Last Semimester Homework

advertisement

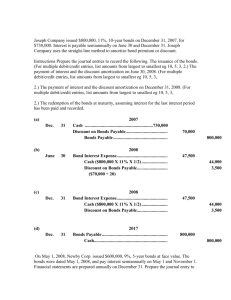

Doran Chan Spring I '06 E17-1 AMA202.0035 Prof. Angela Wu For the following investments indentify whether they are: 1. Trading Securities 2. Available-for-Sale Securities 3. Held-to-Maturity Securities Each case is independent of the other. 1 (a) A bond that will mature in 4 years was bought 1 month ago when the price dropped. As soon as the value increases, which is expected next, noth it will be sold. 2 (b) 10% of the outstanding stock of Farm-Co was purchased. The company is plannin on eventually getting a total of 30% of its outstanding stock. 1 (c) 10-year bonds were purchased this year. The bonds mature at the first of next year. 2 (d) Bond that will mature in 5 years are purched. The company would like to hold them until they mature, but money has been tight recently and they may need to be sold. 2 (e) Preferred stock was purchased for its constant dividend. They company is planning to hold the preferred stock for a long time. 3 (f) A bond that matures in 10 years was purchased. The company is investing money set aside for an expansion project planned 10 years from now. 1 of 1 6/6/2006 Doran Chan Spring I '06 AMA202.0035 Prof. Angela Wu E17-6 1 of 2 6/6/2006 The information on the following page is aailable for Barkley Compnay at December 31, 2003, regarding its investments. 3,000 shares of Myers Corporation Common Stock 1,000 shares of Cole Incorporated Preferred Stock Cost 40,000 25,000 65,000 Fair Value 48,000 22,000 70,000 Instructions (a) Prepare the adjesting entry (if any) for 2003, assuming the securities are classified as trading. (b) Prepare the adjusting entry (if any) for 2003, assuming the securiteis are classified as available. (c) Discuss how the amounts reported in the financial statements are affected by the entries in (a) and (b). Journal Entry Date 12/31/06 Securities Fair Value Adjustment Trading Unrealized Holding Gain or Loss Income (a) (b) (c) 12/31 Securities Fair Value Adjustment Available for Sale Unrealized Holding Gain or Loss Equity - Debit 5,000 Credit 5,000 5,000 5,000 Securities Fair Value Adjustment Trading - account use for investment transaction. Unrealized Holding Gain or Loss Income - reported in I.S. under Other Revenues and Gains Securities Fair Value Adjustment Available for Sale - account use for investment transaction Unrealized Holding Gain or Loss Equity - increase in equity statement. Doran Chan Spring I '06 AMA202.0035 Prof. Angela Wu s. n. 2 of 2 6/6/2006 Doran Chan Spring I '06 AMA202.0035 Prof. Angela Wu E17-7 1 of 1 6/6/2006 On December 21, 2003, Tiger Company provided you with the following information regarding its trading securities. Investments Clemson Corp. stock Colorado Co. stock Buffaloes Co. stock Total of portfolio Previous securites fair value adjustment balance Securities fair value adjustment - Cr. Cost Fair Value Unrealized Gain/Loss 20,000 19,000 -1,000 10,000 9,000 -1,000 20,000 20,600 600 50,000 48,600 -1,400 0 -1,400 During 2004, Colorado Company stock was sold for $9,400. The fair value of the stock on December 31, 2004 was: Clemson Corp stock - $19,100; Buffaloes Co. stock - $20,500. Instructions (a) Prepare the adjusting journal entry needed on December 31, 2003. (b) Prepare the journal entry to record the sale of the Colorado Company stock during 2004. (c) Prepare the adjusting journal entry needed on December 31, 2004. (a) (b) (c) Date Journal Entry 12/31/03 Unrealized Holding Gain or Loss - Income Securiteis Fair Value Adjustment xx/xx/04 Cash Loss on Sale of Securities Trading Securities Investments Clemson Corp. stock Buffaloes Co. stock Total of portfolio Previous securites fair value adjustment balance Securities fair value adjustment - Dr. Debit 1,400 Credit 1,400 9,400 600 10,000 Cost Fair Value Unrealized Gain/Loss 20,000 19,100 -900 20,000 20,500 500 40,000 39,600 -400 -1,400 1,000 Date Journal Entry 12/31/04 Securiteis Fair Value Adjustment Unrealized Holding Gain or Loss - Income Debit 1,000 Credit 1,000 Doran Chan Spring I '06 E17-13 AMA202.0035 Prof. Angela Wu Parent Co. invested $1,000,000 in Sub Co. for 25% of its outstanding stock. At the time of the purchase, Sub Co. had a book value of $3,200,000. Sub Co. pays out %40 of net income in dividends each year. Instructions Use the information in the following T-account for the investment in Sub to anser the following question. Investment in Sub Co. 1,000,000 110,000 44,000 (a) (b) (c) (d) How much was Parent Co.'s share of Sub Co.'s net income for the year? How much was Parent Co.'s share of Sub Co.'s dividends for the year? What was Sub Co.'s total net income for the year? What was Sub Co.'s total dividends for the year? (a) (b) (c) (d) $110,000 increase in the investment for the year. $44,000 share of dividends for the year. $110,000 ÷ 25% = 440,000 is the total net income for the year. $440,000 x 40% = 176,000 is the total dividends for the year. 1 of 1 6/6/2006 Doran Chan Spring I '06 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 E13-2 The following are selected 2004 transactions of Sean Astin Corporation. Sept. 1 Purchased inventory from Encino Company on account for $50,000. Astin records purchases gross and uses periodic inventory system. Issued a $50,000, 12-month, 12% note to Encino in payment of account. Borrowed $50,000 from the Shore Bank by signing a 12-month, noninterest-bearing $56,000 note. Oct. 1 Oct. 1 Instructions (a) Prepare journal entries for the selected transactions above. (b) Prepare adjusting entries at December 31. (c) Compute the total net liability to be reported on the December 31 balance sheet for: (1) the interest-bearing note. (2) the non-interest-bearing note. (a) Date Sept. 1 Oct. 1 Oct. 1 (b) Dec. 31 Dec. 31 Debit 50,000 Journal Entry Purchases Accounts Payable 50,000 Accounts Payable Notes Payable 50,000 Cash Discont on Notes Payable Notes Payable 50,000 6,000 50,000 56,000 Interest Expense Interest Payable 1,500 Interest Expense Discont on Notes Payable 1,200 (c) Notes Payable Interest Payable (1) 50,000 1,500 51,500 Credit 1,500 << 50,000 x 12% x 1/4 1,200 << 6,000 x 1/4 (2) 1,500 Interest Payable 6,000 Discont on Notes Payable -4,500 56,000 Notes Payable 51,500 Doran Chan Spring I '06 E13-11 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 Sheryl Crow Equipment Company sold 500 Rollomatics during 2004 at $6,000 each. During 2004, Crow spent $20,000 servicing the 2-year warranties that accompany the Rollomatic. All applicable transactions are on a cash basis. Instructions (a) Prepare 2004 entries for Crow using expense warranty approach. Assume that Crow estimates the total cost of servicing the warranties will be $120,000 for 2 years. (b) Prepare 2004 entries for Crow assuming that the warranties are not an integral part of the sale. Assume that of the sales total, $150,000 relates to sales of warranty contracts. Crow estimates the total cost of servicing the warranties will be $120,000 for 2 years. Estimate revenues earned on the basis of costs incurred and estimated costs. (a) Date xx-xx Journal Entry Cash Debit 3,000,000 Sales xx-xx xx-xx (b) xx-xx Warranty Expense Cash Warranty Expense Estimated Liability Warranties Cash 3,000,000 << 500 x 6,000 20,000 20,000 100,000 100,000 << 120,000 - 20,000 3,000,000 Sales Unearned Warranty Revenue xx-xx xx-xx Credit 2,850,000 150,000 Warranty Expense Cash 20,000 Unearned Warranty Revenue Warranty Revenue 25,000 20,000 25,000 << (20,000 ÷ 120,000) x 150,000 Doran Chan Spring I '06 E13-12 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 Yanni Campany includes 1 coupon in each box of soap powder that it packs, and 10 coupons are redeemable for a premium (a kitchen utensil). In 2004, Yanni Company purchased 8,800 premiums at 80 cents each and sold 110,000 boxes of soap powder at $3.30 per box; 44,000 coupons were presented for redemption in 2004. It is estimated that 60% of the coupons will eventually be presented for redemption. Instruction Prepare all the entries that would be made relative to sales of soap powder and to the premium plan in 2004. Date Journal Entry Inventory Premiums Cash Debit 7,040 Cash 363,000 Credit 7,040 << 8,800 x .80 Sales 363,000 << 110,000 x 3.30 Premium Expense Inventory Premiums 3,520 Premium Expense Estimated Liability Premiums 1,760 3,520 << (44,000 ÷ 10) X $.80 1,760 << ((110,000 X 60) – 44,000) ÷ 10 X .80 Doran Chan Spring I '06 AMA202.0035 Prof. Angela Wu E13-13 Presented below are three independent situations. Answer the question at the end of each situation. 1. During 2004, Salt‐n‐Pepa Inc. became involved in a tax dispute with the IRS. Salt-n-Pepa’s attorneys have indicated that they believe it is probable that Salt-n-Pepa will lose this dispute. They also believe that Salt-n-Pepa will have to pay the IRS between $900,000 and $1,400,000. After the 2004 financial statements were issued, the case settled with the IRS for $1,200,000. What amount, if any, should be reported as a liability for this contingency as of December 31, 2004? 2. On October 1, 2004, Alan Jackson Chemical was identified as a potentially responsible party by the Environmental Protection Agency. Jackson’s management along with its counsel have concluded that it is probable that Jackson will be responsible for damages, and a reasonable estimate of these damages is $5,000,000. Jackson’s insurance policy of $9,000,000 has a deductible clause of $500,000. How should Alan Jackson Chemical report this information in its financial statements at December 31, 2004? 3. Melissa Etheridge Inc. had a manufacturing plant in Bosnia, which was destroyed in the civil war. It is not certain who will compensate Etheridge for this destruction, but Etheridge has been assured by governmental officials that it will receive a definite amount for this plant. The amount of the compensation will be less than the fair value of the plant, but more than its book value. How should the contingency be reported in the financial statements of Etheridge Inc.? 1. The company should report $900,000 as liability. 2. $500,000 should be accrued because the insurance company cover that amount. 3. Gain contingencies are not recorded. 1 of 1 6/6/2006 Doran Chan Spring I '06 E13-20 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 Jud Buechler, president of the Supporting Cast Company, has a bonus arrangement with the company under which he receives 15% of the net income (after deducting taxes and bonuses) each year. For the current year, the net income before deducting either the provision for income taxes or the bonus is $299,750. The bonus is deductible for tax purposes, and the effective tax rate may be assumed to be 40%. Intructions (a) Compute the amount of Jud Buechler’s bonus. (b) Compute the appropriate provision for federal income taxes for the year. (c) Prepare the December 31 journal entry to record the bonus (which will not be paid until next year). (a) (b) Bonus Tax Bonus Bonus Bonus Bonus 1.09 Bonus Bonus = = = = = = = .15 ($299,750 – Bonus – Tax) .40 ($299,750 – Bonus) .15 [$299,750 – Bonus – .4 ($299,750 – Bonus)] .15 ($299,750 – Bonus – $119,900 + .4 Bonus) .15 ($179,850 – .6 Bonus) 26,977.50 – .09 Bonus $26,977.50 $24,750 Tax Tax Tax Taxes = = = = .40 ($299,750 – Bonus) .40 ($299,750 – $24,750) .40 ($275,000) $110,000 Date (c) = Journal Entry Bonus Expense Bonus Payable Debit 24,750 Credit 24,750 Doran Chan Spring I '06 E14-3 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 Presented below are two independent situations. 1. On January 1, 2004, Paul Simon Company issued $200,000 of 9%, 10-year bonds at par. Interest is payable quarterly on April 1, July 1, and January 1. 2. On June 1, 2004, Graceland Company issued $100,000 of 12%, 10-year bonds dated January 1 at par plus accrued interest. Interest is payable semiannually on July 1 and January 1. Instruction For each of these two independent situations, prepare journal entries to record the following. (a) The issuance of the bonds. (b) The payment of interest on July 1. (c) The accrual of interest on December 31. Date 1/1/04 Cash Paul Simon Company Journal Entry Debit 200,000 Bond 7/1/04 Bond Interest Expense Cash 12/31/04 Bond Interest Expense Interest Payable Date 6/1/04 Cash Graceland Company Journal Entry 200,000 4,500 4,500 << 200,000 x .09 x 1/4 4,500 4,500 Debit 105,000 Bond Bond Interest Expense 7/1/04 Bond Interest Expense Cash 12/31/04 Bond Interest Expense Interest Payable Credit Credit 100,000 5,000 << 100,000 x .12 x 5/12 6,000 6,000 << 100,000 x .12 x 1/2 6,000 6,000 Doran Chan Spring I '06 E14-4 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 Celine Dion Company issued $600,000 of 10%, 20-year bonds on January 1, 2005, at 102. Interest is payable semiannually on July 1 and January 1. Dion Company uses the straight-line method of amortization for bond premium or discount. Instructions Prepare the journal entries to record the following. (a) The issuance of the bonds. (b) The payment of interest and the related amortization on July 1, 2005. (c) The accrual of interest and the related amortization on December 31, 2005. Date 1/1/05 Cash Journal Entry Debit 612,000 Bonds Payable Premium on Bonds Payable 7/1/05 Premium on Bonds Payable Bond Interest Expense Cash 12/31/05 Premium on Bonds Payable Bond Interest Expense Bonds Interest Payable Credit 600,000 12,000 << 600,000 x 1.2 29,700 300 << 12,000 ÷ 40 30,000 << 600,000 x .1 x 1/2 29,700 300 30,000 Doran Chan Spring I '06 E14-10 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 On January 1, 2004, Aumont Company sold 12% bonds having a maturity value of $500,000 for $537,907.37, which provides the bondholders with a 10% yield. The bonds are dated January 1, 2009, and mature January 1, 2009, with interest payable December 31 of each year. Aumont Company allocates interest and unamortized discount or premium on the effective interest basis. Instructions (a) Prepare the journal entry at the date of the bond issuance. (b) Prepare a schedule of interest expense and bond amortization for 2004-2006. (c) Prepare the journal entry to record the interest payment and the amortization for 2004. (d) Prepare the journal entry to record the interest payment and the amortization for 2006. (b) Date 1/1/04 12/31/04 12/31/05 12/31/06 (a) Bond Amortization Table 12% Bonds Sold to Yield 10% Interest Bond Cash Expense Premium 60,000.00 60,000.00 60,000.00 Date 1-Jan-04 Cash 53,790.74 53,169.81 52,486.79 6,209.26 6,830.19 7,513.21 Journal Entry Carrying Value 537907.37 531698.11 524867.92 517354.71 Debit 537,907.37 Premium Bonds Payable Bonds Payable (c) (d) Credit 37,907.37 500,000 31-Dec-04 Bonds Interest Expense Premium Bonds Payable Cash 53,790.74 6,209.26 31-Dec-06 Bonds Interest Expense Premium Bonds Payable Cash 52,486.79 7,513.21 60,000 60,000 Doran Chan Spring I '06 E14-12 AMA202.0035 Prof. Angela Wu 1 of 1 6/6/2006 On January 2, 1999, Banno Corporation issued $1,500,000 of 10% bonds at 97 due December 31, 2008. Legal and other costs of $24,000 were incurred in connection with the issue. Interest on the bonds is payable annually each December 31. The $24,000 issue costs are being deferred and amortized on a straight-line basis over the 10-year term of the bonds. The discount on the bonds is also being amortized on a straight-line basis over the 10 years. (Straight-line is not materially different in effect from the preferable “interest method”.) The bonds are callable at 101 (i.e., at 101% of face amount), and on January 2, 2004, Banno called $900,000 of the bonds and retired them. Instructions Ignoring income taxes, compute the amount of loss, if any, to be recognized by Banno as a result of retiring the $900,000 of bonds in 2004 and prepare the journal entry to record the retirement. Reacquisition price Net carrying amount of bonds redeemed: Par value Unamortized discount Unamortized bond issue costs Loss on redemption 909,000 << 900,000 x 1.01 900,000 -13,500 -7,200 879,300 29,700 Unamortized discount Original amount of discount: 900,000 x .03 = 27,000 ÷ 10 = 2,700 amortization per year Amount of discount unamortized: 2,700 x 5 = 13,500 Unamortized issue costs Original amount of costs: 24,000 x 900,000 ÷ 1,500,000 = 14,400 ÷ 10 = 1,440 amortization per yr Amount of costs unamortized: 1,440 x 5 = 7,200 Date Journal Entry 2-Jan-04 Bonds Payable Loss on Redemption of Bonds Unamortized Bond Issue Cost Discount on Bonds Payable Cash Debit 900,000 29,700 Credit 7,200 13,500 909,000