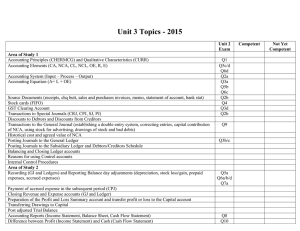

VCE Accounting Unit 3

Chapter 5: Special Journals

Key knowledge

Special Journals vs Double Entry Accounting

State two advantages of Special Journals compare to double entry accounting

(p 82)

1…………………………………………………………………………………………

…………………………………………………………………………………………..

2…………………………………………………………………………………………

………………………………………………………………………………………….

How do we use special journals work for general ledger? (p82)

Role of Special Journal

What is special journal? (p82)

How many types of special journals are often used by small business?

(p82-83)

Special Journal

What does it record?

Type of source documents

Example of Cash Receipts Journal (Figure 5.2, p 84)

Business name: name of special journal + reporting period

Date Details Rec.

Bank Debtors Cost

Sales

no

$

of

sales

Transaction

details

*write

debtors

name if there are

many

Write

Rec.

No. of

cash

GST

Sundries

GST

received

(Increas

e L)

Bank (increase cash at bank) = Total of other columns

Totals of cash receipts for each vertical column=total Dr. or Cr for related

Ledger Accounts.

Key Ledger Accounts relate to CRJ

CRJ

Cash Sales

Cost of Sales

Debtors

GST (received)

Sundries

Ledger Accounts

Sales

Cash at Bank

Cost of sales

Stock control

Debtors Control (under different

debtor’s name)

Cash at Bank

GST Clearing

Depends

-Capital

-Interest on Investment/received

**************************************Your work*******************************

Example of Cash Payments Journals (Figure 5.4, p87)

0

0