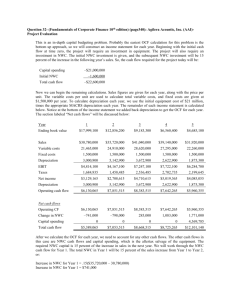

Chapter 7: Making capital investment decisions

advertisement

Chapter 6: Making capital investment decisions Corporate Finance Ross, Westerfield, and Jaffe Outline 1. Relevant/incremental cash flows 2. An example 3. The equivalent annual cost method TVM We need to evaluate a new project using the TVM technique. That is, we should discount future expected cash flows (specifically, FCFs) back to present time and compare PV to initial costs: whether NPV > 0? Discount cash flows, not earnings. Relevant cash flows But before we do this, a few notions about cash flows need to be addressed. The cash flows in the capital-budgeting time line need to be relevant cash flows; that is they need to be incremental in nature. Incremental cash flows: those cash flows that will only occur if the project is accepted. Ask the right question You should always ask yourself “Will this cash flow occur ONLY if we accept the project?” – – If the answer is “yes”, it should be included in the analysis because it is incremental. If the answer is “no”, it should not be included in the analysis because it will occur anyway. Sunk costs A sunk cost is a cost that has already occurred regardless of whether the project is accepted. Example: consulting fee for evaluating a project. Sunk costs should not be taken into consideration when evaluating a project. Opportunity costs Opportunity costs (OCs) are the costs of giving up the second best use of resources. Example: a vacant land. Opportunity costs should be taken into consideration when evaluating the project. Side effects Accepting a new project may have side effects. Erosion occurs when a new project reduces the sales and cash flows of existing projects. Synergy occurs when a new project increases the sales and cash flows of existing projects. Cash flows due to erosion and synergy are incremental cash flows. An example, I Baldwin Company is considering an investment project: producing colored bowling balls. The estimated life of the project: 5 years. The cost of test marketing: $250,000. Would be produced in a vacant building owned by the firm; the property can be sold for $150,000 after taxes. The cost of a new machine: $100,000. The estimated market value of the machine at the end of 5 years: $30,000. An example, II Production by year for the 5-year life: 5,000 units, 8,000 units, 12,000 units, 10,000 units, and 6,000 units. The price of bowling balls in the first year: $20. The price of bowling balls will increase at 2% per year. No debt financing; no interest expenses. An example, III First-year production costs: $10 per unit. Production costs will increase at 10% per year. Incremental/marginal corporate tax rate: 34%. An initial investment (at year 0) in net working capital: $10,000. NWC at the end of each year will be equal to 10% of sales for that year. NWC at the end of the project is zero. An example, IV Year 1 2 3 4 5 Units Price/unit Revenue Cost/unit Cost 5000 20 100000 10 50000 8000 20.4 163200 11 88000 12000 20.808 249696 12.1 145200 10000 21.22416 212241.6 13.31 133100 6000 21.648643 129891.9 14.641 87846 Depreciation Depreciation for tax purpose in the U.S. is based on the Modified Accelerated Cost Recovery System (MACRS). See Table 6.3 (p. 176) for IRS depreciation schedule. For a 5-year depreciation, the depreciation schedule is: 20% (year 1), 32% (year 2), 19.2% (year 3), 11.5% (year 4), 11.5% (year 5), and 5.8% (year 6). An example, V Year 1 Sales 100000 Costs 50000 Dep. 20000 Income before tax 30000 Tax 10200 Net Income 19800 OCF 39800 NWC 10000 Year 2 Year 3 Year 4 Year 5 163200 249696 212241.6 129891.9 88000 145200 133100 87846 32000 19200 11500 11500 43200 85296 67641.6 30545.86 14688 29001 22998.14 10385.59 28512 56295 44643.46 20160.27 60512 75495 56143.46 31660.27 16320 24970 21224.16 After-tax salvage cash flow OCF = sales – costs – taxes. The estimated salvage market value of the machine is 30% of $100,000; that is, $30,000. The machine will have been depreciated to 5.8% of $100,000 at that time; that is, $5,800. The taxable amount is $24,200 ($30,000 - $5,800). The after-tax salvage cash flow is: $30,000 – (34% × $24,200) = $21,772. An example, VI Year 0 OCF Capital OC NWC ΔNWC Salvage Total CF IRR Year 1 Year 2 Year 3 Year 4 Year 5 39800 60512 75495 56143 31660 -100000 -150000 150000 10000 10000 16320 24970 21224 -10000 0 -6320 -8650 3745 21224 21772 -260000 39800 54192 66846 59889 224656 16% Decision If the nominal discount rate (cost of equity) is less than 16%, we accept the project. In other words, if the discount rate is higher than 16%, we have a negative NPV. NPV The firm uses no debt. Thus the appropriate discount rate is the cost of equity. Suppose that cost of equity is 15%. NPV = 5473.43 (> 0). An example, VII Year 0 OCF Capital OC NWC ΔNWC Salvage Total CF Re NPV Year 1 Year 2 Year 3 Year 4 Year 5 39800 60512 75495 56143 31660.3 -100000 -150000 150000 10000 10000 16320 24970 21224 -10000 0 -6320 -8650 3745 21224.2 21772 -260000 39800 54192 66846 59889 224656 15% 5473.43 Alternative definitions of OCF In our previous calculation, we used the topdown approach to compute OCF ( = sales – costs – taxes). Another 2 alternative methods: the bottom-up method, and the tax shield method. See pp. 186-189. The equivalent annual cost method This method is useful (1) when one tries to choose between 2 machines of unequal lives, or (2) whether one should replace an existing machine with a new one. Whereas a general capital budgeting problem is often computed in nominal terms, the equivalent annual cost (EAC) method works best in real terms. Nominal vs. real Time 0 1 2 Nominal CF -1000 600 650 Expected Inflation 5% Real CF -1000 571.43 589.57 2 machines with unequal lives Revenues per year are the same, regardless of machine. The nominal discount rate (NR) is 13.3%. The expected inflation rate (E(I)) is 3%. The real discount rate (RR) is 10%. (1 + NR) = (1 + RR) × (1 + E(I)) (1 + 13.3%) = (1 + 10%) × (1 + 3%). Real cost outflows w/ real discount rate Time 0 Time 1 Time 2 Time 3 Time 4 Machine A 500 120 120 120 Machine B 600 100 100 100 100 Discount 10% PV_A 798.42 PV_B 916.99 Equivalent annual cost One needs to use real (nominal) discount rate to discount real (nominal) cash flows. For A, the EAC is $321.05. 798.42 PV; 3 N; 10 I/Y; CPT PMT. For B, the EAC is $289.28. 916.99 PV; 4 N; 10 I/Y; CPT PMT. B has a lower equivalent annual cost. We should choose B. End-of-chapter Concept questions: 1-12. Questions and problems: 1-20.