Dissatisfactions with normative accounting

advertisement

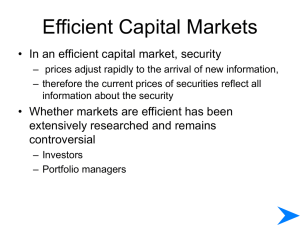

Prepared by Arabella Volkov University of Southern Queensland References •Text – Chapter 9 Positive theory and capital market research Learning Objectives At the conclusion of this lecture, you should have an appreciation of: • the philosophy of positive accounting theory • the strengths of positive accounting over normative accounting • the scope of positive accounting theory Learning Objectives At the conclusion of this lecture, you should have an appreciation of: • capital market research and the efficient market hypothesis • the influence of accounting information on investor behaviour and share prices • trading strategies and mechanistic behavioural effects Philosophy of positive accounting theory • seeks to explain observed accounting phenomena • economic focus • more scientific in methodology • Assumptions about the behaviour of individuals • underlies most empirical studies in economics Strengths of positive theory over normative theory Dissatisfactions with normative accounting: – Prescriptions not based upon identified, empirical observations or methods – Theories are not falsifiable – Does not explain and predict accounting practice – Do not assess existing accounting practices Scope of positive accounting theory Two stages of development: 1. Capital market research – – – – Did not explain accounting practice Connection EMH Market model 2. Explaining and predicting accounting practice Capital Markets Research & the Efficient Markets Hypothesis • Two types of capital markets research: – Impact of the release of accounting information on share returns – The effects of changes in accounting policy on share prices • Most research in these areas relies upon the efficient markets hypothesis (EMH) Capital Markets Research & the Efficient Markets Hypothesis Efficient market: one ‘in which prices ‘fully’ reflect available information’ 3 Forms of Information Efficiency: 1. Weak form (past price information) 2. Semi-strong form (publicly available information) 3. Strong form (all information – public and private) Capital Markets Research & the Efficient Markets Hypothesis • Capital markets research in accounting assumes semi-strong form efficiency • Financial statements and other disclosures form part of the information set that is publicly available Capital Markets Research & the Efficient Markets Hypothesis Sufficient conditions of an efficient market (Fama): • There are no transaction costs in trading securities • All information is available cost-free to all market participants • All agree on the implications of current information for the current price and distributions of future prices of each security Capital Markets Research & the Efficient Markets Hypothesis Market efficiency does not assume: • Other forms of efficiency recognised in economics • Every investor has knowledge of all information • All financial information is correctly presented or interpreted by individual investors • Managers make the best decisions • Investors can predict the future precisely Capital Markets Research & the Efficient Markets Hypothesis CMR: • Empirical research • Tests hypotheses about capital market behaviour Market Model: • Derives from CAPM • Used to estimate abnormal returns on shares when profits announced Capital Markets Research & the Efficient Markets Hypothesis Capital Markets Research & the Efficient Markets Hypothesis Figure 9.1: Sample market model for i = BHP and t = quarter ending June 2001 Impact of Accounting Profits Announcements on Share Prices Ball & Brown (1968): • Seminal work in positive accounting and finance literature • Tested the usefulness of historical cost profit figure to investment decisions • If historical cost profit figure is useful share price will react (EMH) Impact of Accounting Profits Announcements on Share Prices Impact of Accounting Profits Announcements on Share Prices Ball & Brown (1968) Results: • Most of the information contained in the earnings announcement (85-90%) was anticipated by investors • Evidence of Information content at time of (historical cost) earnings announcement Impact of Accounting Profits Announcements on Share Prices • Magnitude • Information asymmetry and firm size • Microstructure extensions to firm size • Magnitude of profit releases of other firms • Volatility Association Studies & Earnings Response Coefficients Association studies • impact of accounting measures on share prices over a longer event window • Earnings response coefficient (ERC) is a subset of this literature ERC: • Ordinary least-squares regression • Dependant variable: returns • Independent variable: profit • R2 (goodness of fit) and slope (sensitivity of returns to profit) used to assess informativeness of profits Association Studies & Earnings Response Coefficients Factors which can affect the ERC: • Risk and uncertainty • Audit quality • Firm size • Industry • Interest rates • Financial leverage • Firm growth • Permanent and temporary profits Association Studies & Earnings Response Coefficients Determinants of firm value: • Industry • Interest rates • Financial leverage • Audit quality • Firm size • Firm growth Association Studies & Profit Response Coefficients Determinants of firm value (cont’d): • Magnitude of profit releases of other firms • Volatility • Permanent and temporary earnings • Omitted variables • Changes versus levels in earnings • Profit components • Cash flows Methodological issues • Ball and Brown’s original paper – Positive theory of accounting • Williams and Findlay – Argue the results of the research are supportive of EMH • Watts and Zimmerman – No attempt to differentiate EMH Trading Strategies • Post-announcement drift • Winner/loser effect – Long-term association anomaly • Past winners tend to be future losers and vice versa • Debondt and Thaler – Long-term return reversals to investor overconfidence and – Biased self-attribution Mechanistic or behavioural effect • Cosmetic accounting – Leftwich • Two hypotheses – Market reacted mechanistically to changes in accounting numbers, regardless whether they were cosmetic or whether they had cash flow implications – Market ignored accounting changes which had no cash flow consequences Mechanistic or behavioural effect Manipulating accounting numbers: Mechanistic or behavioural effect Detecting the quality and probability of accounting management: Summary • Philosophical objective of positive accounting theory is to explain and predict current accounting practice • Positive theory developed in two stages – Capital market research – Contracting theory Key terms and concepts • • • • • • • Positive accounting theory EMH CAPM CAR Information asymmetry Market efficiency Impact of behaviour Where to get more information • • • • Other courses List books Articles Electronic sources