BP financials Financial Analysis of BP Oil Company Abstract The

BP financials

Financial Analysis of BP Oil Company

Abstract

The purpose is to analyze the financial health of BP Oil Company. For this purpose the data for

2011 and 2010 has been used. The company position has also been compared with other competitors in the oil sector. In conclusion, overall performance of the company has been discussed and suggestions have been given.

Summary of Current Financial Performance

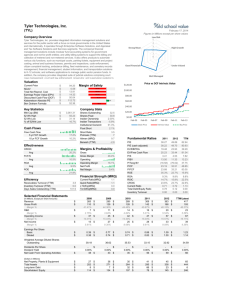

The following table exhibits a ratio analysis of BP’s financial Performance over the period of 2 years

Ratios

Quick Ratio

Ratio Analysis

Formula

Liquidity Ratios

Current Assets/Current

Current Ratio liabilities

{(Current Assetsinventory)/Current liabilities)

Profitability ratios

2011 2010

1.064264 1.083217

0.757973 0.766696

Net Profit Net Income / Sales

Revenue Margin

Return on Assets Net Income /total Assets

Return on equity Net Income /total Equity

Leverage ratios

7%

9%

23%

-1%

-1%

-3%

Degree of operating leverage

Degree of

% change in EBIT / % change in sales -38.87 3.37 financial leverage

% change in EPS/% change in EBIT

Interest coverage ratio EBIT/Interest Expense 31.95586 -3.1641

Debt/Equity ratios Total Debt / Total Equity

60%

86%

90%

96%

Financial Performance of BP

Financial performance of BP Oil Company can be analyzed into following three categories.

Liquidity

Profitability

Leverage

Liquidity

The liquidity ratio analysis determines the cash flow position of the company it identifies whether the revenues and profits earned as per income statement are either the book profits or they are realizing actually in cash flows. The current ratio determines the ability of a company to pay its current liabilities from it current assets however in case of BP we can see that current ratio in 2010 was 1.o8 however in 2011 it was 1.06 it shows that cash flow position of the company has slightly decrease but a current ratio of more than one is usually a good indicator of liquidity .The quick acid test ratio determines a company’s ability to pay of its current liabilities from its most liquid current assets which excludes the inventory .The quick ratio has also decorated slightly but is not a significant change.

Profitability

The profitability of BP has significantly improved in 2011 as compared to 2010 which can b easily evidence by the fact that a loss of 3702 million in 2010 has been replace by a profit of

39817 million in 2011 which is a significant improvement. The major reason for such a remarkable change is the significant improvement in sales revenue of around 80 million in 2011 and a remarkable cost reduction in production and similar tax of around 40 million. however the cost of purchases have increased by 121 million which is not in line with the increase in sales and needs to be controlled in future to further improve the profitability of the company. The return on Assets and Return on Equity of the company are 9% and 23% respectively which is also a sign if improved profitability as profits is increasing resulting in increase return to shareholders.

Leverage

The financial leverage of the company has decrease from 90% to 60 percent but however the operating leverage has increase from 3.37 to 35.37 times .The reason for such significant changes is the turning from losses to profits in 2011.The times interest earned has also turner to

31 times from a negative 3 times from 2010 because in 2010 company does not have sufficient profits to pay of its financial cost but the picture has changes significantly in 2011 where company has enough profits to meet its financial cost .The debt to equity ratio has also declined by 10% in 2011 the reason for this Is not only the decline in long-term debt but also increase in total equity which includes the retain earnings as well (which is increase due to enough profits )

Importance of Industry Comparison and trend analysis

Financial Information is one of the ideal ways to analyze a company’s performance over periods.

Trends can be analyzed over the financial data of a company for a number of years to identify the trends and their movements in different periods. But the financial information of one company does not prove to be sufficient to be analyzing in isolation. A company’s financial result will only provide a reasonable basis for decision making if they are analyze with the financial data of an industry in the same industry or having same circumstances.

Competitors often compare their results with their rivals to identify their position in the market and on the same hand to analyze their performance in comparison to their competitors to formulate their future strategies .For example it is usually said that current ratio of 1 or more than

1 is a good sign of liquidity position but it will depend on industry to industry .a company can compare its current ratio is less than one to another company in the same industry to analyze their standing in that particular industry

An assessment of your company’s financial performance compared with others in its industry

The following table exhibits the comparison of different statistics of BP with its competitors

Direct Competitor Comparison

Ratio

Market

BP CVX XOM Industry

Cap: 134.70B 216.05B 404.46B 73.89B

Employees: 83,400 61,000 82,100 46.58K

Qtrly Rev

Growth

(yoy):

Revenue

(ttm):

-0.05 -0.1 -0.08 0.11

371.81B 224.77B 426.25B 127.11B

Gross

Margin

(ttm): 0.14 0.3 0.28 0.27

EBITDA

(ttm):

Operating

Margin

(ttm):

37.48B 48.51B 64.88B 26.13B

0.06 0.16 0.12 0.12

Net Income 17.65B 24.06B 44.33B N/A

(ttm):

EPS (ttm): 5.53

P/E (ttm): 7.68

PEG (5 yr expected):

P/S (ttm):

4.11

0.36

12.19

9.06

9.46

9.38

-5.39

0.96

3.63

0.95

2.03

10.38

1.21

0.88

Now we can compare the BPs perfromanc with its competitors to analyze its performance in the market and relevant industry. The market capitalization of BP is lower than its both competitors

XOM has around more than double of the market capitalization of BP. However if BP market capitalization is compared with industry average, the BP has a better rate of market capitalization.

BP has a quarterly revenue growth of -0.05 which is far lower than the industry average of 0.11; however its competitors also have a negative revenue growth which can be evidenced by the negative revenue growth of XOM of around -0.08

The gross margin of BP is lower than its industry average and its competitor XOM the gross margin of BP is almost half of the industry gross margin this is the area where BP needs to improve as room for improvement is possible the cost of purchases should be controlled to reduce cogs and increase GP margin. The operating margin of BP is also half of the industry average which shows that operating expense of BP is higher than its competitors in order to improve operating margin BP should take measures to reduce operating cost.

The EPS of BP is better than the industry average which is just 2.03 but the EPS of BP is 5.53 which is almost twice the industry average but the point to notice here is that the two competitors both of them have a higher EPS which shows that its profit per share is higher than BP.

Conclusion

While analyzing the performance of BP over last year we can conclude that BP has made significant improvements a loss of 4 million dollars has been converted in to a profit of 39 million dollars which is a sign of remarkable improvements. The factors to worry about is the increase in purchase cost more than the sales which means that cost of goods sold are increase more than sales which can again turn company into losses the reason for this huge improvement is the reduction in production similar expenses and taxes but BP should take measures to improves its cost of goods sold .However when comparing BP with the industry average we can conclude that the EPS if BP is far better than industry average but room for further improvement is still available .

References

http://mikemckell.wordpress.com/2010/12/10/the-importance-of-industry-analysis-withfinancial-analysis/ http://finance.yahoo.com/q/co?s=BP+Competitors