real options in investments

advertisement

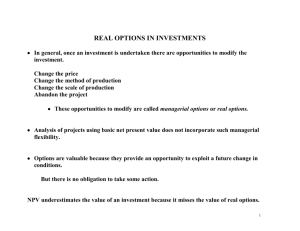

REAL OPTIONS IN INVESTMENTS In general, once an investment is undertaken there are opportunities to modify the investment. Change the price Change the method of production Change the scale of production Abandon the project These opportunities to modify are called managerial options or real options. Analysis of projects using basic net present value does not incorporate such managerial flexibility. Options are valuable because they provide an opportunity to exploit a future change in conditions. But there is no obligation to take some action. 1 NPV underestimates the value of an investment because it misses the value of real options. These include the opportunities to modify an investment and the option to wait before investing. Expanded NPV = Static NPV + Value of managerial flexibility Types of real options: 1. Investment timing options – delay the decision until later, when more information is available. 2. Growth options – allow a company to increase its capacity if market conditions are better than expected. 3. Abandonment options – allow a company to abandon a project if market conditions deteriorate and cause lower than expected cash flows. 4. Flexibility options – permit a firm to alter operations depending on how conditions change during the life of the project. 2 POSSIBLE APPROACHES TO DEAL WITH REAL OPTIONS 1. Use discounted cash flow (DCF) valuation and ignore any real options by assuming their values are zero. 2. Use decision tree analysis. 3. Use a standard model for a financial option. Five basic variables affect the value of real options when using financial option models: 1. The value of the underlying risky asset – a project, investment, or acquisition 2. The strike price – the amount of money invested to exercise the option if you are “buying” the asset (with a call option), or the amount of money received if you are “selling” it (with a put option) 3. The time to expiration of the option 4. The standard deviation of the value of the underlying risky asset 5. The risk-free rate of interest over the life of the option 3 AN EXAMPLE OF THE OPTION TO ABANDON A PROJECT Ignoring flexibility Investment amount is $550. Required rate of return is 20%. There is a 50% chance that cash flow will be $150 per year thereafter and 50% chance that cash flow will be $50 thereafter. Thus, your expected cash flows are the average: $100 per year into perpetuity. NPV = -$550 + $100 = -$50. .20 Incorporating flexibility using decision trees In one year we will know more about market demand. The project or assets can be sold in one year for $400. That is, we have the option to abandon the investment. 4 DECISION TREE FOR THE PROJECT $150 $150 (High demand) T=2 T=3 $50 $50 (P = .50) $150 -$550 T=0 $50 T=1 (At time 1 there is an option to sell assets for $400) (P = .50) (Low demand) T=2 T=3 5 ESTIMATING THE VALUE OF FLEXIBILITY TO ABANDON A PROJECT Contingency planning: Low cash flow outcome leads us to sell the assets in one year for $400. PV of cash flow = 50 $250 < Abandonment value ($400) .20 High cash flow outcome leads us to continue the project. PV of cash flow = 150 $750 > Abandonment value ($400) .20 In one year the going-forward value of the project is either $400 or $750, or an expected value of $575. 6 We will also receive a cash flow of either $150 or $50 in one year. So the total value of the project is either $900 or $450, which gives us an expected value of (0.5)($900) + (0.5)($450) = $675 one year from today. Expanded NPV = Static NPV + Value of managerial flexibility, so Expanded NPV = $550 $675 $12.50 1.20 Value of managerial flexibility = Expanded NPV - Static NPV Value of Flexibility = $12.50 - (-$50) = $62.50 7 INVESTMENT TIMING Investment timing is like a call option on a stock. It gives you the right to delay investment to see if market conditions are favorable. Cash flows may all be discounted at the same rate. However, there is no possibility of losing money if you delay an investment since the low-demand cash flows are eliminated. To account for this, the initial investment is typically discounted at a lower rate (e.g., the risk-free rate). Using financial options models (i.e., Black-Scholes): The value of the underlying risky asset (S) is the present value of the future cash flows of the investment. The exercise price (X) is the initial investment. The time to expiration (t) is the length of time you can delay the investment. The risk-free rate (r) is typically the Treasury bill rate. The standard deviation (σ) is the riskiness of the project's return. 8