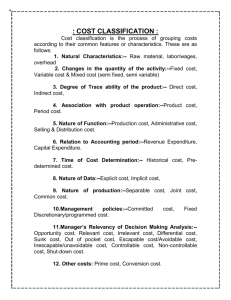

Chapter 2: Objectives Manufacturing Cost Flows Manufacturing

Chapter 2: Objectives

•

•

•

•

•

•

Identify the elements of manufacturing costs

Product versus period costs

Schedule of cost of goods manufactured

Cost behaviour (basics)

Direct versus indirect costs

Economic cost classifications

1

Manufacturing Cost Flows

Balance Sheet

Costs Inventories

Material Purchases Raw Material

Income

Statement

Expenses

Direct Labor

Manufacturing

Overhead

Work in

Process

Selling and

Administrative

Finished

Goods

Period Expenses

Cost of

Goods

Sold

Selling and

Administrative

2

Manufacturing Overhead

All other manufacturing costs

Indirect

Material

Indirect

Labor

Other

Costs

Examples?

3

2-‹#›

Idle Time

Cost of direct labour workers who are unable to perform their assignments due to machine breakdowns, materials shortages, power failures, and other circumstances beyond their control.

Example: A worker is paid $20 per hour for a 40hour work-week and is idle for 4 hours per week due to machine breakdowns, labour would be broken down as follows:

Direct labour

Manufacturing overhead

Total labour cost for the week

4

Overtime Premium

Overtime premiums paid to all factory workers are usually considered to be part of manufacturing overhead.

Why?

Exercise 2-8

5

Product Costs Versus Period Costs

Product costs include: Period costs are:

Inventory

Sale

Cost of Good Sold

Balance

Sheet

Income

Statement

Expense

Income

Statement

6

2-‹#›

Exercise 2-2

•

•

Cost Classification: Direct and

Indirect Costs

Direct costs Indirect costs

Costs that can be easily and conveniently traced to a product or other cost object.

Example of a direct cost for the SOA:

•

•

Costs that must be allocated in order to be assigned to a product or other cost object.

Example of an indirect cost for the SOA:

8

7

Opportunity Cost

The potential benefit that is given up when one alternative is selected over another.

– Wacky Wheatley can earn a contribution margin

(sales less variable costs) of $50 on DVD players and $25 on VCR’s. Based on prior years’ sales,

Wacky expects to sell about 1,000 VCR’s. Since shelf space is limited, Wacky is considering selling only DVD players next year. What is the opportunity cost of selling DVD players?

9

2-‹#›

Sunk Costs

All costs incurred in the past that cannot be changed by any decision made now or in the future.

Example: Wood Company invested $10,000 in a piece of manufacturing equipment two years ago. It has a five-year useful life. A new machine that is more efficient can be purchased today for $15,000; it will have a five year useful life and generate annual savings of $4,000. If the new machine is purchased the old machine will have a $0 trade-in value but can be sold for scrap for $1,000.

Which of these amounts should be included in your analysis of keep the old versus buy the new machine?

10

Differential Revenues & Costs

Costs that differ between alternatives.

Example: You can earn $3,000 per month in Waterloo or

$3,300 per month in the GTA.

Your commuting costs will be $50 per month in Waterloo and $300 per month in the GTA.

Ignoring qualitative factors, should you work in

Waterloo or the GTA?

11

Problems 2-17 & 2-18

12

2-‹#›

Quality Costs

•

•

•

•

Prevention costs are incurred to keep defects from happening.

Appraisal costs are incurred to ensure that defective products, once made, are not shipped to customers.

Internal failure costs are incurred as a consequence of detecting defective products before they are shipped to customers.

External failure costs are the consequences (in terms of repairs, servicing, and lost future business) of delivering defective products to customers.

13

Problem 2-23

14

2-‹#›