.51 1 Year 3 Years 5 Years 1.17 -0.44 8.63 7.24 Since Inception 18.83 14.58 248.07 150.69 Calendar Year Performance (%) Fund Benchmark 2015 2014 2013 2012 2011 2010 3.67 0.79 -1.21 -0.66 6.57 6.37 6.09 5.66 4.29 2.75 15.07 9.93 Most Recent Fund Distributions Gross (Sen/Unit) Yield (%) 2016 Jan 2015 Jul 2015 Jan 2014 Jul 2014 Jan 2013 Jan 0.95 2.92 1.10 3.28 1.10 3.05 1.10 3.20 1.10 3.06 1.01 2.91 Note: March 1998 to January 2016. Performance data represents the combined income & capital return as a result of holding units in the fund for the specified length of time, based on bid to bid prices. Earnings are assumed to be reinvested. Source: Lipper CIMB-PRINCIPAL AWARDS AND ACCOLADES Currency MYR ISIN Code Bloomberg Ticker MYU1000AG004 COMINPI MK CIMB-Principal Asset Management Berhad 10th Floor, Bangunan CIMB, Jalan Semantan Damansara Heights, 50490 Kuala Lumpur. Tel: (603) 2084 8888 Fax: (603) 2084 8899 Website: www.cimb-principal.com.my ^Based on the fund's portfolio returns as at 15 January 2016, the Volatility Factor (VF) for this fund is 3.82 and is classified as "Low" (source: Lipper). "Low" includes funds with VF that are above 1.395 but not more than 6.550. The VF means there is a possibility for the fund in generating an upside return or downside return around this VF. The Volatility Class (VC) is assigned by Lipper based on quintile ranks of VF for qualified funds. VF is subject to monthly revision and VC will be revised every six months. The fund's portfolio may have changed since this date and there is no guarantee that the fund will continue to have the same VF or VC in the future. Presently, only funds launched in the market for at least 36 months will display the VF and its VC. We recommend that you read and understand the contents of the Master Prospectus Issue No. 19 dated 30 June 2015, which has been duly registered with the Securities Commission Malaysia, before investing and that you keep the said Master Prospectus for your records. Any issue of units to which the Master Prospectus relates will only be made upon receipt of the completed application form referred to in and accompanying the Master Prospectus, subject to the terms and conditions therein. Investments in the Fund are exposed to country risk, credit (default) and counterparty risk, currency risk, interest rate risk, risk of investing in emerging markets and stock specific risk. You can obtain a copy of the Master Prospectus from the head office of CIMB-Principal Asset Management Berhad or from any of our approved distributors. Product Highlight Sheet ("PHS") is available and that investors have the right to request for a PHS; and the PHS and any other product disclosure document should be read and understood before making any investment decision. There are fees and charges involved in investing in the funds. We suggest that you consider these fees and charges carefully prior to making an investment. Unit prices and income distributions, if any, may fall or rise. Past performance is not reflective of future performance and income distributions are not guaranteed. You are also advised to read and understand the contents of the Financing for Investment in Unit Trust Risk Disclosure Statement/Unit Trust Loan Financing Risk Disclosure Statement before deciding to borrow to purchase units. Where a unit split/distribution is declared, you are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from pre-unit split NAV/cum-distribution NAV to post-unit split NAV/ex-distribution NAV; and where a unit split is declared, the value of your investment in Malaysian ringgit will remain unchanged after the distribution of the additional units. Page 1 of 2 31 January 2016 CIMB-Principal Income Plus Balanced Fund A S S E T MA N A GE ME N T FUND MANAGER'S REPORT PORTFOLIO ANALYSIS The Fund fell 1.34% in January, and underperformed the benchmark by 0.83%. Fixed income outperformed, but equities underperformed. Equities were hit by the weaker performance in exporters as a result of stronger MYR in January 2016. For fixed income, main contributors were from power, quasi-government , construction and banking related bonds. ASSET ALLOCATION Fixed Income 63.30% Equities (Local) 34.07% Cash 2.63% 100.00% Total Equities had a rocky start in 2016 as the FTSE Bursa Malaysia Kuala Lumpur Composite Index ("FBMKLCI") shed 1.46%. Key global events in January were: 1) Discussion about recession risk 2) Bank of Japan’s negative interest rates stance 3) Oil prices dipping below USD30/barrel 4) Russia floating proposals for joint oil production cuts with OPEC 5) US Federal Reserve interest rates path may be less steep. The question is whether markets are reverting to the asset reflationary theme, boosted by central banks’ dovish stance. Locally, Malaysia announced the 2016 recalibrated budget outlining 11 measures to commit to the 3.1% fiscal deficit. The headline forecasts are: 1) Fiscal deficit target maintained at 3.1% to Gross Domestic Product (GDP); 2) Brent crude oil priced at USD30-35 from USD48/barrel and 3) GDP growth revised down to 4.0-4.5% from 4.0-5.0%. Key measures for fiscal consolidation include the refarming of telco spectrum and cutting employees Employees Provident Fund contribution by 3% to stir private consumption. Implementation of key projects such as MRT, LRT, HSR, Pan-Borneo and RAPID will proceed. The Government stressed that they will neither impose capital control nor peg the Ringgit (MYR). During the month, the MYR strengthened 3.41% to 4.148. SECTOR BREAKDOWN We think the current strength in MYR is not sustainable. Hence, we continue to like Exporters, but will rotate into lower Price Earnings Ratio, high growth names. We like Construction companies for infrastructure plays. We underweight Telcos as the sector could be de-rated over spectrum refarming and keen competition. We also underweight Banks due to slowing loans growth and weaker asset quality. For fixed income, we prefer selective corporate bonds from the primary and secondary market with higher coupon for better yield enhancement. Fixed Income 63.30% Trading / Services 10.55% Finance 7.54% Industrials 6.44% Construction 2.61% Technology 2.22% Mutual Fund 1.80% IPC 1.50% Plantations 0.84% Consumer 0.37% REITS 0.20% Cash 2.63% 100.00% Total RISK STATISTICS TOP HOLDINGS Beta 1.12 1 Golden Assets Intl Fin Ltd Malaysia AA3s 9.36% Information Ratio 0.32 2 Tanjung Bin Energy Issuer Bhd Malaysia AA3 6.39% 3 Sarawak Energy Bhd Malaysia AA1 6.16% 4 Bank Muamalat Malaysia Malaysia A3 6.08% 5 Syarikat Prasarana Negara Bhd Malaysia GG 6.01% 6 Alliance Bank M Bhd Malaysia A2 4.85% 7 Eversendai-Corp Bhd Malaysia A2 4.71% 8 Temasek Eksklusif Sdn Bhd Malaysia AA3s 4.23% 9 Sports Toto Malaysia Sdn Bhd Malaysia AA- 3.65% Sharpe Ratio -0.15 3 years monthly data 10 Tenaga Nasional Bhd Total Malaysia 3.47% 54.91% Page 2 of 2