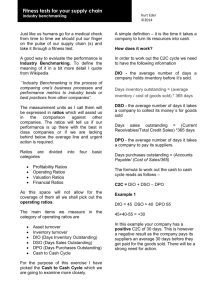

Working Capital Management

Freeing cash flow

in your business

pwc.com.au/privateclients

Executive summary

Your company is growing. Sales are skyrocketing, you’re taking on

new people and you’re looking at expanding. Business is booming

and everything’s in order. Right?

If you scratch below the surface, you may find everything is not

alright – in fact, some things may be very wrong.

When you are not sure if your next sale will result in increased cash

flow, you may be ‘growing broke’ and this publication is for you.

2

PwC

When things are looking good and

you’re focused on taking your business

to the next level, it can be easy to look at

the big picture; but like so many things

in life, the devil is in the detail.

When you consider growing your

business, you’re most likely driven by the

desire to increase your customer base,

win market share and expand into new

products and markets.

Ambitious growth strategies – in

particular those which shift the

attention from managing the here and

now to focusing on the end result – can

have unpleasant side effects.

These unforeseen consequences cannot

only deprive a business of cash flow from

a build up of inventories and accounts

receivables, but also result in inefficient

operational processes and sub-optimal

capital management. This can lead to

lower returns on assets, riskier capital

structures, stress on dividends and

depressed business valuations.

With a diverse range of clients across a

wide range of industries, our combined

experience has taught us that private

businesses must balance growth and

profitability with actively managing

working capital. The most successful

companies manage not only the profit

and loss statement, but also the balance

sheet and working capital.

Working capital management (WCM)

focuses on maintaining efficient levels

of both current assets and current

liabilities. It ensures a company has cash

flow in order to meet its short-term debt

obligations and operating expenses,

which can be a particular challenge

during periods of strong growth.

Given the time it takes to recognise

profit and generate positive cash flow,

businesses undergoing rapid growth

without a WCM system in place can be

starved of funds.

By adopting a working capital

management system that

includes effective management

of debtors, procurement and

supply chain, a company can

improve earnings and cash flow.

WCM can benefit any business at any

stage in its life cycle.

By implementing performance

improvement initiatives and

reducing working capital

intensity, the finance function

can have a direct link to

increasing the value of the

business.

This focus can shift the role of the

finance team from a perceived cost

centre to playing a vital strategic role

in the business.

In order to achieve maximum savings

from WCM programs, businesses must

address the often hidden relationships

and levers between different

components of working capital across

the business.

For this to be successful WCM initiatives

need the commitment and support of

your leadership team.

Significant improvements in WCM

should be a strategic focus of the finance

function, as businesses often hold more

working capital than necessary.

“ WCM can benefit any business

at any stage in its life cycle.”

This publication looks at:

• The benefits of efficient working capital management and the impact on business value.

• A case study demonstrating the potential to release cash by reverse engineering

common working capital metrics.

• Identifying the main levers of inventory, receivables and payables balances.

• Linking the operating elements of working capital to value creation.

• Common indicators and trigger points to instigate a working capital review.

• PwC’s WCM value proposition.

Working Capital Management

3

There is a clear link

between working

capital management

and business value.

Contents

4

PwC

05

Working capital

management

07

Why do you need to

manage working

capital?

09

Releasing cash flow

through debtors

10

Using creditors to

improve cash flow

11

Freeing cash with

inventory

12

How do I know if I have

a problem?

13

PwC’s working

capital services

14

Conclusion

15

PwC Private Clients

Working capital management

Working capital management (WCM) is the art of minimising

cash absorbed in a businesses operating cycle.

The timing difference between

recognising profit and generating

positive cash flow can create cash flow

or liquidity problems for a business.

This can be the result of costs associated

with acquiring and holding inventory

as payment is required in advance of

making a sale. If the sale is made on

credit terms, it takes even more time

to collect the cash. Depending on the

industry, this cycle could take in excess

of ninety days, meaning the business

must fund this timing difference.

When working capital is expressed

in terms of days it is commonly referred

to as the operating cycle of the

business, the cash conversion cycle or

the cash-to-cash cycle (C2C). The C2C

cycle of a business reflects the time in

days it takes for a company to convert

the purchase of inventory into sales and

collect the cash.

The quantification of this timing

difference is known as the working

capital requirement of a business.

The time lag from purchasing inventory

to making a sale and finally collecting

cash creates a timing difference between

profit and cash flow.

Start

DPO

$100,000

purchase inventory

Payment for

inventory due

Inventory sold

to customer

for $130,000

Day 1

Cashflow

Day 30

- $100,000

Day 60

C2C

90 days

• Days inventories outstanding (DIO)

= average number of days that

inventory is held.

• Days sales outstanding (DSO)

= average number of days until

a company is paid by its customers.

• Days payables outstanding (DPO) =

average number of days until a company

pays its suppliers.

DIO

DSO

Customer

pays

Day 120

$130,000

In the above example, if an overdraft is used to fund

working capital throughout the C2C cycle at 10% p.a,

the $30,000 gross margin is reduced by finance costs

of $2,500 or approximately 8.3% of gross margin.

The secret to unlocking cash

flow in the business can be

found in the operations of

the value chain.

Working Capital Management

5

DIO

Supply

chain

strategy

Packaging and

shipping

SKU

management

Storage and

logistics

Supply chain

Management

Production

and

assembly

Volume

forecasting

Production

scheduling

WCM and

C2C cycle

Planning

Sourcing

ns/Logi

sti

ratio

e

cs

Op

Once you view working

capital management as

a system, you can steer,

influence and manage the

drivers to free up cash.

Inventory

(DIO)

WCM

WCM

and C2C

Cycle

M

ar

DSO

en

t

Creditors

(DPO)

m

s&

ke

C 2 C C ycle

ti n

re

S ale

Debtors

(DSO)

g

o

Pr

cu

Sales

strategy

Purchasing

strategy

Pipeline

management

After Sales

Service

Suppliers

evaluation

Planning and

preparation

Sales offers

Cash

collections

and control

Rebates &

discounts

Revenue

Debtor

Management

Credit

control

PwC

Settlement

and cash

management

controls

Procurement

Management

Contract admin

processing

Sales order

processing

Fulfilment

6

Customer

acceptance

DPO

Tendering

and

bidding

Negotiating

and evaluation

Contract

relationship

management

Contracting

Why do you need to manage

working capital?

Alignment with strategy

The C2C cycle can be analysed and

viewed in light of a company’s strategy.

A business that competes on price

should have tight working capital

policies and manage its inventory and

receivables days with discipline. This

includes short credit terms for customers

and the willingness to accept stock-outs in

order to avoid holding excess inventory.

The stage of maturity of an organisation

will also have an impact on the working

capital requirements of a business.

Those that are experiencing fast growth,

declining growth or financial distress

due to a broken capital structure are

most likely to face cash constraints and

therefore require strict WCM.

On the other hand, a niche player is more

inclined to extend favourable credit terms

to reflect a business model that charges

higher prices to its customers.

Net working capital absorption

450m

400m

B

Optimal growth

C Fast growth

A

Sales $

350m

Declining

300m

D growth

250m

200m

F

150m

The goal of working

capital management is

to optimise growth and

move from position C

to A as shown here.

E Financial stress

Downsizing

100m

20m

25m

30m

35m

40m

45m

Net working capital (NWC) $

“ Businesses that ‘grow broke’ typically

experience deteriorating cash,

working capital metrics and exhibit

a lack of accountability.”

Working Capital Management

7

Improving business value

Worked example

The interplay between working capital

absorption and value:

$100 / (20% - 3%) =

$588 or 5.3 times EBITDA

There is a clear link between WCM and value creation.

Assume now the business makes improvements to the

rate of working capital being absorbed into the business

and generates $130 in free cash flow, with risk, growth

and EBITDA remaining constant.

Creating business value is all about generating returns that

exceed the level of risk taken. Cash is said to be king, and

shareholders value growth in their investment.

Therefore business value can be expressed as a function

of three inputs; free cash flow, risk and growth.

Value = Free cash flow/(risk less growth)

The valuation framework would produce a valuation

of $765, calculated as:

$130 / (20% - 3%) =

$765 or 7 times EBITDA

Given the above valuation mechanic there are three

general options available to management for increasing

the value of a company:

1. Increase the cash flow available to debt

and equity providers.

2. Lower risk for the same reward.

3. Increase the rate of growth.

Assume a company generates $100 in free cash flow

and $110 in earnings before interest, tax, depreciation

and amortisation (EBITDA). Risk as measured by the

company’s cost of capital is 20 percent, and based on

historical data the future growth rate is expected to be 3

percent per annum.

Using the valuation framework above, the company

could be valued at $588.

8

PwC

In this example, management can increase

a company’s value through operating

efficiencies focused on working capital

improvements.

Increased efficiencies will lower the capital

invested in the company and therefore

allow surplus cash to be distributed back

to shareholders or reinvested in strategic

initiatives.

It is worth noting that businesses with

inefficient working capital management are

often acquired at a discount.

Releasing cash flow

through debtors

Debtors in a business are

typically monitored and

managed using a profile of

ageing that segments the

balance based on the number

of days outstanding; being 30,

60, 90 and 120 days past due.

Days sales outstanding (DSO) is commonly

calculated by the following formula:

DSO= (Accounts receivable/sales) x days

in period.

Worked example

Consider a private importing business that has annual sales of $100

million and an accounts receivables balance at year end of $15 million.

DSO can be calculated as follows:

$15/$100 x 365 = 55 days of credit sales that are unpaid at the end

of the period.

If the importing business was able to reduce the DSO from 55 days

down to 44 days then the potential to free up cash can be calculated by

reverse engineering the traditional DSO calculation as follows:

Potential to free cash (DSO) = (Sales/days in period x target collection

terms) – accounts receivable balance

Potential to free cash (DSO) = ($100,000,000/365 x 44) – $15,000,000

= $2,945,205

In this example, collecting debts on average in 44 days

instead of 55 days would free up $2.9 million in cash,

which could be returned to shareholders or used to

retire debt.

Common mistakes

• No credit policy.

• No reference checks.

• No progress payments.

• No incentives for early payment.

Working Capital Management

9

Using creditors to improve cash flow

Creditors, like debtors are

typically monitored and

managed using a profile of

ageing that segments the

balance based on the number

of days outstanding; being 30,

60, 90 and 120 days past due.

Worked example

Consider an importing business that has cost of goods sold of

$40 million and an accounts payables balance at year end of $2

million.

DPO would be calculated as follows:

$2/$40 x 365 = 18 days

Days payables outstanding (DPO)

is commonly calculated by the

following formula:

If the importing business increased DPO by 12 days, representing

30 days credit terms, the potential to free up cash can be

calculated as follows:

Days payables outstanding (DPO)

= Accounts payable/cost of

sales x days in period.

Potential to free cash (DPO) = (cost of sales/days in period x

target settlement terms) – existing accounts payable balance.

Potential to free cash (DPO) = ($40,000,000/365 x 30) –

$2,000,000 = $1,287,671

In this example, settling accounts payable in 30

days instead of 18 days would free up almost

$1.3 million in cash, which could be returned to

shareholders or used to retire debt.

However, it is worth noting that days to pay creditors often

depends on working capital management philosophy.

Some companies will deliberately defer settlement or stretch

creditors to preserve cash. Other businesses may pay creditors

quickly to achieve favourable return service and to maintain a

reputation in the local markets in which they operate.

Common mistakes

• Settling creditors too quickly.

• Limited negotiation skills and

lack of focus on payment terms

from buyers.

• Limited controls on the interface

between vendor master files and

online payment systems.

• No centralised procurement

function.

10

PwC

Freeing cash with inventory

Depending on the industry,

inventory can be the largest

component of working capital

that ties cash up in a business.

If inventory is not turned

over regularly it incurs

overheads such as storage,

administration, handling and

insurance. It is also subject

to risk of damage, theft,

deterioration, obsolescence

and may even be perishable.

The amount of inventory held at any

time depends on balancing the holding

costs against the opportunity cost of

stock outs. Therefore, deciding when

an operation should replenish its

inventory is a critical success factor.

From our experience, many companies

overstock simply by purchasing goods

greater than historic usage patterns

which leads to excess working capital.

Worked example

Days inventories outstanding (DIO) is a commonly used key performance

indicator and is calculated by the following formula:

DIO = inventory/cost of sales x days.

Consider an importing business that has cost of goods sold of $40 million,

and stock on hand at year end of $8 million.

DIO would be calculated as follows:

$8/$40 x 365 = 73 days

If the importing business decreased the inventory days by 13, representing

two months worth of stock, the potential to free up cash

can be calculated as follows:

Potential to free cash (DIO) = (cost of sales/ days in

period x target inventory days) – stock on hand.

Potential to free cash (DIO) = ($40,000,000/365 x

60) – $8,000,000 = $1,424,658

In this example, turning over inventory on average

in 60 days instead of 73 days would free up $1.4 million

in cash for the business.

From our experience many

companies overstock

simply by purchasing

goods greater than historic

usage, which drains cash.

Working Capital Management

11

How do I know if I have a problem?

Poor working capital

management can result in

liquidity risk to a business –

it can cause the business to

be in a position where it is

unable to pay its debts as

and when they fall due.

Traditional measures of liquidity

including current and quick ratios

can actually mask systemic working

capital issues.

The current ratio as measured by

the level of current assets compared

to current liabilities has historically

been accepted as being favourable

when it exceeds a ratio of 2:1.

However, this measurement can be

misleading if the organisation has a

poor record of collecting debts and/or

has an accumulation of slow moving

and obsolete inventory.

Common indicators and

triggers for a working

capital review

• The business is generating strong

sales, but never seems to have

enough money.

• The business has deteriorating

cash, working capital metrics and

exhibits a lack of accountability for

managing the balance sheet.

• The business is making profits, but

cash flow is tight.

• You are uncertain if the business

can pay a dividend.

• You find yourself regularly bumping

up against credit limits.

• There is an inability to fund future

capital expenditure needs from

operations.

• You have invested in new systems,

but your cash management

performance hasn’t improved.

• Your bankers are suggesting you

review your operations.

• You never know what your cash

position is.

• You have large differences between

profit and cash flow.

• You are not sure how much cash is

available.

• You have large amounts of money

tied up in inventories and/or

debtors.

• You have difficulties in managing

seasonal fluctuations.

• Your bank overdraft and finance

lines are drawn down.

• You are approaching or have

breached bank covenants.

• You experience difficulty in raising

additional capital.

“Liquidity measures can be ‘fools

gold’ – traditional measures of

liquidity including current and

quick ratios can actually mask

systemic working capital issues.”

12

PwC

• You are planning to sell the business

in the future.

• You are experiencing high levels

of working capital investment

compared to sales revenue.

PwC’s working capital services

Release cash from

operations

Inventory

Accounts

payable

Sales

What we do

We take a practical, operational approach

to improving the value of your business

at a personal level. Our approach goes

further than just an analytical high level

review; we will examine your operations

to identify improvement opportunities to

increase cash flow. Once we’ve worked

with you to uncover how you can do

this, our methodology has identified in

excess of 200 best practice initiatives

that can be implemented to generate

tangible, measurable improvements in the

management of working capital.

We don’t just measure performance,

we improve it.

How we do it

Accounts

receivable

Our approach to unlocking the benefits of

working capital improvements is based on

a best practice gap analysis to determine

if there are opportunities to implement

operational improvements.

Cash

We analyse existing business problems

and develop tailored plans for

improvement by providing specialised,

objective advice based on our knowledge

and expertise in industry best practice.

Best practice is the most efficient and

effective way of accomplishing a task,

based on repeatable procedures that

have proven themselves successful

over time for large numbers of

businesses. A procedure that meets

best practice should achieve the best

results with the least amount of effort.

Benefits

Increasing cash flow will

enable you to reduce the

capital intensity of your

business, allowing you to

increase the return or yield

the business generates.

Increasing free cash flow in the

business will also make the business

more valuable as measured by

enterprise valuation models based on

discounted cash flow techniques.

This means the business will be

worth more, allowing owners the

opportunity to extract additional value

on exit.

Freeing up additional cash also gives

management more options, including:

• The increased ability to pay higher dividends.

• The ability to pay down debt to reduce finance

charges and increase net operating profit.

• Improved credit rating and increased capacity to borrow

and service additional debt to fund future growth.

• The ability to re-invest in the businesses through

additional capital expenditure and research

and development.

• The ability to pass on savings to customers to improve

competitiveness and increase market share.

• Creates flexibility and opportunity to achieve an

optional capital structure for the business.

Typically our working

capital services

pay for themselves,

meaning a net gain

to the business.

Working Capital Management

13

Conclusion

The most successful companies apply the same discipline to capital management as

to managing the profit and loss account. They understand the C2C value chain along

with the working capital levers and actively address the root causes of tied-up cash.

By doing this they make the company more valuable for shareholders and more

attractive to debt providers.

Additional revenue growth

$1,000

$0

Are you growing broke?

Cost of Sales

-$400

After

additional

funding

$0

Gross

margin

$600

Growing broke –

next $1,000

of sales volume

Additional

Debt

+$60

After

working

capital

$(-60)

AR

Days

-$60

AP

Days

+$30

Operating

Expenses

-$300

Fixed

Costs

-$100

Tax

-$63

Inv

Days

-$90

Dividends

-$67

Interest

-$10

Retained

income $60

The marginal cash flow represents the cash inflow generated from

incremental revenue less the cash outflows to cover incremental variable

cost of sales, incremental variable expenses and the incremental

investment in working capital.

In the above example, a fast expanding business is ‘growing broke’. An

additional $1,000 of sales results in earnings, but after working capital

absorption it experiences a $60 cash shortfall, which needs to be funded.

14

PwC

EBIT

$200

PwC Private Clients

PwC Private Clients uses it’s proprietary business improvement process to help private business

owners and individuals improve business performance and realise ambitions. Often the first

step to improve business performance is an assessment of financial health using PwC’s own

financial X-Ray® management tool.

Making the invisible visible

Financial X-Ray® vital

signs report

PwC’s Financial X-Ray® can highlight the

absorption (good or bad) of working capital in a

business to isolate if there is a problem.

The Financial X-Ray® vital signs report allows

businesses to look at management performance,

positive or adverse trends, funding decisions,

the actual cash generated and other meaningful

financial data, including marginal cash flow and

working capital management.

PwC’s Financial X-Ray® is a one-page overview

of a businesses financial results that turns

normal balance sheet and profit and loss

data into meaningful financial management

information.

Working capital metrics can be analysed and

benchmarked against industry standards as well

as management objectives.

Private Clients Advisory – service offering

Horizon 1 services (Definition of business potential)

Horizon 2 services (Roadmap)

•

•

•

•

•

•

•

•

• Financial Health Assessment –

Financial X-Ray®

• Strategy design and strategic planning

• Business model design and review

• Activity based management and

value driver analysis

• Value and wealth creation plans

• Organisational design and evaluation

• Capabilities and resource

assessments

• Decision support analysis – what if Financial X-Ray®

• Growth 100 day action plans

• Waste audits

• Pre-lend reviews

• Credit risk assessments – Bankers X-Ray®

Commercialisation plans, R&D and grant assistance

Commercial due diligence

Market research and industry analysis

Competitor analysis

Customer and product research

Business plan design and review

Business case development

Financial modelling

1. Early stage

Develop products

and services

ss

3.

M

a

•

•

•

•

•

•

•

•

Strategic review and due diligence

Process improvement

Risk management & governance

Balanced and strategic scorecard

design and implementation

Financial improvement plans – X-Ray®

Working capital improvement

tu

Cost reduction & restructuring

rit

Finance function effectiveness

y

Customer, portfolio and margin analysis

Cultural assessments and change management

Remuneration models and employee incentive plans

Succession planning

Corporatisation

Journey to

sustained

performance

ine

•

•

•

•

bus Dev

ine e

s

ma

el

p

lo mod

s

M a n a ge t h e b u s

Horizon 3 services

(Accelerate performance)

2.

G

e

tag

hs

wt

ro

Identify and

define markets

er D

at ev e

ing lo p

syst

ems

Horizon

op

Dev p

n a g e l o st e m

e m ent sy

Working Capital Management

15

pwc.com.au/privateclients

Alister Berkeley

Director, Private Clients

Sydney

Tel: (02) 8266 0022

Mob: 0415 757 492

Email: alister.berkeley@au.pwc.com

© 2013 PricewaterhouseCoopers. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers a partnership formed in Australia,

which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

16 PwC

WL276663