Partnership TAx

advertisement

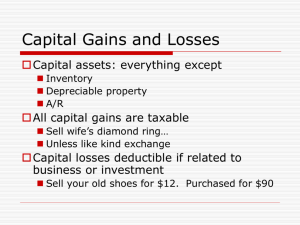

Section 1231 • • Congress added this section to help taxpayers during the 1940’s and it continues today. Essentially, – Net gains become capital, resulting in lower rates. – Net losses become ordinary, resulting in deductibility. • Recall that section 1211 strictly limits the deductibility of capital losses. TPs with net gains benefit from low rates and TPs with net losses benefit from no limits on deductibility. © Steven J. Willis 2000 1 Section 1231(b) Property • 1231(b) defines the applicable property – Depreciable property held > 1 year – Real property (land, essentially) held > 1 year and used in a trade or business • But not PHPSCOCTB Section 1221(a)(2) excludes this property from capital asset status. A common mistake among students is to view this property as thus ordinary property! It fits in a middle category: 1231 property. © Steven J. Willis 2000 2 Two Main Steps of 1231 • • Step One: – FIRE POT Step Two – HOTCH POT If HOTCH POT is negative, all gains and all losses are ordinary! Called the “firepot” because of this language. Gains & losses from fire, storm, shipwreck, other casualty or theft of: 1. 2. 3. © Steven J. Willis 2000 If FIRE POT is negative, all gains and all losses are ordinary. TB property TB LTCA Transaction for Profit LTCA NEGATIVE POSTITIVE Gains & losses from sale or exchange of: 1. 2. If HOTCH POT is positive, all gains and all losses are LT capital. NEGATIVE TB property Non-Fire Pot gains & losses from involuntary conversions of 1. TB property 2. TB LTCA 3. For Profit LTCA POSTITIVE If FIRE POT is positive, all gains and all losses are dumped into the HOTCH POT. 3