Indirect tax

advertisement

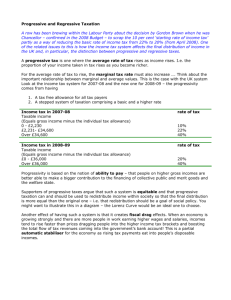

Methods to Promote Equity: Policies of Redistribution Ch. 11, p. 309-318 What is the difference between a direct and indirect tax? What are examples of each? Define and explain the difference between proportional, progressive, and regressive taxes. How can income tax be used to lower income inequalities? Adam Smith’s “canons of taxation” • Smith outlined four main characteristics of taxation in TWoN: – Certainty: those paying should know how much they are paying – Convenience: easy to collect – Economy: taxes should be cheap to collect realtive to their yield (“cost-efficient” to collect) – Equity: fairness of taxes levied, efficiency (not counterproductive to goals of economic policies) Equity Equity in tax terms means “fairness” of taxes levied (i.e., burden should be felt equally among those paying): • Horizontal equity: “treating equals equal”—two people having the same income should pay the same tax • Vertical equity: “treating different people differently” in order to enhance fairness; less tax paid by lower income earners than higher (again, normative) Transfer payments: why taxes matter • Transfer payments: payments made by the government to individuals specifically for redistributing income away from certain groups and towards others – Transferred from those who work and pay taxes towards those who cannot/need assistance – Groups are called vulnerable and include: elderly, sick, very poor (and their children), unemployed Types of payments: • Old age pension (Social Security in the US) • Disability pensions • Unemployment benefits • War veterans’ benefits • Housing benefits for the poor • Student grants • Etc…. Other methods of distribution The government uses other methods to help with income inequalities: 1. Subsidized provision or direct provision of merit goods: – Health and education (major goods under-consumed by those with low incomes/in poverty); both in provision and accessibility – Provision of infrastructure, including physical capital such as clean water, sanitation This works by making certain goods available to people on low incomes that would not otherwise be able to afford them. 2. Government intervention in markets; i.e., minimum wage legislation, food price ceilings; rent control; price floors for farmers 3. Taxation: the most important source of government revenue and source of transfer payments and subsidized provision of goods (allows achievement of greater equity through direct and indirect methods) Two broad categories of taxes: – Direct – indirect Direct taxation • Direct taxation: tax paid directly to the government tax authority by the taxpayer – in the US, the IRS – Taxpayer=economic agents=firms and households – Paid on income, wealth, or property Firms pay: – Profit tax (corporate income tax) – Labor tax Households/individuals pay: – Income tax – Capital gains tax (profits from stockholding) – Property tax/inheritance tax One extra type… • Social insurance contribution (payroll tax)—paid by workers and their employees • Instead of going into the gov’t budget (fiscal year spending), it goes into specific funds for pensions, SS, and health care (i.e., Canada) • This is also known as “earmarked” taxation, as the money is earmarked, or set aside, for a certain purpose • So why would it matter that many of today’s workers will be retiring in the next 20 years? Indirect taxation • Indirect tax--tax paid indirectly to the government tax authority by firms selling goods/services – Taxes on spending on g/s • Indirect taxes affect supply, implying that market equilibrium is negatively affected – Supply curve shifts left – Can have negative and positive outcomes (externalities) Types of indirect taxes: • Value-added tax (VAT; Europe, Asia) or sales tax in the US • Excise duties (on specifics/ “bad” g/s such as tobacco, gasoline, alcohol, gambling in US) • Tariffs (taxes on imports) – aka customs duties Calculating tax • Using a tax table, multiply income times the corresponding tax rate. – Data available through IRS or other government taxation organization – Example (simple) table for Europe on p. 313 Progressive tax • Progressive tax—as income increases, the fraction of income paid in taxes increases; creating an increasing tax rate • Is it the most “fair”? Why? According to what principle? Examples: • Income tax – Based on marginal tax rate, calculated using “layers” of income, or income brackets • Taxes on luxury items, for example, yachts and private jets – not normally paid by lower income people; only paid by people wealthy enough to purchase such items Proportional tax • Proportional tax—as income increases, the fraction of income paid as taxes remains constant; constant tax rate Examples: • Some countries’ income taxes (flat tax) – Can also be progressive with addition of exclusions (amounts not taxed, etc.) • Sales tax Regressive tax • Regressive tax—as income increases, the fraction of income paid as taxes decreases; decreasing tax rate – “flat-rate” tax, or unit tax • Indirect taxes are always regressive. – A slight exception may be tax-exempt items such as necessities like medicines Examples: • The FICA (Federal Insurance Contributions Act) tax is a federal payroll tax used to fund Social Security • Sales tax can also be considered a regressive tax. – Every person buys relatively the same amount of food regardless of their income. • Therefore a low income person would pay a larger proportion of their income for food sales tax than a high income person A note about these taxes • All three: progressive, regressive, and proportional relate not just to income tax, but to all types of tax (direct or indirect) • This is because taxes are paid out of income; therefore, they can be compared with income • The more progressive the tax system, the more equal is the after-tax distribution of income, compared to the pre-tax distribution. • Regressive tax systems tend to make the distribution of income less equal.