CHAPTER 14 Non-Current Liabilities

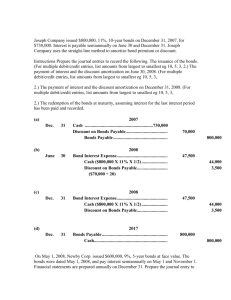

advertisement