Chapter 7: Banking

advertisement

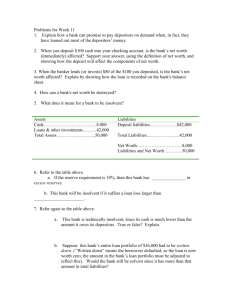

Chapter 7: Banking Personal Financial Management FINANCIAL SERVICES AND INSTITUTIONS CHAPTER 7.1 Beginning of Banking • 1791 • First central bank – 8 branches • Today - 11,000 banks, 2,000 savings and loan associations, and 12,000 credit unions. Types of Financial Services • Savings • Payment Services • Borrowing • Other financial services Savings • Essential for any personal finance plan. • Time Deposit – money that is left in a financial institution for months or years. • Examples: money in any type of savings account and CDs • Selection of savings plan should be based on interest rates, liquidity, safety, and convenience. Payment Services • Checking Account – most commonly used payment service • Demand Deposit – money that you place in a checking account • You can withdraw the money at any time, or on demand. Borrowing • Short-Term • Credit cards, personal cash loan • Long-Term • Mortgage, auto loan Other Financial Services • Insurance protection • Stock – money paid for investment into a business (securities) • Bond – A form of a loan or IOU (securities) • Mutual Funds – pools money from multiple investors to purchase securities Electronic Banking Services • Direct Deposit – automatic deposit of net pay into an employees designated banking account • Automatic Payments – authorization needed, your bank withdrawing money monthly for a payment or bill • ATM – computer terminal that allows for the withdrawal of money, deposits, and transfers Document Detectives • Textbook Page 193 • Answer question #1-6 in your notes Evaluating Financial Services • Balance your short-term needs with your longterm needs • Location and convenience • Fees • Re-evaluate occasionally Types of Financial Institutions • Safety • Deposit Institutions • Non-Depository Institutions Safety • Record, examine history • Federal Deposit Insurance Corporation (FDIC) • Protects deposits in banks • Insures each account in a federally chartered bank up to $100,000 per account Deposit Institutions • Commercial banks – for-profit institution that offers a full range of financial services. • Savings and loan associations – traditionally specialized in savings accounts and mortgage loans but now offers many of the same services as commercial banks. • Mutual savings banks – owned by depositors, specialize in savings accounts and mortgage loans. Lower interest rates on loans and pay a higher rate on savings accounts. • Credit unions – nonprofit, owned by its members and organized for their benefit. Non-Depository Institutions • Life Insurance Companies – provide financial security for dependents. • Investment Companies – combine money with funds from other investors in order to purchase securities, mutual funds. • Finance Companies – Advice, loans for consumers and small businesses, investing Problematic Financial Businesses • Pawnshops • Make loans based on the value of tangible possessions • Interest charged • Check Cashing Outlets • Charge from 1-20% of the face value of a check • Payday Loans • Write a check to get a ‘loan’ • Personal check not cashed for 14 days • Interest charged and rolled over, a continuous cycle • Rent-to-Own Centers • Own an item if consumers complete a certain number of monthly or weekly payments. • Interest charged – end up paying more than the item is valued. Section 1: Assessment • Textbook page 201 • #1-7 • Complete on separate sheet of paper and turn in