1_Money -basic notion

advertisement

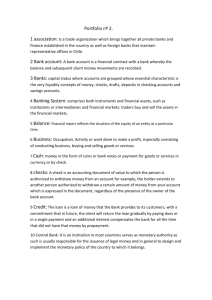

MONEY: BASIC NOTION Samir K Mahajan MONEY: MEANING AND FUNCTIONS • • • • • Money is regarded any object which is generally accepted as: medium of exchange unit of account standard of deferred payment store of value transfer of value. Samir K Mahajan MONEY: MEANING AND FUNCTIONS contd. Primary Functions o As medium of exchange, money is used as a means of payment. As money has ready purchasing power, it facilitates in transacting exchange of goods and services with minimum effort and time. o As unit of account, money is treated as common measure of value. Value of all goods and services in exchange can be expressed in terms of money. Such expression gives rise to price system in which money act as a means of calculating the relative prices of goods and services. Secondary Functions: o As standard of deferred payment, money can be used in the settlement of debt and future payments. Loans are advanced and future contracts are settled in terms of money. o As store of value, money is hold as an asset in liquid (or cash balance) to use anytime in future. This is because money has purchasing power which holds commands over goods and services all time – at present and in future. However use of money as store of value is not without drawbacks. Changes in general price level causes rise and fall in the value of money. When price level rises, value of money falls and vice versa. o As transfer of value, sale and purchase of movable and immovable assets, paper wealth and physical wealth can be made with the help of money. Thus, value available with a person in the form of asset can be transferred from one person to another with the use of money. Samir K Mahajan FORMS OF MONEY IN MODERN TIMES In modern monetary transactions, In modern era, the total stock of money or money supply includes the following: Metallic money or currency coins : Metallic money refers to the coins made out of metal like gold, bronze, silver, copper, nickel. Coins are of two types such as: Standard or Full-bodied Coins and Token coins. o Standard or Full-bodied Coins are those coins whose face value is equal to its intrinsic (metallic) value. o Token coins have intrinsic (metallic) value less than its face value. They generally are of lower denominations are made of cheap metals like nickel and copper. Token coins are used for exchange of small value. Paper money or paper currency : Paper money consists of currency notes issued by the State Treasury or the Central bank of the country. Paper currency have intrinsic (metallic) value less than its face value Credit or bank money: Bank demand deposits withdraw-able by issuing cheque has started functioning as money, and cheque are conventionally accepted as a means of payment by the business community in general. Samir K Mahajan LEGAL TENDER AND CONVENTIONAL MONEY In modern era, currency money and bank money together constitute the total stock of money or money supply. Currency money (both currency coins and currency notes) is legal tender money or fiat money and has general acceptability. Currency coins have limited legal tender whereas currency notes have unlimited legal tender. Credit money or bank demand deposits are conventional money and lacks general acceptability. Samir K Mahajan MONEY AS LIQUID ASSET Further return giving assets such as time deposits with bank, bonds and government securities, treasury bills, common stock and inventories, and real estate do serve as value but they differ in the degree of liquidity. Stocks or Equity share in the stock exchange are store of value because they are marketable but they are not stable in terms of value. Their price stability is less than that of money. Therefore such asset is not as liquid as money. Further, equity share, bonds etc have to be sold in stock market first in order to obtain money which is exchangeable. In the selling process there is not only some delay, but there are chances of loss (as their price is not stable) and it also involves costs such as: broker’s commissions etc. Time or fixed deposits in banks are not readily withdraw-able and convertible to cash. The customer has to serve notice to the banker in advance to encash the deposits. There is thus the presence of time lag in their transferability. If the assets are held in terms of real goods, there is storage cost and there is possibility of depreciation. It also involves a high time-element in the selling process. Thus money is readily expendable; while in the case of other assets (financial or real), one has to first exchange a given assets for cash which involves a time-lag, cost and even capital uncertainty. Samir K Mahajan MONEY AND NEAR MONEY Modern economists draw a distinction between money and near money. Money/pure money include currencies (coins and notes) and demand deposits withdrw-able by cheques. Near-money is income yielding assets which give return in the form of dividend and interests. Holding cash balance /pure money bear opportunity cost in the form of interests or dividends. Holding cash balance or pure money does not yield any income. Near money/ money substitutes are financial assets or paper wealth such as: •Bills of exchange •Promissory notes •Bankers’ acceptance or time draft •Redeemable and marketable government securities •Gilt-edged securities •Cash surrender and value of life insurance policies •Traveler’s cheque •Share of joint stock companies •Negotiable credit instruments •Bond , debentures and certificates •Fixed deposits •Mutual funds Samir K Mahajan CLASSIFICATION OF MONEY BY RESERVE BANK OF INDIA M1 ( Narrow Money/High Powered Money) = Currency ( coins and notes) with public + Demand deposits (Current Deposits and Demand Liabilities Portion of Savings Deposits ) with the Banking system + Other deposits with RBI M2 = M1 + Time Liabilities Portion of Savings Deposits with the Banking System + Certificate of Deposit (CDs) issued by Banks + Term Deposits of residents with a contractual maturity of up to and including one year with the Banking System (excluding CDs) M3 (Broad Money)= M2 + Term Deposits of residents with a contractual maturity of over one year with the Banking System + Call/Term borrowings from 'Non-depository Financial Corporations by the Banking System M4 = M3 + All deposits with post office savings banks (abolished) Samir K Mahajan CLASSIFICATION OF MONEY BY RESERVE BANK OF INDIA M1 ( Narrow Money/High Powered Money) = Currency ( coins and notes) with public + Demand deposits with the Banking system + Other deposits with RBI = coins and notes with public +Current Deposits and Demand Liabilities Portion of Savings Deposits deposits with RBI + Other M2 = M1 + Time Liabilities Portion of Savings Deposits with the Banking System + Certificate of Deposit (CDs) issued by Banks + Term Deposits of residents with a contractual maturity of up to and including one year with the Banking System (excluding CDs) =coins and notes with public + Current Deposits and Demand Liabilities Portion + Other deposits with RBI + Time Liabilities Portion of Savings Deposits + Certificate of Deposit (CDs) issued by Banks + Term Deposits of residents with a contractual maturity of up to and including one year with the Banking System (excluding CDs) =Currency ( coins and notes) with public + Savings Deposits + Other deposits with RBI + Certificate of Deposit (CDs) issued by Banks + Term Deposits of residents with a contractual maturity of up to and including one year with the Banking System (excluding CDs) M3 (Broad Money)= M2 + Term Deposits of residents with a contractual maturity of over one year with the Banking System + Call/Term borrowings from 'Non-depository Financial Corporations by the Banking System M4 = M3 + All deposits with post office savings banks (abolished) Samir K Mahajan CLASSIFICATION OF MONEY BY RESERVE BANK OF INDIA M1 ( Narrow Money/High Powered Money) = Currency ( coins and notes) with public + Demand deposits (Current Deposits and Demand Liabilities Portion of Savings Deposits ) with the Banking system + Other deposits with RBI M2 = M1 + Time Liabilities Portion of Savings Deposits with the Banking System + Certificate of Deposit (CDs) issued by Banks + Term Deposits of residents with a contractual maturity of up to and including one year with the Banking System (excluding CDs) M3 (Broad Money)= M2 + Term Deposits of residents with a contractual maturity of over one year with the Banking System + Call/Term borrowings from 'Non-depository Financial Corporations by the Banking System M4 = M3 + All deposits with post office savings banks (abolished) Samir K Mahajan