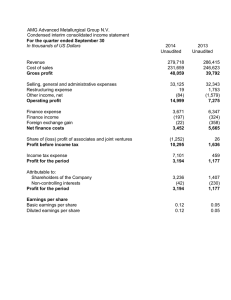

Notes to Consolidated Financial Statements

advertisement