break even slides 2

advertisement

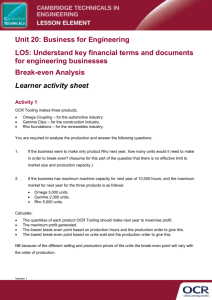

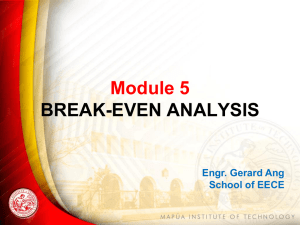

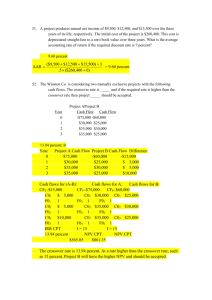

Break Even Lesson 3 Lesson Objectives £ To construct break-even charts ££ To evaluate how changes impact the break-even chart £££ To analyse the strengths and weaknesses of break-even analysis Break-even charts Eat-your-fill restaurant Information needed Eat-yourfill data Weekly fixed costs £2,800 Variable cost per customer £3 Average revenue earned per customer £10 Maximum weekly number 600 of customers- the capacity of the restaurant Construct a break-even chart using the information in the table You will each need a piece of graph paper, a ruler and a pencil You have 5 minutes to complete this … ON YOUR OWN Bill Potter Information needed Forecasts Annual fixed costs £30,000 Variable costs per customer £45 Selling price per pair of shoes £105 Expected maximum sales level 2,000 pairs per year Using the information in the table construct a break-even chart. If you need help, refer to the chart that you constructed last lesson • The break-even chart was included in Bill’s business plan, however the Bank Manager questioned the high selling price. Bill completed some market research and decided that £85 would be more realistic. • He also decided that it would be best to rent a shop in a better location but this would cost an extra £20,000 a year. • Compare the two break-even charts Strengths and weaknesses of break even analysis • Working in a pair, list as many strengths and weaknesses as possible Strengths Weaknesses •Simple concept •Assumes that all output is sold •Good for decision making •Assumes that the business only sells one product •Used when applying for loans •Can be easily changes to deal with ‘what if’ situations •Assumes that everything is consistent •It does not show what will happen, revenue or price may change Complete the activity booklet Complete the following • Research topic: Use the BBC Business website to research a company that is struggling to meet its break-even point. • Hint: Search for the Airbus A380 Plenary • Can you… – Explain what contribution and contribution per unit mean – Explain what ‘breaking-even’ means and define break-even point – Use contribution per unit to calculate the break-even point – Draw a break-even chart and identify its main features – Change any of the key variables- price, variable cost and fixed cost- and re-draw a break-even chart – Use the data to advise decision making – Evaluate the usefulness of break-even analysis