Accounting Standards and Standard Setting Organisations

advertisement

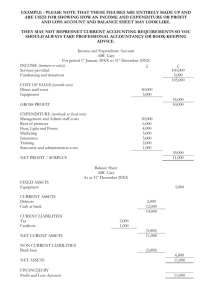

6201 – Financial Accounting Borrowing Costs Example PART A On 1 April 2011 ABC Ltd commenced the construction of factory premises for their manufacturing operation. The factory was completed and ready for occupation on 30 September 2012. Payments for materials and services relating to the construction activity were made as follows: 2 April 2011 30 June 2011 31 December 2011 31 May 2012 31 July 2012 31 August 2012 $ 340,000 200,000 570,000 450,000 234,000 86,400 1,880,400 On 1 April 2011, ABC Ltd negotiated a loan for $1,600,000 for the duration of the construction period. Interest at 12 percent per annum was payable on this loan. ABC Limited has a financial year end of 31 March. Required: (a) Calculate the interest to be capitalised for the year ending 31 March 2012, assuming that the loan negotiated on 1 April 2011 was specifically for the construction activity. (b) Prepare the journal entry at 31 March 2012 to record those costs of the building that should be capitalised. (c) Calculate the interest to be capitalised for the year ended 31 March 2013. (d) Determine the total costs of the building premises at the end of construction. PART B Using the information from Part A, assume that instead of borrowing funds for the construction activity ABC Ltd had a $4,000,000 9 percent and $2,800,000 13 percent long-term loan outstanding during the entire construction period. Required: Calculate the amount of interest that would be capitalised for the year ended 31 March 2012. 6201 – Financial Accounting SOLUTION (a) First calculate the weighted-average expenditure to be used to determine interest capitalisation: 2 April 2011 30 June 2011 31 December 2011 Accumulated expenditure $ 340,000 x 12/12 200,000 x 9/12 570,000 x 3/12 1,110,000 Weightedaverage expenditure $ 340,000 150,000 142,500 632,500 As the loan was negotiated specifically for the construction of the manufacturing operation the interest to be capitalised is calculated as: $632,500 x 12% = $75,900 (Note that this doesn’t affect the interest of $192,000 paid on the 12% $1.6m loan. It simply means that $75,900 of this amount is capitalised and the balance of $116,100 expensed.) (b) Journal entry J1.1 DR CR (c) Calculate weighted average expenditure for 31 March 2013: Manufacturing building 1,185,900 Cash 1,185,900 Capitalising construction costs of $1,110,000 and interest of $75,900 1 April 2012 31 May 2012 31 July 2012 31 August 2012 Accumulated expenditure $ *1,185,900 450,000 234,000 86,400 1,956,300 x x x x 6/6 4/6 2/6 1/6 Weightedaverage expenditure $ 1,185,900 300,000 78,000 14,400 1,578,300 * Amount of expenditure on project at balance date, meaning that during the current financial year interest must be capitalised on this amount from 1 April 2012 to the end of the construction period. 6201 – Financial Accounting The interest to be capitalised for the year ended 31 March 2013 amounted to: $1,578,300 x 12% x 6/12 = $94,698 Journal entry J2.1 DR CR Manufacturing building 865,098 Cash 865,098 Capitalising construction costs of $770,400 and interest of $94,698 (d) Up to 31 March 2012, $1,185,900 is capitalised, with a further $865,098 for the final six months, so overall the total cost of the building is $2,050,998. PART B As the funds were not borrowed to finance the construction activity, the average interest rate on all debt must be calculated as follows: Loan ($) 4,000,000 2,800,000 Interest rate (%) 9 13 Interest ($) 360,000 364,000 724,000 The weighted average of interest to total debt is 10.6 percent ($724,000 $6,800,000). The determinations will be the same as in Part A, but using the weighted average interest rate. So the interest capitalised for the first year (ended 31 March 2012) is: $632,500 x 10.6% = $67,045