Long-Term

advertisement

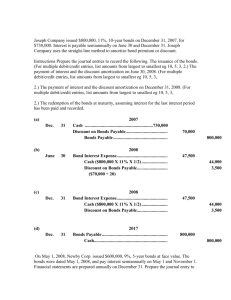

BUS210 Accounting for Financing Decisions: Long-Term Liabilities Liabilities • Current or Short-term Liabilities • Long-term Debt (borrowed funds) • Lease Liabilities • Deferred Taxes • Contingencies and Commitments Accounting for liabilities is a subject that can be very technical. There is a tendency for some institutions to create exotic instruments for marketing of funds in recent years. Despite this, there are some basic principles that govern the accounting for liabilities…. Basis for Valuing Liabilities • Because money has time value, the amount of money needed today to pay a future debt is less than the future obligation. • Historically, the best basis for valuing a liability was its economic present value (the present value of the future cash flows, i.e., the amount of money that would have to be set aside today to accumulate to the future cash flows required to pay the interest and the principal of the debt). • Most current liabilities are reported on the BS at their face (or nominal value)—the amount that will be paid. • Most Long-term liabilities are reported on the BS at their present value (the time-discounted value of the future cash flows). Basic Definitions and Different Contractual Forms Some contracts, called interest-bearing obligations, require periodic (annual or semiannual) cash payments (called interest) that are determined as a percentage of the face, principal, or maturity value, which must be paid at the end of the contract period. Non-interest-bearing obligations, on the other hand, require no periodic payments, but only a single cash payment at the end of the contract period. These contractual forms may contain additional terms that specify assets pledged as security or collateral in case the required cash payments are not met (default), as well as additional provisions (restrictive covenants). Short-term Liabilities • Report at Face value: Accounts payable, Accrued expenses, Unearned revenue, Taxes payable, Warranties payable • Non-interest bearing ST Notes Payable generally are reported at maturity value less any unamortized interest discount. i.e., BS shows either: Note payable $950 or Note payable $1,000 less Unamortized discount $50. • Interest-bearing ST Notes Payable generally are reported at the maturity (face) value plus any accrued interest. i.e., Note Payable $1,000 and Interest payable $50 on BS. • Short-term debt which company has no intentions of liquidating, but plans to continually refinance, should be classified as long-term. Also, the current portion (the amount that will be paid within one year) of any longterm debt should be classified on the BS as a current liability. Long-term Debts • Since interest accounts for the difference between the amount received and the amount paid back, the interest rate is the basis for computing interest. • On all long-term debt contracts there are two interest rates: The stated rate and the effective rate, they may not be the same… • The stated rate is the interest rate on interest-bearing debt that is used to calculate the amount of cash interest payments that will be made to the lender. • The effective rate is the compounded interest rate that mathematically accounts for the total difference between the amount borrowed and the amount repaid. Bond Terminology Key Questions: -Present Value? Issue value or Proceeds -Future Value? Maturity value or Face value -n= number of periods? -r=effective or market interest rate? -Bond or Note stated rate or face rate? -Single payment or Ordinary annuity (multiple payments)? -Interest bearing or Noninterest bearing? What is the interest payment? How often? Draw a Timeline and fill in: -Issue date -When pay interest and amortize discount or premium -Maturity date BE11-2 Bond Terms In October 1997 HP issued zero-coupon bonds with a face of 1.8 billion, due in 2017, for proceeds of $968 million. a. What is the life of these bonds? b. What is the stated rate on these bonds? c. Estimate the effective interest rate of these bonds. (hint: $PV/$FV = approximate Table value) d. How many bonds did HP issue? e. What entry did HP make when the bonds were issued? E11-8 Present Value of a Non-interest-bearing Note Purchased a building 1.1.2015 in exchange for a 3 year non-interest-bearing note with a face of $693,000. Building appraisal is $550,125. a. What amount should this building be capitalized? E11-8 Present Value of a Non-interest-bearing Note Purchased a building 1.1.2015 in exchange for a 3 year non-interestbearing note with a face of $693,000. Building appraisal is $550,125. b. Compute the present value of the note’s future cash flows, using the following discount rates: 1. 6 percent 2. 8 percent 3. 10 percent c. What is the effective rate of this note? d. Explain how one could more quickly compute the effective interest rate on the note. E11-5 Discounted Non-interest-bearing Notes Purchase equipment with a FMV of $11,348 in exchange for a 5 year non-interest-bearing note with a face of $20,000. a. Compute the effective interest rate on the note payable. b. Prepare entry to record the purchase. E11-5 Discounted Non-interest-bearing Notes Purchase equipment with a FMV of $11,348 in exchange for a 5 year non-interest-bearing note with a face of $20,000. c. How much interest expense should be recognized in the first year? d. What is the BS value of the note at the end of the first year? e. Will the interest expense recognized in the second year be greater, equal, or less than the interest expense recognized in the first year? Why? f. Will the interest expense recognized in the third year be greater, equal, or less than the interest expense recognized in the second year? Why? E11-7 Effective Interest Rate On 1.1.15 a company borrowed $2,413 from the bank. The $2,500 note had a maturity date of 12.31.16 and specified an interest rate of 8 percent. (interest $200) a. Compute the PV of the note at the following discount rates: a. 8% b. 10% c. 12% b. What is the effective rate of the note? c. Determine the effective rate if originally borrowed $2,500. E11-9 Effective Interest Rate What is the effective interest rate on the note payable? 2016 2015 Balance Sheet Note Payable Less: Discount on NP $200,000 $200,000 12,000 14,400 16,400 16,200 Income Statement Interest Expense Prepare the journal entry to record 2016 interest expense. E11-4 Non-interest-bearing Note Payable Proceeds Compute the proceeds from the following notes payable. Interest payments are made annually. PV Principal PV Interest Payments = Proceeds Stated Rate Effective Rate Face Value Life 0% 8% $1,000 4 years 0% 6% $5,000 6 years Recap: Non-Interest Bearing Notes and Bonds >Issue date >Amortize discount >Maturity date Accounting for Non-Interest Bearing Notes Payable Recap Sample Non-interest bearing Long-term Notes Payable • Problem 1: On January 2, 2008, Pearson Company purchases a section of land for its new plant site. Pearson issues a 5 year noninterest bearing note, and promises to pay $50,000 at the end of the 5 year period. What is the cash equivalent price of the land, if a 6 percent discount rate is assumed? PV1 = 50,000 x ( 0.74726) = $37,363 [ i=6%, n=5] Journal entry Jan. 2, 2008: Dr. Land Dr. Discount on N/P Cr. Notes Payable 37,363 12,637 50,000 Sample Problem 1 Solution, continued The Effective Interest Method: Interest Expense = Carrying value x Effective interest rate x Time period (CV) (Per year) (Portion of year) Where carrying value = face - discount. For Example 1, CV= 50,000 - 12,637 = 37,363 Interest expense = 37,363 x 6% per year x 1year = $2,242 Sample Problem 1 Solution, continued Journal entry, December 31, 2008: Interest expense Discount on N/P 2,242 2,242 Carrying value on B/S at 12/31/2008: Notes Payable Discount on N/P (Discount = $12,637 - 2,242 = $10,395) $50,000 (10,395) $39,605 Sample Problem 1 Solution, continued Interest expense at Dec. 31, 2009: 39,605 x 6% x 1 = $2,376 Journal entry, December 31, 2009: Interest expense Discount on N/P 2,376 Carrying value on B/S at 12/31/2009: Notes Payable $50,000 Discount on N/P (8,019) 2,376 $41,981 (Discount = 10,395 - 2,376) Carrying value on 12/31/2012 (before retirement)? $50,000 Time Value of Money and Interest bearing LongTerm Liabilities: Notes, Bonds, and Leases • Long-term liabilities are recorded at the present value of the future cash flows. • Two components determine the “time value” of money: – interest (discount) rate – number of periods of discounting • Types of activities that require PV calculations: – notes payable – bonds payable and bond investments – capital leases Interest bearing: Bond Prices E 11-3 Bond Terms The stated and effective interest rates for several notes and bonds follow: Is Note or Bond issued a Par, Premium, or Discount? Bond Stated Interest Rate Effective or Market Interest Rate 1. 10% 10% 2. 7% 8% 3. 9% 8% 4. 11.5% 9% E11-4 Interest-bearing and Non-interest-bearing Note Payable Proceeds Compute the proceeds from the following notes payable. Interest payments are made annually. PV Principal PV Interest Payments = Proceeds Stated Rate Effective Rate Face Value Life 4% 12% $8,000 6 years 8% 8% $3,000 7 years 10% 6% $10,000 10 years Bonds Payable Issued at a Discount • If bonds are issued at a discount, the carrying value will be below face value at the date of issue. • The Discount on B/P account has a normal debit balance and is a contra to B/P (similar to the Discount on N/P). • The Discount account is amortized with a credit. Note that the difference between Cash Paid and Interest Expense is still the amount of amortization. • Interest expense for bonds issued at a discount will be greater than cash paid. • The amortization table will show the bonds amortized up to face value. E11-13 Bonds issued at a Discount Issued 500 five-year bonds on 7.1.15. Interest payments are due semiannually at 1.1 and 7.1 at an interest rate of 6%. The effective rate is 8%. The face value of each bond is $1,000. a. 7.1.15 entry when bonds are issued? b. 12.31.15 entry at yearend? E11-13 Bonds issued at a Discount Issued 500 five-year bonds on 7.1.15. Interest payments are due semiannually at 1.1 and 7.1 at an interest rate of 6%. The effective rate is 8%. The face value of each bond is $1,000. c. 12.31.15 Balance sheet value? d. PV of bonds remaining cash flows as of 12.31.15? Your Turn E11-14 Bonds issued at a Premium Issued 100 ten-year bonds on 7.1.15. Interest payments are due semiannually (1.1 and 7.1) at an annual rate of 8%. The effective rate is 6%. The face of each bond is $1,000. a. 7.1.15 entry to issue bonds? b. 12.31.15 entry? E11-14 Bonds issued at a Premium Issued 100 ten-year bonds on 7.1.15. Interest payments are due semiannually (1.1 and 7.1) at an annual rate of 8%. The effective rate is 6%. The face of each bond is $1,000. c. 12.31.15 balance sheet value? d. PV of remaining cash flows as of 12.31.15? Your Turn E11-11 Bonds Interest payments are made semi-annually on these bonds: Bond Issuance Face Value Stated Interest Rate Effective Interest Rate Life A $110,000 6% 6% 10 years B $400,000 8% 6% 10 years C $600,000 6% 8% 5 years a. Compute the proceeds of each bond. b. c. Will the BS value increase, decrease, or remain constant over life of bond? Will the interest expense increase, decrease, or remain constant over life of bond? E11-11 Bonds Interest payments are made semi-annually on these bonds: Bond Issuance Face Value Stated Interest Rate Effective Interest Rate Life A $110,000 6% 6% 10 years B $400,000 8% 6% 10 years C $600,000 6% 8% 5 years a. Compute the proceeds of each bond. b. c. Will the BS value increase, decrease, or remain constant over life of bond? Will the interest expense increase, decrease, or remain constant over life of bond? E11-11 Bonds Interest payments are made semi-annually on these bonds: Bond Issuance Face Value Stated Interest Rate Effective Interest Rate Life A $110,000 6% 6% 10 years B $400,000 8% 6% 10 years C $600,000 6% 8% 5 years a. Compute the proceeds of each bond. b. c. Will the BS value increase, decrease, or remain constant over life of bond? Will the interest expense increase, decrease, or remain constant over life of bond? Sample Problem 2: Bonds Payable issued at Premium, semiannual interest payments • On July 1, 2007, Mustang Corporation issues $100,000 of its 5-year bonds which have an annual stated rate of 7%, and pay interest semiannually each June 30 and December 31, starting December 31, 2007. The bonds were issued to yield 6% annually. • Calculate the issue price of the bond: (1) What are the cash flows and factors? Face value at maturity = $100,000 Stated Interest = Face value x stated rate x time period 100,000 x 7% x (1/2) = $3,500 Number of periods = n = 5 years x 2 = 10 Discount rate = 6% / 2 = 3% per period Sample Problem 2 - calculations PV of interest annuity: PVOA Table PVOA = 3,500 (8.53020) = $29,856 i = 3%, n = 10 PV of face value: PV1 Table PV = 100,000 (0.74409)=$74,409 i=3%, n=10 Total issue price = $104,265 Issued at a premium of $4,265 because the company was offering an interest rate greater than the market rate, and investors were willing to pay more for the higher interest rate. Sample Problem 2 - Amortization Schedule To recognize interest expense using the effective interest method, an amortization schedule must be constructed. (This expands the text discussion.) To calculate the columns (see next slide): Cash interest paid = Face x Stated Rate x Time = 100,000 x 7% x 1/2 year = $3,500 (this is the same amount every period) Int. Expense = CV x Market Rate x Time at 12/31/07 = 104,265 x 6% x 1/2 year = 3,128 at 6/30/08 = 103,893 x 6% x 1/2 year = 3,117 The difference between cash paid and interest expense is the periodic amortization of premium. Note that the carrying value is amortized down to face value by maturity. Sample Problem 2 - Amortization Schedule Date 7/01/07 12/31/07 6/30/08 12/31/08 6/30/09 12/31/09 6/30/10 12/31/10 6/30/11 12/31/11 6/30/12 Cash Paid 3,500 3,500 3,500 3,500 3,500 3,500 3,500 3,500 3,500 3,500 Interest Expense 3,128 3,117 3,105 3,093 3,081 3,069 3,056 3,042 3,029 3,015 Premium 372 383 395 407 419 431 444 458 471 485 Carrying Value 104,265 103,893 103,510 103,115 102,708 102,289 101,858 101,414 100,956 100,485 100,000 Sample Problem 2 - Journal Entries JE at 7/1/07 to issue the bonds: Cash 104,265 Premium on B/P 4,265 Bonds Payable 100,000 JE at 12/31/07 to pay interest: Interest Expense Premium on B/P Cash 3,128 372 3,500 Note that the numbers for each interest payment come from the lines on the amortization schedule. Sample Bonds Issued at Face Value Sample Bonds Issued at a Discount Sample Bond Amortization Table Recap: Interest Bearing Notes and Bonds >Issue date >Pay interest and amortize discount or premium >Maturity date Investor’s Bond Yield= annual cash received/note price “The yield on a 10 year note, which was hovering at about 2.2% before the release of the non-farm report [on Friday] plummeted to about 2.07% in a matter of minutes. Yields, which move in the opposite direction to prices, continued to move lower, ending the day at 2.056%, compared with 2.173% late Thursday.” Page B2, The Wall Street Journal, 4.7-8.2012 Bond Redemptions When bonds are redeemed at the maturity date, the issuing company simply pays cash to the bondholders in the amount of the face value and removes the bond payable from the balance sheet. To illustrate the redemption of a bond issuance prior to maturity at a loss, assume that bonds with a $100,000 face value and a $5,000 unamortized discount are redeemed for $102,000. The $7,000 loss on redemption would decrease net income P11-10 Callable Bond Redemptions 12.31.14 account balances are: Bond payable $500,000 Premium on bond payable $ 12,600 The bonds have an annual stated rate of 8% and an effective rate of 6%. Interest is paid 6.30 and 12.31. a. Compute the gain or loss if the bonds are called for 104 on 1.1.2015? P11-10 Callable Bond Redemptions 12.31.14 account balances are: Bond payable $500,000 Premium on bond payable $ 12,600 The bonds have an annual stated rate of 8% and an effective rate of 6%. Interest is paid 6.30 and 12.31. b. Compute the gain or loss if the bonds are called for 108 on 1.1.2015? c. Compute the gain or loss if the bonds are called for 110 on 7.1.2015? Bond Conversions The Jolly Corporation has $400,000 of 6 percent bonds outstanding. There is $20,000 of unamortized discount remaining on these bonds after the July 1, 2015, semiannual interest payment. The bonds are convertible at the rate of 20 shares of $5 par value common stock for each $1,000 bond. On July 1, 2015, bondholders presented $300,000 of the bonds for conversion. 1. Is there a gain or loss on conversion, and if so, how much is it? 2. How many shares of common stock are issued in exchange for the bonds? 3. In dollar amounts, how does this transaction affect the total liabilities and the total stockholders' equity of the company? In your answer, show the effects on four accounts. International Perspective • The accounting disclosure requirements in non-U.S. countries and IFRS are not as comprehensive as those in the United States, partially because the information needs of the major capital providers (i.e., banks) are satisfied in a relatively straightforward way—through personal contact and direct visits. • A second way in which the heavy reliance on debt affects nonU.S. accounting systems is that the required disclosures and regulations tend to be designed either to protect the creditor or to help in the assessment of solvency. Economic Consequences of Reporting Long-Term Liabilities • Improved credit ratings can lead to lower borrowing costs • Management has strong incentive to manage the balance sheet by using “off-balance-sheet financing” i.e., operating leases Leases: operating or capital • FASB issued SFAS No. 13, which requires certain leases to be recorded as capital leases. – Capital leases record the leased asset as a capital asset, and reflect the present value of the related payment contract as a liability. • Requirements of SFAS No. 13 - record as capital lease for the lessee if any one of the following is present in the lease: – Title transfers at the end of the lease period, – The lease contains a bargain purchase option, – The lease life is at least 75% of the useful life of the asset, or – The lessee pays for at least 90% of the fair market value of the lease. Capital Lease P11-14 Capital and Operating Leases Company leased equipment on 1.1.14 for an annual lease payment of $30,000. Assume the lease term is 5 years and the life of the equipment is also 5 years. If the lease is treated as a capital lease, the FMV of the equipment is $119,781. The straight line depreciation method is used to depreciate fixed assets. The effective interest rate on the lease is 8%. a. Compute rent expense for 2014-2018 if lease is treated as an operating lease. b. Compute the amounts that would complete the table: Date BS Value Leasehold Obligation Interest Expense Depreciation Expense Total Expense 1.1.2014 12.31.2014 12.31.2015 12.31.2016 12.31.2017 12.31.2018 c. Compare total expense over 5 years for the two methods and comment.