Third Quarter 2014 Market Commentary

Doug Ramsey, CFA, CMT

Chief Investment Officer

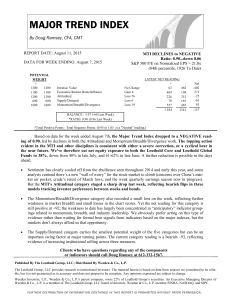

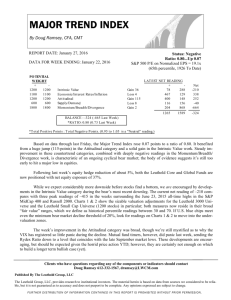

After a prolonged period in which our asset allocation disciplines kept us heavily exposed

to the stock market, it’s time to play defense. The Major Trend Index (MTI), a composite of more

than one hundred market indicators and sub-models, dropped into its Neutral zone in early August, and two months later followed up with its first Negative reading in three years. We responded

to these changes with several adjustments to our tactical funds’ exposures which ultimately drove

net equity positions down to 40%, currently, a reduction from a fairly aggressive 65% in early July.

We would not be surprised to see a peak-to-trough correction in global stocks of 12-15%,

with considerably larger losses in Small Caps and Emerging Market equities. However, the duration or extent of a market correction (or a rebound, for that matter) can never be known in advance, and there’s certainly the chance that any decline will fall short of our expectation. In that

event, the self-correcting elements of the MTI should respond quickly enough in directing us to

rebuild equity exposure.

Why did the MTI fall into Negative territory? First, we’ve commented on the elevated valuations of U.S. equities (and Small Caps in particular) repeatedly the past 18 months. The dilemma

with valuation tools is that they are very effective over long-term horizons of five to ten years, but

of limited (or no) use in the short-term. That is to say, an overvaluation condition can move from

mild to moderate and, sometimes, to an extreme as long as cyclical market conditions remain hospitable.

Second, investor sentiment had been fairly restrained throughout most of the bull market,

but the big gains of 2013 seemed to finally drive away the last of any lingering memories from the

2008 debacle. In fact, in March, our proprietary composite reading of investor sentiment shot up

to the most optimistic reading in its 36-year history, sending a strong negative signal from a contrarian point of view.

Still, the combination of elevated stock market valuations (especially in the U.S.) and inflated investor expectations can persist for extended periods… the market advance throughout

the Technology mania provides the most memorable historical example. However, inflated sentiment and valuation readings generally don’t become dangerous until stock market “liquidity” (or

Federal Reserve policy accommodation) begins to contract. We believe the succession of Fed “tapers” in the monthly level of Quantitative Easing (QE) throughout 2014 has finally triggered such

a liquidity contraction. In other words, this unusual form of Fed “tightening” has been underway

for several months—even though the Fed isn’t expected to increase its benchmark Federal Funds

Rate above the zero level until mid-2015 at the earliest.

(Continued)

Leuthold Weeden

1

Capital Management

Third Quarter 2014 Market Commentary

(continued)

A mere ten months ago, the Fed was making monthly purchases of Treasury bonds and mortgage securities for its own account that totaled one-half of one percent of Gross Domestic Product. By

the end of October, that stimulus will end. Thus, the overall level of policy accommodation remains

high, with the Fed sitting on a bloated $4 trillion balance sheet. But the stock market is extremely sensitive to the rate of change in policy, and the rate of change has stalled. This policy change has clearly

been felt by three market groups that are particularly responsive to changes in Fed policy: Small Caps,

Emerging Markets, and stocks in the Consumer Discretionary sector are all underperforming the

broader benchmarks YTD.

The extreme underperformance of Small and Mid Cap stocks in the third quarter proved a

challenge for most active equity portfolios—including our domestic and global industry strategies

which both surrendered the YTD outperformance they had built up during the first and second quarters. On the positive side, stock selection within quantitatively favored industries has remained very

strong.

Over the past several years, weak stock market action has tended to go hand in hand with a

strong bond market. Eventually, this pattern will break… but it has held firm in the past few months,

with yields on the 30-year U.S. Treasury bond briefly dropping below 3.0%. We see little in long-term

valuation appeal for bonds, but they’ve played a valuable tactical role in our portfolios this year. We

continue to increase credit quality across our fixed income holdings, and maintain average portfolio

duration of about 5 years.

If you have any questions, please do not hesitate to contact us. We appreciate your support.

Sincerely,

Doug Ramsey, CFA, CMT

Chief Investment Officer

Leuthold Weeden

2

Capital Management

Other Market Notes

"Averages" Conceal Plight Of The Average Stock

September’s small S&P 500 loss of less than 2% disguised a significant breakdown in the

“average stock” and, we suspect, the typical actively managed portfolio (including ours). We, along

with most active managers, tend to be chronically under-exposed to the Mega Cap stocks that have

propped up the DJIA and S&P 500.

If the September 18th high in the

Chart 1

S&P 500 turns out to be a significant, intermediate-term (or longer-term) stock

market top, it will be an unusual case

because of the lack of forewarning from

internal stock market action. The “granddaddy of all technical indicators,” the

NYSE Daily (All Issues) Advance/Decline

Line typically tops out in advance, with a

lead time of 2-6 months. In September,

this indicator made a new cycle high only

a few days prior to the S&P 500's September 18th high. Furthermore, other

traditionally leading groups such as transportation, banks, and brokerage stocks,

also made highs simultaneously with the

Chart 2

mid-September highs in the S&P 500 and

Chart 2

DJIA.

Our main worry has not been the

Large Caps, however. It has been the

weakness of Mid and Small Cap stocks

(Chart 1). It is not unprecedented, however, for a bull market to persist for an

extended time in the face of Small Cap

underperformance (this occurred in the

1995-1999 period).

In addition to the weakness of Mid

and Small Caps, Chart 2 shows significant

underperformance of Equal-Weighted

measures in relation to Cap-Weighted

ones, all across the market capitalization

spectrum. This is a big reason why the

benchmark indexes have become so difficult for managers to beat.

Leuthold Weeden

3

Capital Management

Other Market Notes

Cycles: Bearish Window Closing, Another Opening...

The mid-year months of a mid-term election year are historically the weakest for the stock market from

a calendar perspective. This year, however, Large Caps have mostly bucked that pattern. The S&P 500 remains

up 4.3% since April 30th (through October 6th), compared with an average annualized return of just +1.1%

in the May-October period of mid-term election years (Chart 1). The good news is that this “cycle overlap”

(mid-year seasonality combined with the presidential election cycle) turns maximum bullish on November 1st.

Small Caps have historically proven more sensitive than Large Caps to various cyclical phenomena

(including calendar anomalies), and their performance in 2014 has been no exception. From a fundamental point of view, we think Small Caps’ YTD underperformance reflects an overdue decline in their relative

P/E premiums. But, admittedly we had been warning of Small Cap P/E compression for some time, and are

intrigued that it commenced only upon the arrival of an exceptionally bearish window of the four-year cycle

“calendar.”

As shown in Chart 2, since 1926 Small Caps have generated an average annualized total return loss of

more than 10% during the mid-year months of a mid-term year. Incredible... and impossible to explain from

a fundamental perspective.

Remember, this cycle combination swings from maximum bearish to maximum bullish at the end of

October. During the combined cycles' six month window beginning with mid-term elections, Small Caps have

generated an astounding annualized total return gain of almost 35% (Chart 2). Once again, this strong performance has no possible fundamental rationale (other than the cynical view that the party in presidential power

has begun to juice the economy, and markets, for re-election purposes).

Chart 2

Chart 1

33 S. 6th Street, Suite 4600

Minneapolis MN 55402

612.332.9141

info@LWCM.com

www.LWCM.com

Disclaimer: The views expressed are those of Doug Ramsey and The Leuthold Group, and are subject to change at any time based on market and other conditions. References to specific securities and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. DOFU: 10.24.14

Leuthold Weeden Capital Management is the adviser to Leuthold Funds. Distributor: Rafferty Capital Markets, LLC, Garden City, NY, 11530 Copyright © 2014 by The Leuthold Group. All Rights

Reserved.

Leuthold Weeden

4

Capital Management