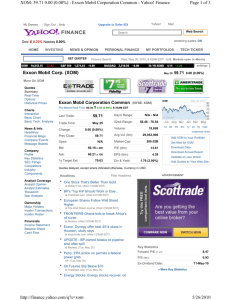

February 28, 2016

NYSE: XOM

EXXON MOBIL CORP

BUY

A+

A

A-

HOLD

B+

B

Annual Dividend Rate

$2.92

B-

C+

C

Annual Dividend Yield

3.56%

SELL

C-

STOCK PERFORMANCE (%)

3 Mo.

Price Change

0.93

D

Beta

0.88

Sector: Energy

XOM BUSINESS DESCRIPTION

Exxon Mobil Corporation engages in refining and

marketing crude oil and natural gas in the United

States, Canada/South America, Europe, Africa,

Asia, and Australia/Oceania.

D+

D-

E+

E

E-

F

Market Capitalization

$340.6 Billion

Sub-Industry: Integrated Oil & Gas

Weekly Price: (US$)

SMA (50)

HOLD

52-Week Range

$66.55-$90.09

RATING SINCE

03/06/2015

Price as of 2/25/2016

$82.01

Source: S&P

SMA (100)

1 Year

2 Years

105

100

95

90

1 Yr.

-8.48

3 Yr (Ann)

-2.21

12 Mo.

-34.28

-50.34

-49.35

3 Yr CAGR

-17.09

-28.88

-26.51

85

80

GROWTH (%)

Last Qtr

-28.46

-57.69

-57.06

Revenues

Net Income

EPS

RETURN ON EQUITY (%)

XOM

Q4 2015

NA

Q4 2014

18.64

Q4 2013

18.72

75

70

Rating History

BUY

Ind Avg

-1.65

23.34

21.81

S&P 500

12.28

14.59

13.97

HOLD

Volume in Millions

200

100

2014

2015

0

2016

COMPUSTAT for Price and Volume, TheStreet Ratings, Inc. for Rating History

P/E COMPARISON

RECOMMENDATION

We rate EXXON MOBIL CORP (XOM) a HOLD. The primary factors that have impacted our rating are mixed some indicating strength, some showing weaknesses, with little evidence to justify the expectation of either a

positive or negative performance for this stock relative to most other stocks. The company's strongest point

has been its strong cash flow from operations. At the same time, however, we also find weaknesses

including feeble growth in the company's earnings per share and a generally disappointing performance in

the stock itself.

21.30

45.00

21.53

XOM

Ind Avg

S&P 500

HIGHLIGHTS

Regardless of the drop in revenue, the company managed to outperform against the industry average of

33.0%. Since the same quarter one year prior, revenues fell by 28.4%. Weakness in the company's revenue

seems to have hurt the bottom line, decreasing earnings per share.

2013

2014

Q3 1.01

Q2 1.00

Q1 1.17

Q4 1.56

Q3 1.89

Q2 2.05

Q1 2.10

Q4 1.91

Q3 1.79

Q2 1.55

Q1 2.12

Q4 0.67

EPS ANALYSIS¹ ($)

2015

NA = not available NM = not meaningful

1 Compustat fiscal year convention is used for all fundamental

data items.

The change in net income from the same quarter one year ago has significantly exceeded that of the Oil, Gas

& Consumable Fuels industry average, but is less than that of the S&P 500. The net income has significantly

decreased by 57.7% when compared to the same quarter one year ago, falling from $6,570.00 million to

$2,780.00 million.

The share price of EXXON MOBIL CORP is down 8.48% when compared to where it was trading one year

earlier. This reflects both (a) the trend in the overall market as well as (b) the sharp decline in the company's

earnings per share. The fact that the stock is now selling for less than others in its industry in relation to its

current earnings is not reason enough to justify a buy rating at this time.

EXXON MOBIL CORP has experienced a steep decline in earnings per share in the most recent quarter in

comparison to its performance from the same quarter a year ago. Earnings per share have declined over the

last two years. We anticipate that this should continue in the coming year. During the past fiscal year, EXXON

MOBIL CORP reported lower earnings of $3.85 versus $7.60 in the prior year. For the next year, the market is

expecting a contraction of 31.8% in earnings ($2.63 versus $3.85).

Net operating cash flow has decreased to $4,336.00 million or 41.52% when compared to the same quarter

last year. In conjunction, when comparing current results to the industry average, EXXON MOBIL CORP has

marginally lower results.

This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Neither TheStreet Ratings nor any other party guarantees its accuracy

or makes warranties regarding results from its usage. Redistribution is prohibited without the express written consent of TheStreet Ratings. Copyright(c) 2006-2015. All rights reserved.

Report Date: February 28, 2016

PAGE 1

February 28, 2016

NYSE: XOM

EXXON MOBIL CORP

Sector: Energy Integrated Oil & Gas Source: S&P

Annual Dividend Rate

$2.92

Annual Dividend Yield

3.56%

PEER GROUP ANALYSIS

-25%

PBR

V

FA

SU

AB

OR

UN

STO

LE

AB

-37.5%

R

VO

FA

Revenue Growth (TTM)

LE

TOT

RDS.A

RDS.B

BP 50%

-200%

EBITDA Margin (TTM)

Companies with higher EBITDA margins and

revenue growth rates are outperforming companies

with lower EBITDA margins and revenue growth

rates. Companies for this scatter plot have a market

capitalization between $19.9 Billion and $340.6

Billion. Companies with NA or NM values do not

appear.

*EBITDA – Earnings Before Interest, Taxes, Depreciation and

Amortization.

52-Week Range

$66.55-$90.09

Price as of 2/25/2016

$82.01

-25%

PBR

V

FA

SU

The Oil, Gas & Consumable Fuels industry is cyclical in nature and is one of the most important globally

because it touches so many others. It is broken down into its component parts by the nature of activity

performed. Upstream activities are related to finding and producing commodities; midstream refers to the

transportation of product from the wellhead to intermediate customers; and, downstream includes the

refining, transformation and marketing of related products. Coal producers are integrated, much like the

players in alternative fuels like uranium. Some of the largest players in the industry are the integrated oil &

gas producers (aka Big Oil).

Close to two-thirds of the world’s energyneeds are satisfied by hydrocarbons (crude oil and natural gas).

Althoughconservation, increased efficiency and substitutes are gaining in prominence,they are not likely to

significantly reduce this dependence in the near future.Crude oil prices have moderated at present due to

lagging economies and newsupplies coming online. In 2004, West Texas Intermediate (WTI) crude oil

brokeout of its historic trading range of $10 to $40 per barrel on a steady climb tomore than $145 per barrel in

June 2008 before crashing to under $40 by the endof 2008. Since then the price of spot crude has climbed

back near the $90 to$110 range before falling again. Natural gas prices, responding to excesssupply, have

retreated to the $2 to $4 range per million BTU (British thermalunit). Coal prices are dependent on the energy

content of the type of coalconsidered and its location, but it, too, has climbed significantly over thepast few

years.

Following nearly 20 years of underinvestment,the supply of crude oil is barely keeping pace with demand.

Longer term demandshould grow at about 1.8% per year, meaning it is expected to grow more than40% over

the next 20 years. Natural gas demand is expected to rise over time,according to the American Petroleum

Institute, as its cleaner-burningproperties increase in value for industry. Coal consumption is projected

togrow at about 1.7% per year over the next 20 years, based on US EnergyInformation Administration

forecasts.

Analysis of companies in this industry beginsby forming a view of the global economy and geopolitics, which

is combined witha supply and demand analysis that leads to commodity price forecasts. At theindividual firm

level, how efficiently a company operates goes a long way indetermining its profitability. Supply management

is an important factor, too,as high commodity prices are affected by how much supply the industry as awhole

produces. Geographic positioning can also be important, as regionaleconomic cycles may not synch up well

with each other.

REVENUE GROWTH AND EARNINGS YIELD

AB

OR

IMO

LE

The so-called “supermajor” integrated oilcompanies include Exxon Mobil (XOM), BP Plc (BP), Chevron (CVX),

Total SA(TOT), and ConocoPhillips (COP). Some of the other major Exploration &Production firms include

Norsk Hydro (NHYDY), Anadarko Petroleum (APC), DevonEnergy (DVN) and Apache (APA). On the Refining &

Marketing level, majorplayers include Valero Energy (VLO), Sunoco (SUN), and Tesoro (TSO). The

majoruranium producer is Cameco (CCJ).

TOT

PEER GROUP: Oil, Gas & Consumable Fuels

UN

LE

AB

-37.5%

R

VO

FA

Revenue Growth (TTM)

Market Capitalization

$340.6 Billion

INDUSTRY ANALYSIS

REVENUE GROWTH AND EBITDA MARGIN*

OXY

Beta

0.88

-40%

XOM

OXY STO

CVX

RDS.A

RDS.B

BP

5%

Earnings Yield (TTM)

Companies that exhibit both a high earnings yield

and high revenue growth are generally more

attractive than companies with low revenue growth

and low earnings yield. Companies for this scatter

plot have revenue growth rates between -37.1% and

-25.6%. Companies with NA or NM values do not

appear.

Ticker

XOM

BP

OXY

STO

SU

IMO

PBR

RDS.A

RDS.B

CVX

TOT

Recent

Company Name

Price ($)

EXXON MOBIL CORP

82.01

BP PLC

28.66

OCCIDENTAL PETROLEUM CORP

69.65

STATOIL ASA

13.98

SUNCOR ENERGY INC

24.65

IMPERIAL OIL LTD

31.50

PETROLEO BRASILEIRO SA- PETR

3.50

ROYAL DUTCH SHELL PLC

45.06

ROYAL DUTCH SHELL PLC

45.30

CHEVRON CORP

85.30

TOTAL SA

44.37

Market

Cap ($M)

340,568

88,296

53,194

44,577

35,644

26,699

19,887

179,679

179,679

160,633

108,884

Price/

Earnings

21.30

NM

NM

NM

NM

23.86

NM

75.10

75.50

34.82

20.26

Net Sales

TTM ($M)

238,926.00

222,894.00

12,480.00

52,551.33

29,208.00

25,214.00

108,576.00

264,960.00

264,960.00

122,566.00

143,421.00

Net Income

TTM ($M)

16,150.00

-6,482.00

-7,829.00

-4,235.28

-1,995.00

1,122.00

-8,751.00

1,939.00

1,939.00

4,587.00

5,087.00

The peer group comparison is based on Major Integrated Oil & Gas companies of comparable size.

This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Neither TheStreet Ratings nor any other party guarantees its accuracy

or makes warranties regarding results from its usage. Redistribution is prohibited without the express written consent of TheStreet Ratings. Copyright(c) 2006-2015. All rights reserved.

Report Date: February 28, 2016

PAGE 2

February 28, 2016

NYSE: XOM

EXXON MOBIL CORP

Sector: Energy Integrated Oil & Gas Source: S&P

Annual Dividend Rate

$2.92

Annual Dividend Yield

3.56%

COMPANY DESCRIPTION

Exxon Mobil Corporation engages in refining and

marketing crude oil and natural gas in the United States,

Canada/South America, Europe, Africa, Asia, and

Australia/Oceania. It also manufactures and markets

commodity petrochemicals, including olefins, aromatics,

polyethylene and polypropylene plastics, and specialty

products; and transports and sells crude oil, natural gas,

and petroleum products. Exxon Mobil Corporation was

formerly known as Exxon Corporation and changed its

name to Exxon Mobil Corporation in November 1999.

Exxon Mobil Corporation was founded in 1870 and is

headquartered in Irving, Texas.

EXXON MOBIL CORP

5959 Las Colinas Boulevard

Irving, TX 75039

USA

Phone: 972-444-1000

http://corporate.exxonmobil.com

Employees: 75000

Beta

0.88

Market Capitalization

$340.6 Billion

52-Week Range

$66.55-$90.09

Price as of 2/25/2016

$82.01

STOCK-AT-A-GLANCE

Below is a summary of the major fundamental and technical factors we consider when determining our

overall recommendation of XOM shares. It is provided in order to give you a deeper understanding of our

rating methodology as well as to paint a more complete picture of a stock's strengths and weaknesses. It is

important to note, however, that these factors only tell part of the story. To gain an even more comprehensive

understanding of our stance on the stock, these factors must be assessed in combination with the stock’s

valuation. Please refer to our Valuation section on page 5 for further information.

FACTOR

SCORE

0.5

Growth

out of 5 stars

weak

Measures the growth of both the company's income statement and

cash flow. On this factor, XOM has a growth score better than virtually

none of the stocks we rate

strong

2.5

Total Return

out of 5 stars

weak

Measures the historical price movement of the stock. The stock

performance of this company has beaten 40% of the companies we

cover.

strong

4.5

Efficiency

out of 5 stars

weak

Measures the strength and historic growth of a company's return on

invested capital. The company has generated more income per dollar of

capital than 80% of the companies we review.

strong

3.5

Price volatility

out of 5 stars

weak

Measures the volatility of the company's stock price historically. The

stock is less volatile than 60% of the stocks we monitor.

strong

5.0

Solvency

out of 5 stars

weak

Measures the solvency of the company based on several ratios. The

company is more solvent than 90% of the companies we analyze.

strong

4.5

Income

out of 5 stars

weak

Measures dividend yield and payouts to shareholders. The company's

dividend is higher than 80% of the companies we track.

strong

THESTREET RATINGS RESEARCH METHODOLOGY

TheStreet Ratings' stock model projects a stock's total return potential over a 12-month period including both

price appreciation and dividends. Our Buy, Hold or Sell ratings designate how we expect these stocks to

perform against a general benchmark of the equities market and interest rates. While our model is

quantitative, it utilizes both subjective and objective elements. For instance, subjective elements include

expected equities market returns, future interest rates, implied industry outlook and forecasted company

earnings. Objective elements include volatility of past operating revenues, financial strength, and company

cash flows.

Our model gauges the relationship between risk and reward in several ways, including: the pricing drawdown

as compared to potential profit volatility, i.e.how much one is willing to risk in order to earn profits; the level of

acceptable volatility for highly performing stocks; the current valuation as compared to projected earnings

growth; and the financial strength of the underlying company as compared to its stock's valuation as

compared to projected earnings growth; and the financial strength of the underlying company as compared

to its stock's performance. These and many more derived observations are then combined, ranked, weighted,

and scenario-tested to create a more complete analysis. The result is a systematic and disciplined method of

selecting stocks.

This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Neither TheStreet Ratings nor any other party guarantees its accuracy

or makes warranties regarding results from its usage. Redistribution is prohibited without the express written consent of TheStreet Ratings. Copyright(c) 2006-2015. All rights reserved.

Report Date: February 28, 2016

PAGE 3

February 28, 2016

NYSE: XOM

EXXON MOBIL CORP

Sector: Energy Integrated Oil & Gas Source: S&P

Annual Dividend Rate

$2.92

Annual Dividend Yield

3.56%

Consensus EPS Estimates² ($)

IBES consensus estimates are provided by Thomson Financial

Beta

0.88

Market Capitalization

$340.6 Billion

52-Week Range

$66.55-$90.09

Price as of 2/25/2016

$82.01

FINANCIAL ANALYSIS

Sales and net income fell significantly, but still managed to outperform when compared to the average

company in its industry.

STOCKS TO BUY: TheStreet Quant Ratings has identified a handful of stocks that can potentially TRIPLE in the

next 12-months. To learn more visit www.TheStreetRatings.com.

0.35

Q1 FY16

2.63 E

3.99 E

2016(E)

2017(E)

INCOME STATEMENT

Net Sales ($mil)

EBITDA ($mil)

EBIT ($mil)

Net Income ($mil)

Q4 FY15

54,437.00

NA

NA

2,780.00

Q4 FY14

76,085.00

9,960.00

5,502.00

6,570.00

Q4 FY15

3,700.00

NA

38,700.00

NA

Q4 FY14

4,658.00

349,493.00

29,121.00

174,399.00

Q4 FY15

NA

NA

NA

NA

NA

NA

Q4 FY14

17.91%

13.09%

7.23%

1.04

9.30%

18.64%

Q4 FY15

NA

NA

NA

NA

Q4 FY14

0.82

0.14

68.00

80.91

Q4 FY15

4,156

0.73

0.67

NA

NA

18,582,961

Q4 FY14

4,201

0.69

1.56

41.51

NA

14,259,220

BALANCE SHEET

Cash & Equiv. ($mil)

Total Assets ($mil)

Total Debt ($mil)

Equity ($mil)

PROFITABILITY

Gross Profit Margin

EBITDA Margin

Operating Margin

Sales Turnover

Return on Assets

Return on Equity

DEBT

Current Ratio

Debt/Capital

Interest Expense

Interest Coverage

SHARE DATA

Shares outstanding (mil)

Div / share

EPS

Book value / share

Institutional Own %

Avg Daily Volume

2 Sum of quarterly figures may not match annual estimates due to

use of median consensus estimates.

This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Neither TheStreet Ratings nor any other party guarantees its accuracy

or makes warranties regarding results from its usage. Redistribution is prohibited without the express written consent of TheStreet Ratings. Copyright(c) 2006-2015. All rights reserved.

Report Date: February 28, 2016

PAGE 4

February 28, 2016

NYSE: XOM

EXXON MOBIL CORP

Sector: Energy Integrated Oil & Gas Source: S&P

Annual Dividend Rate

$2.92

Annual Dividend Yield

3.56%

Beta

0.88

Market Capitalization

$340.6 Billion

52-Week Range

$66.55-$90.09

Price as of 2/25/2016

$82.01

VALUATION

HOLD. The current P/E ratio indicates a significant discount compared to an average of 45.00 for the Oil, Gas

& Consumable Fuels industry and a value on par with the S&P 500 average of 21.53. The price-to-sales ratio is

below both the S&P 500 average and the industry average, indicating a discount. After reviewing these and

other key valuation criteria, EXXON MOBIL CORP proves to trade at a discount to investment alternatives

within the industry.

2 Year Chart

$110

Price/Earnings

$100

XOM 21.30

Peers 45.00

• Discount. A lower P/E ratio than its peers can

signify a less expensive stock or lower growth

expectations.

• XOM is trading at a significant discount to its peers.

HOLD: $85.63

BUY: $96.31

RATINGS HISTORY

Our rating for EXXON MOBIL CORP has not

changed since 3/6/2015. As of 2/25/2016, the stock

was trading at a price of $82.01 which is 9.0% below

its 52-week high of $90.09 and 23.2% above its

52-week low of $66.55.

$90

$80

2014

2015

1

2

3

premium

Price/Projected Earnings

1

2

From

Buy

Buy

To

Hold

Buy

5

3

4

5

XOM 20.55

Peers 23.35

• Premium. A higher price-to-projected earnings ratio

than its peers can signify a more expensive stock

or higher future growth expectations.

• XOM is trading at a significant premium to its peers.

(as of 2/25/2016)

32.19% Buy - We believe that this stock has the

opportunity to appreciate and produce a total return of

more than 10% over the next 12 months.

35.29% Hold - We do not believe this stock offers

conclusive evidence to warrant the purchase or sale of

shares at this time and that its likelihood of positive total

return is roughly in balance with the risk of loss.

32.52% Sell - We believe that this stock is likely to

decline by more than 10% over the next 12 months, with

the risk involved too great to compensate for any

possible returns.

TheStreet Ratings

14 Wall Street, 15th Floor

New York, NY 10005

www.thestreet.com

Research Contact: 212-321-5381

Sales Contact: 866-321-8726

Price/Book

1

2

3

premium

4

5

Price/Sales

1

2

premium

3

4

5

Price to Earnings/Growth

4

5

discount

1

2

3

premium

4

5

discount

XOM NM

Peers 3.23

• Neutral. The PEG ratio is the stock’s P/E divided by

the consensus estimate of long-term earnings

growth. Faster growth can justify higher price

multiples.

• XOM's negative PEG ratio makes this valuation

measure meaningless.

Earnings Growth

1

2

3

4

lower

5

higher

XOM -49.35

Peers -196.34

• Higher. Elevated earnings growth rates can lead to

capital appreciation and justify higher

price-to-earnings ratios.

• XOM is expected to have an earnings growth rate

that significantly exceeds its peers.

Sales Growth

discount

XOM 1.43

Peers 1.76

• Discount. In the absence of P/E and P/B multiples,

the price-to-sales ratio can display the value

investors are placing on each dollar of sales.

• XOM is trading at a discount to its industry on this

measurement.

3

XOM 11.25

Peers 15.07

• Discount. The P/CF ratio, a stock’s price divided by

the company's cash flow from operations, is useful

for comparing companies with different capital

requirements or financing structures.

• XOM is trading at a significant discount to its peers.

discount

XOM NA

Peers 8.19

• Neutral. A lower price-to-book ratio makes a stock

more attractive to investors seeking stocks with

lower market values per dollar of equity on the

balance sheet.

• Ratio not available.

2

premium

discount

Price reflects the closing price as of the date listed, if available

RATINGS DEFINITIONS &

DISTRIBUTION OF THESTREET RATINGS

1

Price/CashFlow

discount

premium

MOST RECENT RATINGS CHANGES

Date

Price

Action

3/6/15

$85.63 Downgrade

2/25/14

$96.31 No Change

4

1

2

3

lower

4

5

higher

XOM -34.28

Peers -16.02

• Lower. A sales growth rate that trails the industry

implies that a company is losing market share.

• XOM significantly trails its peers on the basis of

sales growth

DISCLAIMER:

The opinions and information contained herein have been obtained or derived from sources believed to be reliable, but

TheStreet Ratings cannot guarantee its accuracy and completeness, and that of the opinions based thereon. Data is provided

via the COMPUSTAT® Xpressfeed product from Standard &Poor's, a division of The McGraw-Hill Companies, Inc., as well as

other third-party data providers.

TheStreet Ratings is a division of TheStreet, Inc., which is a publisher. This research report contains opinions and is provided

for informational purposes only. You should not rely solely upon the research herein for purposes of transacting securities or

other investments, and you are encouraged to conduct your own research and due diligence, and to seek the advice of a

qualified securities professional, before you make any investment. None of the information contained in this report constitutes,

or is intended to constitute a recommendation by TheStreet Ratings of any particular security or trading strategy or a

determination by TheStreet Ratings that any security or trading strategy is suitable for any specific person. To the extent any of

the information contained herein may be deemed to be investment advice, such information is impersonal and not tailored to the

investment needs of any specific person. Your use of this report is governed by TheStreet, Inc.'s Terms of Use found at

http://www.thestreet.com/static/about/terms-of-use.html.

This report is for information purposes only and should not be considered a solicitation to buy or sell any security. Neither TheStreet Ratings nor any other party guarantees its accuracy

or makes warranties regarding results from its usage. Redistribution is prohibited without the express written consent of TheStreet Ratings. Copyright(c) 2006-2015. All rights reserved.

Report Date: February 28, 2016

PAGE 5