Chapter 7

Chapter 7, Solutions Cornett, Adair, and Nofsinger

CHAPTER 7 – Valuing Stocks

Questions

LG1 1. As owners, what rights and advantages do shareholders obtain?

They are able to participate in the economic growth of publicly traded firms without having to manage business entities directly. They have the right to residual cash flows of corporate profits and often receive some of these cash flows through dividends. In addition, shareholders vote on the members for board of directors and other proposals for the company. Shareholder capital losses are capped in that they can only lose their initial investment. Stocks are very liquid and investors can enjoy this liquidity in both their entrance into the stock market and their exit from it.

LG1 2. Describe how being a residual claimant can be very valuable.

Residual claimant’s are able to delegate the operations of the firm to professional managers, enjoying the possibly vast gains in value that can be created by some firms over time.

LG2 3. Obtain a current quote of McDonald’s (MCD) from the Internet. Describe what has changed since the quote in Figure 8.1.

As of November 23, 2007, MCD’s stock price had increased in value to $57.72 per share.

MCD experienced a modest loss from July 11, 2007 reaching a trough in mid-August

2007 at approximately $47.50 per share. Since that time, it has generally trended upward through the Fall of 2007.

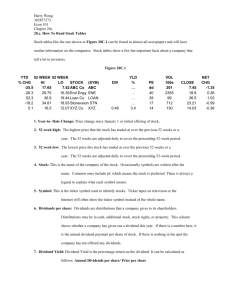

LG2 4. Get the trading statistics for the three main U.S. stock exchanges. Compare the trading activity to that of Table 8.1.

The table below reflects trading activity on the three main U.S. stock exchanges for

November 26, 2007. Trading volume was particularly high this day compared to the July

11, 2007 activity reflected in Table 8.1. Continued concerns over the home mortgage crises built into a selling frenzy in the markets with the DJIA plummeting 240 points on this day. Volume was also up due to this trading day immediately following the

Thanksgiving holiday weekend, since markets were closed the previous Thursday and only light trading volume was experienced in the lightly attended trading session the day after Thanksgiving.

7-1

Chapter 7, Solutions Cornett, Adair, and Nofsinger

ADVANCES & DECLINES

Advancing Issues

Declining Issues

Unchanged Issues

Total Issues

New Highs

New Lows

NYSE

834 (24%)

2,565 (74%)

64 (2%)

3,463

45

340

AMEX

451 (33%)

824 (60%)

96 (7%)

1,371

48

128

NASDAQ

782 (25%)

2,248 (72%)

104 (3%)

3,134

54

286

Up Volume

Down Volume

Unchanged Volume

463,831,873 (13%) 102,173,146 (13%) 339,948,056 (17%)

3,149,651,823 (86%) 667,962,524 (86%) 1,599,678,727 (82%)

38,646,084 (1%) 8,138,296 (1%) 8,948,642 (0%)

Total Volume 3,652,129,780 1 778,273,966 1 1,948,575,425 1

LG3 5. Why might the Standard & Poor’s 500 Index be a better measure of stock market performance than the Dow Jones Industrial Average? Why is the DJIA more popular than the S&P 500?

The S&P 500 is a broad market index that includes stocks of the 500 largest US firms from ten sectors of the economy. It captures 80% of the overall stock market capitalization and is a good proxy for what is occurring in the overall stock market. The

DJIA has been used for a longer period, since the mid-1880’s, and represents the activity of the 30 largest corporations in the US, covering 30% of the stock market. Its popularity arises from it being the first index used by the media.

LG3 6. Explain how it is possible for the DJIA to increase one day while the Nasdaq

Composite decreases during the same day.

The components of the DJIA and the Nasdaq Composite index are mostly different companies. The DJIA includes the 30 industry leaders across all sectors of the economy.

The Nasdaq is comprised of predominantly technology related firms and emits a noisy signal of technology performance on any given day.

LG4 7. Which is higher, the ask quote or the bid quote? Why?

7-2

Chapter 7, Solutions Cornett, Adair, and Nofsinger

The market maker’s ask price is the lowest price offered for stock sale and the bid price is the highest price a market maker will pay for stock purchase. Thus, the ask price is higher than the bid price. The difference is the bid-ask spread and it represents the gain a market maker achieves by taking the risk position and providing the needed liquidity for the stock in question.

LG4 8. Illustrate through examples how trading commission costs impact an investor’s return.

Assume an investor wishes to purchase a stock at a strike price of $90. Two scenarios to consider, at their extremes, would be the purchase of 10 shares versus the purchase of 100 shares. The costs to purchase through a discount broker, assuming the broker charges $20 per trade would be $920 ($900 + $20) and $9020, respectively. The commission for the trades in percentages would be 2.22% and 0.22%, respectively. For the investor who owns only 10 shares, the price would have to rise by $2 per share to recoup the commission cost. It would only have to rise 20¢ for the investor who owns 100 shares. It is evident that the percentage of trading commissions is lower on larger volume trades and the effect would be even more pronounced if the trades had been placed through a retail broker.

LG4 9. Describe the difference in the timing of trade execution and the certainty of trade price between market orders and limit orders.

Market makers fill market orders immediately at the current stock price. This provides the liquidity an investor needs to buy and sell stocks quickly. However, the price at which the stock will fill cannot be guaranteed. With limit orders, the market maker will only fill the order when the stated price is reached. This means that you can count on the execution only after your target buy or sell price is reached, but you cannot guarantee your trade will execute with a limit order.

LG5 10. What are the differences between common stock and preferred stock?

Common stock dividends change over time, hopefully increasing in the long-term.

Preferred stock pays a constant dividend. Preferred stockholders have higher precedence for payment in the event of firm liquidation from bankruptcy. However, preferred stockholders do not have voting rights that common stock holders enjoy. Preferred stock prices fluctuate with market interest rates and behave like corporate bond prices.

Common stock price changes with the value of the company’s underlying business.

LG5 11. How important is growth to a stock’s value? Illustrate with examples.

Consider two firms with a common next period dividend of $1, a common market discount rate of 8%, but differing growth rates of 3% and 5%, respectively. The implied current prices of these stocks are $20 [=$1/(0.08-0.03)] and $33.33 [=$1/(0.08-0.05)] respectively. The firm with higher growth prospects (5%) is valued more highly than the firm with lower growth rate prospects (3%).

7-3

Chapter 7, Solutions Cornett, Adair, and Nofsinger

LG5 12. Under what conditions would the constant growth rate model not be appropriate?

When the growth rate exceeds the discount rate, the constant growth rate model cannot be employed. It is also not appropriate when the growth rate cannot reasonably be expected to be constant into the future.

LG5 13. The expected return derived from the constant growth rate model relies on dividend yield and capital gain. Where do these two parts of the return come from?

Rearranging the terms and solving for the i from the constant growth model yields the expected return model. The components are the dividend yield and the capital gain. The dividend yield reflects the percentage return from current firm operations. The capital gain captures the firm’s future growth prospects. Both components are important from an investor point of view, with dividends providing income to an investor over the stock holding period and the capital gain being realized at the time of stock sale.

LG6 14. Describe, in words, how to use the variable growth rate technique to value a stock.

When the firm is growing at a very fast pace in its infancy, the expected growth rate will initially be very large. This rate should be used for the high growth period, but a terminal growth rate should be employed for valuation when the firm matures. Essentially, a firm cannot grow faster than the general economy indefinitely and must be capped in the long term by its mature growth rate.

LG6 15. Can the variable growth rate model be used to value a firm that has a negative growth rate in Stage 1 and a stable and positive growth in Stage 2? Explain.

In this case, the firm would be contracting over a short period and then reaching a stable, positive growth rate. Insofar as the initial rate during contraction does not dominate the later mature growth rate, this is possible. It would suggest that a firm’s dividends in the short term decreased, followed by a positive dividend stream in the longer term.

LG7 16. Explain why using the P/E relative value approach may be useful for companies that do not pay dividends.

Since dividends are non-existent, the forecast stock price is simply a function of current price and the discount rate. In isolation, it is hard to determine if the firm is under or overvalued based on this information only. Using the P/E relative value approach, the trailing P/E can be calculated and compared to a firm’s competitors.

LG7 17. How is a firm’s changing P/E ratio reflected in the stock price? Give examples.

The P/E ratio multiplied by a firm’s earnings result in the stock price. For example, if a firm is experiencing high growth and all other factors are held constant, this will lead to a

7-4

Chapter 7, Solutions Cornett, Adair, and Nofsinger higher P/E ratio reflecting the growth prospects. Stock prices can change simply because the market changes the P/E ratio appropriate for that stock.

LG7 18. Differentiate the characteristics of growth stocks and value stocks?

Taken in tandem, P/E ratios and growth rates illustrate the type of stock the firm is characterized by, growth or income. Firms with high P/E and high growth rates are growth stocks. A comparison across an industry of P/E ratios can be an aid to investors in selecting the best growth stock to purchase. By contrast, firms with low P/E ratios and low growth rates tend to be value stocks.

LG7 19. What’s the relationship between the P/E ratio and a firm’s growth rate?

The price of a stock can be modeled with the constant growth rate equation. Note that the denominator is ( i – g ). So the price relative to earnings is impacted by the growth rate of the firm. A high growth rate will cause a high price and P/E. Thus, high growth firms should have high P/E ratios while low growth rate firms should have low P/E ratios.

LG7 20. Describe the process for using the P/E ratio to estimate a future stock price.

Using current earnings and an expected growth rate for these earnings, the current P/E ratio can be multiplied by the estimate of future earnings to produce a price estimate for the future stock value. That is, the current P/E ratio acts as a guide for the stock’s future price. This approach should be employed cautiously by comparing the P/E ratios to similar firms to ensure that the firm you have selected has a reasonable P/E ratio.

LG3

Problems

Basic

Problems 7-1 Stock Index Performance On January 16, 2007, the Dow Jones Industrial Average set a new high. The index closed at 12,582.59, which was up 26.51 that day. What was the return (in percent) of the stock market that day?

FV = PV × (1 + i)

12,582.59 = (12,582.59-26.51) × (1 + i) i = (12,582.59/12,556.08)-1 = 0.2111%

LG3 7-2 Stock Index Performance On January 16, 2007, the Standard & Poor’s 500 Index reached the highest it had been since 2000. The index closed at 1,431.90, which was up

1.17 that day. What was the return (in percent) of the stock market that day?

FV = PV × (1 + i)

1,431.90 = (1,431.9-1.17) × (1 + i) i = (1.431.90/1,430.73)-1 = 0.08178%

7-5

Chapter 7, Solutions Cornett, Adair, and Nofsinger

LG4 7-3 Buying Stock with Commissions At your discount brokerage firm, it costs $8.95 per stock trade. How much money do you need to buy 200 shares of Pfizer, Inc. (PFE), which trades at $27.22?

($27.22/share × 200 shares) + $8.95 = $5,452.95

LG4 7-4 Buying Stock with Commissions At your discount brokerage firm, it costs $9.50 per stock trade. How much money do you need to buy 300 shares of Time Warner, Inc.

(TWX), which trades at $22.62?

($22.62/share × 300 shares) + $9.50 = $6,795.50

LG4 7-5 Selling Stock with Commissions At your full-service brokerage firm, it costs $120 per stock trade. How much money do you receive after selling 150 shares of Nokia

Corporation (NOK), which trades at $20.13?

($20.13/share × 150 shares) - $120 = $2,899.50

LG4 7-6 Selling Stock with Commissions At your full-service brokerage firm, it costs $135 per stock trade. How much money do you receive after selling 250 shares of International

Business Machines (IBM), which trades at $96.17?

($96.17/share × 250 shares) - $135 = $23,907.50

LG4 7-7 Buying Stock with a Market Order You would like to buy shares of Sirius Satellite

Radio (SIRI). The current ask and bid quotes are $3.96 and $3.93 respectively. You place a market buy-order for 500 shares that executes at these quoted prices. How much money did it cost to buy these shares?

($3.96/share × 500 shares) = $1,980.00

LG4 7-8 Buying Stock with a Market Order You would like to buy shares of Coldwater

Creek, Inc. (CWTR). The current ask and bid quotes are $20.70 and $20.66 respectively.

You place a market buy-order for 200 shares that executes at these quoted prices. How much money did it cost to buy these shares?

($20.70/share × 200 shares) = $4,140.00

LG4 7-9 Selling Stock with a Limit Order You would like to sell 200 shares of WorldSpace,

Inc. (WRSP). The current ask and bid quotes are $4.66 and $4.62 respectively. You place a limit sell-order at $4.65. If the trade executes, how much money do you receive from the buyer?

($4.65/share × 200 shares) = $930.00

7-6

Chapter 7, Solutions Cornett, Adair, and Nofsinger

LG4 7-10 Selling Stock with a Limit Order You would like to sell 100 shares of eCollege.com (ECLG). The current ask and bid quotes are $15.33 and $15.28 respectively. You place a limit sell-order at $15.31. If the trade executes, how much money do you receive from the buyer?

($15.31/share ×100 shares) = $1,531.00

LG5 7-11 Value of a Preferred Stock A preferred stock from Duquesne Light Company

(DQUPRA) pays $2.10 in annual dividends. If the required return on the preferred stock is 5.4 percent, what’s the value of the stock?

Use equation 7-6, noting that for preferred stock, the growth rate g equals zero:

Constant growth model

P

0

D

0 i

1

g

g

$ 2 .

10

0 .

054

0

$ 38 .

89

LG5 7-12 Value of a Preferred Stock A preferred stock from Hecla Mining Co. (HLPRB) pays $3.50 in annual dividends. If the required return on the preferred stock is 6.8 percent, what is the value of the stock?

Use equation 7-6, noting that for preferred stock, the growth rate g equals zero:

Constant growth model

P

0

D

0 i

1

g

g

$ 3 .

50

0 .

068

0

$ 51 .

47

LG7 7-13 P/E Ratio and Stock Price Ultra Petroleum (UPL) has earnings per share of $1.56 and a P/E ratio of 32.48. What’s the stock price?

Use equation 7-10:

P n

E n

E n

32 .

48

1 .

56

$ 50 .

67

LG7 7-14 P/E Ratio and Stock Price JP Morgan Chase Co. (JPM) has earnings per share of

$3.53 and a P/E ratio of 13.81. What is the price of the stock?

Use equation 7-10:

P n

E n

E n

13 .

81

3 .

53

$ 48 .

75

Intermediate

Problems 7-15 Value of Dividends and Future Price A firm is expected to pay a dividend of $1.35

LG5 next year and $1.50 the following year. Financial Analysts believe the stock will be at their price target of $75 in two years. Compute the value of this stock with a required return of 11.5 percent.

7-7

Chapter 7, Solutions Cornett, Adair, and Nofsinger

Use equation 7-3:

P

0

D

1

1

i

D

2

i

P

2

2

1 .

35

1

0 .

115

1 .

50

1

75 .

00

0 .

115

2

$ 62 .

74

LG5 7-16 Value of Dividends and Future Price A firm is expected to pay a dividend of $2.05 next year and $2.35 the following year. Financial Analysts believe the stock will be at their price target of $110 in two years. Compute the value of this stock with a required return of 12 percent.

Use equation 7-3:

P

0

D

1

1

i

D

2

P

2

2

2 .

05

1

0 .

12

2 .

35

1

110

0 .

12

.

00

2

$ 91 .

40

LG5 7-17 Dividend Growth Annual dividends of AT&T Corp (T) grew from $0.96 in 2000 to

$1.33 in 2006. What was the annual growth rate?

Use equation 4-2:

Future value in 6 years

1 .

33

0 .

96

1

g

6 g

5 .

58 %

LG5 7-18 Dividend Growth Annual dividends of General Electric (GE) grew from $0.66 in

2001 to $1.03 in 2006. What was the annual growth rate?

Use equation 4-2:

Future value in 5 years

1 .

03

0 .

66

1

g

5 g

9 .

31 %

LG5 7-19 Value a Constant Growth Stock Financial analysts forecast Safeco Corp. (SAF) growth for the future to be 10 percent. Safeco’s recent dividend was $1.20. What is the value of Safeco stock when the required return is 12 percent?

Use equation 7-6:

Constant growth model

P

0

D

0

1

i

g g

$ 1 .

20

1

0 .

10

0 .

12

0 .

10

$ 66 .

00

LG5 7-20 Value a Constant Growth Stock Financial analysts forecast Limited Brands (LTD) growth for the future to be 12.5 percent. LTD’s recent dividend was $0.60. What is the value of Limited Brands stock when the required return is 14.5 percent?

Use equation 7-6:

Constant growth model

P

0

D

0

1

i

g g

$ 0 .

60

1

0 .

125

0 .

145

0 .

125

$ 33 .

75

7-8

Chapter 7, Solutions Cornett, Adair, and Nofsinger

LG5 7-21 Expected Return Ecolap Inc. (ECL) recently paid a $0.46 dividend. The dividend is expected to grow at a 14.5 percent rate. At a current stock price of $44.12, what is the return shareholders are expecting?

First convert D

0

to D

1

by $0.46×(1+0.145) = $0.527. Then use equation 7-7:

Expected return

i

D

1

P

0

g

( 0 .

527 / 44 .

12 )

0 .

145

15 .

69 %

LG5 7-22 Expected Return Paychex Inc. (PAYX) recently paid a $0.84 dividend. The dividend is expected to grow at a 15 percent rate. At a current stock price of $40.11, what is the return shareholders are expecting?

First convert D

0

to D

1

by $0.84×(1+0.15) = $0.966. Then use equation 7-7:

Expected return

i

D

1

P

0

g

( 0 .

966 / 40 .

11 )

0 .

15

17 .

41 %

LG6 7-23 Dividend Initiation and Stock Value A firm does not pay a dividend. It is expected to pay its first dividend of $0.20 per share in 3 years. This dividend will grow at

11 percent indefinitely. Using a 12 percent discount rate, compute the value of this stock.

First compute the year 2 value of the stock using equation 7-6 and then discount this back two years to get the present value of the stock price:

Constant growth model

P

2

i

D

3

g

$ 0 .

20 /( 0 .

12

0 .

11 )

$ 20 .

00

P

0

( 20 / 1 .

12

2

)

$ 15 .

94

LG6 7-24 Dividend Initiation and Stock Value A firm does not pay a dividend. It is expected to pay its first dividend of $0.25 per share in 2 years. This dividend will grow at

10 percent indefinitely. Using a 11.5 percent discount rate, compute the value of this stock.

First compute the year 1 value of the stock using equation 7-6 and then discount this back one year to get the present value of the stock price:

Constant growth model

P

1

i

D

2

g

P

0

( 16 .

67 / 1 .

115 )

$ 14 .

95

$ 0 .

25 /( 0 .

115

0 .

10 )

$ 16 .

67

LG7 7-25 P/E Ratio Model and Future Price Kellogg Co. (K) recently earned a profit of

$2.52 earnings per share and has a P/E ratio of 19.86. The dividend has been growing at a

5 percent rate over the past few years. If this growth rate continues, what would be the

7-9

Chapter 7, Solutions Cornett, Adair, and Nofsinger stock price in five years if the P/E ratio remained unchanged? What would the price be if the P/E ratio declined to 15 in five years?

Under these two scenarios, the future price estimates using equation 7-10 are:

P

5

E n

E

0

1

g

n

19 .

86

$ 2 .

52

1

0 .

05

5

$ 63 .

87

P

5

E n

E

0

1

g

n

15

$ 2 .

52

1

0 .

05

5

$ 48 .

24

LG7 7-26 P/E Ratio Model and Future Price New York Times Co. (NYT) recently earned a profit of $1.21 earnings per share and has a P/E ratio of 19.59. The dividend has been growing at a 7.25 percent rate over the past six years. If this growth rate continues, what would be the stock price in five years if the P/E ratio remained unchanged? What would the price be if the P/E ratio increased to 22 in five years?

Under these two scenarios, the future price estimates using equation 7-10 are:

P

5

E n

E

0

1

g

n

19 .

59

$ 1 .

21

1

0 .

0725

5

$ 33 .

64

P

5

E n

E

0

1

g

n

22

$ 1 .

21

1

0 .

0725

5

$ 37 .

77

Advanced

Problems 7-27 Value of Future Cash Flows A firm recently paid a $0.45 annual dividend. The

LG5 dividend is expected to increase by 10 percent in each of the next four years. In the fourth year, the stock price is expected to be $80. If the required return for this stock is 13.5 percent, what is its value?

Find the dividends in the next four years:

D1 = $0.45 × (1 + 0.10) = $0.495

D2 = $0.495 × (1 + 0.10) = $0.5445

D3 = $0.5445 × (1 + 0.10) = $0.599

D4 = $0.599 × (1 + 0.10) = $0.659

Then use equation 7-3 as:

P

0

D

1

1

i

D

2

D

3

3

D

4

P

4

4

0 .

495 / 1 .

135

0 .

5445 / 1 .

135

2

0 .

599 / 1 .

135

3

( 0 .

659

80 ) / 1 .

135

4

$ 49 .

87

LG5 7-28 Value of Future Cash Flows A firm recently paid a $0.60 annual dividend. The dividend is expected to increase by 12 percent in each of the next four years. In the fourth year, the stock price is expected to be $110. If the required return for this stock is 14.5 percent, what is its value?

7-10

Chapter 7, Solutions Cornett, Adair, and Nofsinger

Find the dividends in the next four years:

D1 = $0.60 × (1 + 0.12) = $0.672

D2 = $0.672 × (1 + 0.12) = $0.753

D3 = $0.753 × (1 + 0.12) = $0.843

D4 = $0.843 × (1 + 0.12) = $0.944

Now use equation 7-3:

P

0

D

1

1

i

D

2

i

2

D

i

3

3

D

4

P

4

4

0 .

672 / 1 .

145

0 .

753 / 1 .

145

2

0 .

843 / 1 .

145

3

( 0 .

944

110 ) / 1 .

145

4

$ 66 .

27

LG5 7-29 Constant Growth Stock Valuation Walgreen Co. (WAG) paid a $0.137 dividend per share in 2000, which grew to $0.286 in 2006. This growth is expected to continue.

What is the value of this stock at the beginning of 2007 when the required return is 13.7 percent?

First calculate the growth rate from 2000 to 2006:

FV = PV × (1 + g) 6

0.286 = (0.137) × (1 + g) 6 g = (0.286/0.137)

1/6

-1 = 0.1305

Now, use this growth rate in equation 7-6 to get obtain the present value of the stock:

Constant growth model

P

0

D

0 i

1

g

g

$ 0 .

286

( 1 .

1305 ) /( 0 .

137

0 .

1305 )

$ 49 .

74

LG5 7-30 Constant Growth Stock Valuation Campbell Soup Co. (CPB) paid a $0.632 dividend per share in 2003, which grew to $0.76 in 2006. This growth is expected to continue. What is the value of this stock at the beginning of 2007 when the required return is 8.7 percent?

First calculate the growth rate from 2003 to 2006:

FV = PV × (1 + g) 3

0.76 = (0.632) × (1 + g) 3 g = (0.76/0.632)

1/3

-1 = 0.0634

Now, use this growth rate in equation 7-6 to get obtain the present value of the stock:

Constant growth model

P

0

D

0 i

1

g

g

$ 0 .

76

( 1 .

0634 ) /( 0 .

087

0 .

0634 )

$ 34 .

25

LG5 7-31 Changes in Growth and Stock Valuation Consider a firm that had been priced using a 10 percent growth rate and a 12 percent required return. The firm recently paid a

7-11

Chapter 7, Solutions Cornett, Adair, and Nofsinger

$1.20 dividend. The firm has just announced that because of a new joint venture, it will likely grow at a 10.5 percent rate. How much should the stock price change (in dollars and percentage)?

Use equation 7-6 to calculate the firm’s value prior to the venture:

Constant growth model

P

0

D

0

1

g

i

g

$ 1 .

20

( 1 .

10 ) /( 0 .

12

0 .

10 )

$ 66 .

00

If the firm’s growth rate changes to 10.5%, then the new stock price is:

Constant growth model

P

0

D

0

1

g

i

g

$ 1 .

20

( 1 .

105 ) /( 0 .

12

0 .

105 )

$ 88 .

40

The dollar amount of this change is $88.40 - $66.00 = $22.40 or 33.93% for the 0.5% increase to the growth rate.

LG5 7-32 Changes in Growth and Stock Valuation Consider a firm that had been priced using a 11.5 percent growth rate and a 13.5 percent required return. The firm recently paid a $1.50 dividend. The firm has just announced that because of a new joint venture, it will likely grow at a 12 percent rate. How much should the stock price change (in dollars and percentage)?

Use equation 7-6 to calculate the firm’s value prior to the venture:

Constant growth model

P

0

D

0

1

g

i

g

$ 1 .

50

( 1 .

115 ) /( 0 .

135

0 .

115 )

$ 83 .

63

If the firm’s growth rate changes to 12%, then the new stock price is:

Constant growth model

P

0

D

0

1

g

i

g

$ 1 .

50

( 1 .

12 ) /( 0 .

135

0 .

12 )

$ 112 .

00

The dollar amount of this change is $112.00-$83.63 = $28.37 or 33.92% for the 0.5% increase to the growth rate.

LG6 7-33 Variable Growth A fast growing firm recently paid a dividend of $0.35 per share.

The dividend is expected to increase at a 20 percent rate for the next 3 years. Afterwards, a more stable 12 percent growth rate can be assumed. If a 13 percent discount rate is appropriate for this stock, what is its value?

Use equation 7-8:

7-12

Chapter 7, Solutions Cornett, Adair, and Nofsinger

P

0

P

0

P

0

D

0

1

0 .

35

1

1

1

i

g

1

0 .

20

0 .

13

D

0

1

g

1

2

2

D

0

0 .

35

1

1

0 .

20

0 .

13

2

2

1

g

1

3

0 .

35

1

D

0

i

1

g

1

1

g

2

i

g

2

3

0 .

20

3

1

0 .

35

1

0 .

13

0 .

13

3

0 .

20

1

0 .

12

0 .

12

0 .

372

0 .

395

47 .

36

$ 48 .

13

LG6 7-34 Variable Growth A fast growing firm recently paid a dividend of $0.40 per share.

The dividend is expected to increase at a 25 percent rate for the next 4 years. Afterwards, a more stable 11 percent growth rate can be assumed. If a 12.5 percent discount rate is appropriate for this stock, what is its value?

Use equation 7-8:

P

0

P

0

D

0

1

1

i g

1

D

0

1

g

1

2

2

0 .

40

1

1

0 .

25

0 .

125

0 .

444

0 .

494

0 .

549

0 .

40

1 .

25

1 .

125

2

2

D

0

1

g

1

3

3

0 .

40

1 .

25

1 .

125

45 .

725

$ 47 .

21

3

3

D

0

1

g

1

4

0 .

40

1 .

25

4

D

0

1

g

1

1

g

2

i

g

2

4 i

0 .

40

1 .

25

1

0 .

125

1 .

125

4

0 .

11

0 .

11

LG5 7-35 P/E Model and Cash Flow Valuation Suppose that a firm’s recent earnings per

LG7 share and dividend per share are $2.50 and $1.30, respectively. Both are expected to grow at 8 percent. However, the firm’s current P/E ratio of 22 seems high for this growth rate.

The P/E ratio is expected to fall to 18 within five years. Compute a value for this stock by first estimating the dividends over the next five years and the stock price in five years.

Then discount these cash flows using a 10 percent required rate.

Find the dividends in the next four years:

D1 = $1.30 × (1 + 0.08) = $1.404

D2 = $1.404 × (1 + 0.08) = $1.516

D3 = $1.516 × (1 + 0.08) = $1.638

D4 = $1.638 × (1 + 0.08) = $1.769

D5 = $1.769 × (1 + 0.08) = $1.910

Next, use equation 7-10 to calculate the stock price in year 5:

P

5

E

5

E

5

E

5

E

0

1

g

5

18

$ 2 .

50

( 1 .

08 )

5

$ 66 .

12

Now find the present value of these cash flows using a 10% discount rate to get P

0

:

7-13

Chapter 7, Solutions Cornett, Adair, and Nofsinger

P

0

D

1

1

i

D

i

2

2

D

3

i

3

D

i

4

4

D

5

P

5

5

1 .

404 / 1 .

10

1 .

516 / 1 .

10 2

1 .

638 / 1 .

10 3

1 .

769 / 1 .

10 4

( 1 .

910

66 .

12 ) / 1 .

10 5

$ 47 .

21

LG5 7-36 P/E Model and Cash Flow Valuation Suppose that a firm’s recent earnings per

LG7 share and dividend per share are $2.75 and $1.60, respectively. Both are expected to grow at 9 percent. However, the firm’s current P/E ratio of 23 seems high for this growth rate.

The P/E ratio is expected to fall to 19 within five years. Compute a value for this stock by first estimating the dividends over the next five years and the stock price in five years.

Then discount these cash flows using an 11 percent required rate.

Find the dividends in the next four years:

D1 = $1.60 × (1 + 0.09) = $1.744

D2 = $1.744 × (1 + 0.09) = $1.901

D3 = $1.901 × (1 + 0.09) = $2.072

D4 = $2.072 × (1 + 0.09) = $2.258

D5 = $2.258 × (1 + 0.09) = $2.462

Next, use equation 7-10 to calculate the stock price in year 5:

P

5

E

5

E

5

E

5

E

0

1

g

5

19

$ 2 .

75

( 1 .

09 ) 5

$ 80 .

39

Now find the present value of these cash flows using an 11% discount rate to get P

0

:

P

0

D

1

1

i

D

2

i

2

D

i

3

3

D

i

4

4

D

5

P

5

5

1 .

744 / 1 .

11

1 .

901 / 1 .

11 2

2 .

072 / 1 .

11 3

2 .

258 / 1 .

11 4

( 2 .

462

80 .

39 ) / 1 .

11 5

$ 55 .

29

7-37 Excel Problem Spreadsheets are especially useful for computing stock value under different assumptions. Consider a firm that is expected to pay the following dividends:

Year 1 2 3 4 5 6

$1.20 $1.20 $1.50 $1.50 $1.75 $1.90 and grow at 5% thereafter

A. Using an 11 percent discount rate, what would be the value of this stock?

B. What is the value of the stock using a 10 percent discount rate? A 12 percent discount rate?

C. What would the value be using a 6% growth rate after Year 6 instead of the 5% rate using each of these three discount rates?

D. What do you conclude about stock valuation and its assumptions?

SOLUTION:

7-14

Chapter 7, Solutions Cornett, Adair, and Nofsinger

Year

1

2

3

4

5

6

6 @ 11%

6 @ 10%

6 @ 12%

At 5% growth

Dividend

$1.20

$1.20

$1.50

$1.50

$1.75

$1.90

Terminal Price

$33.25

$39.90

$28.50

Sum =

11%

Discount

Rate

$1.08

$0.97

$1.10

$0.99

$1.04

$1.02

$17.78

$23.97

Year

1

2

3

4

5

6

6 @ 11%

6 @ 10%

6 @ 12%

At 6% growth

Dividend

$1.20

$1.20

$1.50

$1.50

$1.75

$1.90

Terminal Price

$40.28

$50.35

$33.57

11%

Discount

Rate

$1.08

$0.97

$1.10

$0.99

$1.04

$1.02

$21.54

Sum = $27.73

Present

Value

10%

Discount

Rate

$1.09

$0.99

$1.13

$1.02

$1.09

$1.07

$22.52

12%

Discount

Rate

$1.07

$0.96

$1.07

$0.95

$0.99

$0.96

$14.44

$28.92 $20.44

Present

Value

10%

Discount

Rate

$1.09

$0.99

$1.13

$1.02

$1.09

$1.07

$28.42

12%

Discount

Rate

$1.07

$0.96

$1.07

$0.95

$0.99

$0.96

$17.01

$34.81 $23.01

A.

From the table calculated in Excel, the value of the stock based on an 11% discount rate would be $23.97.

B.

From the table, the value of the stock based on a 10% discount rate would be

$28.92 and based on a 12% discount rate would be $20.44.

C.

From the table, the value of the stock that grows at 6% (rather than 5%) in year 7 and after causes a higher stock value than a future 5% growth.

7-15

Chapter 7, Solutions Cornett, Adair, and Nofsinger

D.

Assumptions are crucially important in stock valuation. Minor changes in either the discount rate or the growth assumption rate can have big impact on stock valuation.

Research It

Stock Screener

Investors can choose from many thousands of stocks. The large number to choose from can be quite daunting to new investors. Fortunately, some good stock screeners are available for free on the Internet that will find only the kinds of companies the investor is looking for. Looking for small value companies? A stock screen at Yahoo! Finance will show all the stocks that meet the three criteria of (1) market capitalization between $250 million and $1 billion, (2) P/E ratio less than or equal to 10, and (3) a quick ratio greater or equal to 1.0. In January of 2007, 86 firms met all three of these criteria. Yahoo! Finance provides 19 screens like this one to choose from. Pick one of these pre-set screens.

Discuss the kinds of stocks the screen will find and report on those companies.

(http://screener.finance.yahoo.com/presetscreens.html)

SOLUTION: Consider the preset screen for Large Cap Value. The stock screener description is as follows:

Stocks with market capitalizations greater than or equal to $5 billion with a priceearnings ratio less than or equal to 15 and a quick ratio of greater than or equal to 1.0

Selecting this prescreen yields many of the big, mature firms you would expect, such as

ExxonMobil (XOM), Pfizer, Inc. (PFE), Goldman Sachs (GS) and Fedex Corp (FDX).

These are mature firms in their industry that command very large capitalization ($417 billion for XOM) and are favored investments for larger institutional investors. These firms tends to be leaders in their industry and offer an attractive stream of dividends for their investors.

Integrated Mini Case: Valuing Carnival Corporation

Carnival Corp. provides cruises to major vacation destinations. Carnival operates 79 cruise ships with a total capacity of 136,960 passengers in North America, Europe, the

United Kingdom, Germany, Australia, and New Zealand. The company also operates hotels, sightseeing motor coaches and rail cars, and luxury day boats. These activities generated earnings per share of $2.73 for 2006.

The stock price in January of 2007 was $51.95. The previous stock prices and dividends are shown in the following table.

7-16

Chapter 7, Solutions Cornett, Adair, and Nofsinger

Annual Dividend

2000

$0.42

2001

$0.42

2002

$0.42

2003

$0.44

2004

$0.525

2005

$0.80

2006

$1.025

Stock Price in January $40.30 $29.35 $24.96 $22.59 $42.26 $55.44 $50.58

Carnival is a firm in the General Entertainment industry, which is in the Services sector.

The following table shows some key statistics for Carnival, the industry, and the sector.

Key Statistic

P/E ratio

Dividend Yield

Next 5-year Growth

Carnival

30.37

0.50%

15.0%

General

Entertainment

26.20

2.09%

13.28%

Services Sector

25.66

1.33%

13.44%

Use the various valuation models and relative value measures to assess whether Carnival stock is correctly valued. Compute value estimates from multiple models. The appropriate required rate of return is 15 percent.

It will be useful to calculate the stock price for January of 2007 from various methods to compare to the actual value realized at the time, $51.95 per share.

Note that the growth rate is currently the same or higher than the discount rate, so the constant growth rate model cannot be used.

(1) Determine the dividends to year 5 with the same growth rate that the dividends have been growing and then use a terminal P/E ratio of 26 (which is a decline from the current

P/E of 30) to compute the future price. Then find the PV of these cash flows. So first, determine the historical dividend growth rate:

Future value in 6 years

1 .

025

0 .

42

1

g

6 g

16 .

03 %

Now use this 16% growth rate to find the next five dividends:

D1 = $1.025 × (1 + 0.16) = $1.189

D2 = $1.189 × (1 + 0.16) = $1.379

D3 = $1.379 × (1 + 0.16) = $1.600

D4 = $1.600 × (1 + 0.16) = $1.856

D5 = $1.856 × (1 + 0.16) = $2.153

Next, use equation 7-10 to calculate the stock price in year 5:

P

5

E

5

E

5

E

5

E

0

1

g

5

26

$ 2 .

73

( 1 .

16 ) 5

$ 149 .

08

Now find the present value, P

0

, of these cash flows:

7-17

Chapter 7, Solutions Cornett, Adair, and Nofsinger

P

0

D

1

1

i

D

i

2

2

D

3

i

3

D

i

4

4

D

5

P

5

5

1 .

189 / 1 .

15

1 .

379 / 1 .

15 2

1 .

600 / 1 .

15 3

1 .

856 / 1 .

15 4

( 2 .

153

149 .

08 ) / 1 .

15 5

$ 79 .

38

(2) Now, use the variable valuation model, using equation 7-8. Assume that the growth rate for 5 years is 15% and then it scales back to a 13.28%, the General Entertainment industry growth rate, as its constant growth rate:

P

0

P

0

D

0

1 .

025

1

1

1

1 .

025

1

1 i g

1

0 .

15

0 .

15

0 .

15

5

D

0

1

1

1 .

025 g

1

2

1

2

D

0

1

g

1

3

3

1 .

025

1

1

0 .

15

0 .

15

2

2

0 .

15

0 .

15

0 .

15

5

1

0 .

1328

D

0

1

g

1

4

1 .

025

1

1

0 .

15

0 .

15

3

3

0 .

1328

4

4 .

10

68 .

53

$ 72 .

63

D

0

1

g

1

5

1 .

025

1

1

0 .

15

0 .

15

4

4

D

0

1

g

1

1

g

2

i

g

2

i

5

(3) Note that the expected return from equation 7-7 is:

Expected return

i

D

1

P

0

g

0 .

50 %

15 .

0 %

15 .

5 %

This is higher than the proposed discount rate of 15%. This suggests that the stock is undervalued.

Given the results of (1), (2), and (3), and the current stock price of $51.95, Carnival appears undervalued.

7-18