Income Tax

advertisement

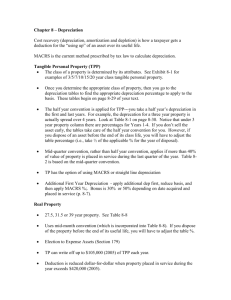

Income Tax Chapter 10 (Depreciation, Cost Recovery, Amortization and Depletion ) I) Introduction A) To be eligible for depreciation or cost recovery, property must be: 1. Used in a trade or business or held for production of income 2. Subject to wear, tear, and/or obsolescence 3. Must have a limited life B) Important terminology 1. Tangible vs. intangible 2. Real property vs. personal property a. Office Building b. Residence c. Dump truck 3. Residential rental vs. nonresidential real property 4. Allowed vs. allowable II) Depreciation A) Pre 1981 Rules 1. Commonly used methods a. S.L.; DDB; 150 DB; 125 DB; SYD b. Various limitations on methods available existed. 2. Must consider salvage value a. Exception - could disregard salvage up to 10% of basis in property 3. Additional 1st year depreciation (bonus depreciation) B) ACRS (Generally property placed in service between 1/1/81 - 12/31/86) 1. Categorizes property into various classes 2. Personal property depreciation rules (for information only) a. Based on 150% DB method with switch over to S.L. (Half year convention) b. Deduction for any one year is equal to the recoverable basis multiplied by the applicable %. (See table 12 page C-11) i. Recoverable basis generally is cost ii. Exception for tangible personal property eligible for investment tax credit placed in service after 12/31/82. a. Must reduce recoverable basis by 2 of I.T.C. claimed or elect a reduced I.T.C. percentage. iii. Personal use property converted to business -- basis is lower of FMV or cost when converted. c. No deduction is allowed in year property is disposed of ! 3. Real Property Depreciation Rules (other than low-income housing) a. Use tables 13 through 16 depending on date placed in service. I. Not all tables are presented. See IRS Pub 534 for additional tables. b. Based on 175% DB with switch to S.L c. Depreciation is available in year of disposal for number of months held. I. Apply mid-month convention where applicable 4. Election of optional S.L.method a. For personal property election applies to all assets in that class for that year. b. For real property election is on a property by property basis 5. Section 179 expensing election a. Amount was limited to 5000 per year through 1986 C) MACRS (after 12/31/86) (GDS) 1. Generally lengthens class lives (see pages 10-6 and 10-7) 2. Personal property a. Generally based on 200% DB with switch to S.L. (Half year convention) b. Mechanics of computations basically same as ACRS (See table 1) c. Mid Quarter Convention applies if more than 40% of value of property placed in service in last quarter (see example 7, page10-7) (Tables 2-5) d. Under MACRS depreciation can be claimed in year of disposition under applicable convention (i.e. half year vs. mid-quarter) e. Straight line method over regular recovery period or extended recovery period may be elected. 3. Real Property a. Must use S.L. b. Residential rental 27.5 years c. Non-residential real property 31.5 years or 39 years 5. Alternative Depreciation System (ADS) a. Generally depreciate over ADR mid-point life (See publication 946) b. 150 DB for certain property or S.L. is available c. If taxpayer will have an alternative minimum tax problem this may be a viable option. 6. Section 179 Expensing election a. Up to $19,000 of cost of tangible personal property can be expensed in 1999. b. Ceiling is reduced dollar for dollar if over $200,000 cost of assets placed in service during year. c. Amount expensed cannot exceed aggregate income derived from any trade or business. d. Watch out for recapture provision if property fails predominate use test. D) Special rules for "Listed Property" 1. What is listed property??? (see page 10-11) 2. Must analyze business use of items to determine appropriate method of depreciation. a. Used more than 50% in trade or business then ACRS and MACRS is available. b. If not used more than 50% -- must use S.L. under A.D.S. life. c. If business use was greater than 50% in 1st year and later falls to less than or equal 50%. There is a special recapture provision. Must use S.L. for remaining life. (even if business usage is greater than 50%) 3. Further restrictions for "Passenger Autos" a. Dollar limitation on annual depreciation deductions for "Passenger Autos" (Luxury auto limitations) b. What is a "passenger auto"? c. In service on or after 1/1/99 ($15,300 cost before limits apply) 1st year -- $3,060 2nd year -- $5,000 3rd year -- $2,950 Succeeding -- $1,775 d. Note these limits assume 100% business use!! 4. Lease inclusion amounts. Theory is to make automobile leases equivalent with luxury automobile deduction limitations. 5. Substantiation requirements for use of listed property! III) Depletion A) Recovery of costs of natural resources B) 2 methods of depletion 1. Cost method 2. Percentage or statutory method a. Certain percentage of gross income from property b. In most cases cannot exceed 100% of taxable income from the property. (Oil and gas properties) IV) Amortization of Intangible (Section 197) A) Applies to certain intangibles acquired after August 10, 1993 B) Amortized ratably over a 15 year period beginning in the month the intangible is acquired.. 1. This period applies regardless of the actual useful life of the intangible C) Will have an impact on the negotiations involved in buying and selling businesses.