PowerPoint

advertisement

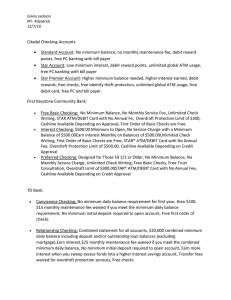

Checking Accounts What Kind of Spender are You? Take the Spending Challenge! U.S. Mint Video 2 Federal Reserve Cont. 3 The Federal Reserve Created 1913 Goal: Economic stability Monetary Policy – Influences growth of money/credit Bank for banks – Payroll, large payments, provide cash Bank for govt. – Taxes go here to pay for military payrolls & SS Supervisor/regulator of banks – Oversee institutions 4 The Role of Banks (private entities) Banks are in business to earn a profit – Interest charged for lending – Interest depositors paid lower than interest bank charges = income Banks provide security – Protect your money’s purchasing power – Banks are regulated 5 The Role of Banks Cont. FDIC (Federal Deposit Insurance Corp) Insures maximum $250,000 Money and financial transactions – Barter Trading good and services without using money Work only if you have something the other person wants Internet: What is FDIC and Purpose 6 10-J History of the Federal Reserve Bank of Kansas City http://www.kc.frb.org 7 Types of Money Currency – paper money & coin Check – order bank to pay sum to person named on check (payee) 8 The New Color Of Money 2006 2008 2004 2003 9 Did you know… Susan B. Anthony $1 coin replaced by Golden Dollar in 2000 $100,000 largest note produced – December, 1934 - January, 1935 – Used for transactions btn FRB – Not circulated to general public $100 note is largest denomination currently issued in United States “In God We Trust” – Didn't appear on U.S. Federal Reserve Notes until Series 1963 currency. 10 Checking Acct video – new one 11 Advantages of Using Checks Safety – Lost or stolen – Replaced – cash can’t! Convenience – Large purchases – Safer to send through mail than cash Records of your transactions – Check – Bank sends statement Written record of all transactions 12 Checking Acct. Types Basic Checking Money Free Market Checking Senior/ Interest Student Bearing Joint Lifeline Checking Express 13 Checking Account Costs Checking account fees – Maintenance fee Flat fee to cover cost of maintaining acct. No matter how many checks you write – Service Charge Charge for each check you write 14 Your Checking Account Open a checking account – 18 or older Signature card Hand out voc. sheet 15 Deposits Deposit form Record your deposit 16 Parts of a Check Check Number Drawer Payee Date written Steven H. Williams 3456 Willow Road Maryville, MO 64468 (660) 562-3234 Amt in figures Written Amt Nodaway Valley Bank Main Street Maryville, MO 64468 (660) 562-0000 :5434564436 Drawee 433567 342 Purpose of check Acct/Routing Numbers Drawer’s Signature 17 Writing a Check Parts of a check – Use ink – Numerical amount vs. handwritten amount – How to fill one out 18 Endorsements Blank – Your name Restrictive – Restricts use – “For Deposit Only” Special – Transfer ownership 19 Check Register and other info Record checks in check register – – – – Record each transaction Record interest Calculate your new balance Record check numbers Overdrawn Stop payment Void Post-dated 20 Your Bank Statement “Reconciliation” Monthly statement – Transactions (deposits/wd) – Bank fees Balancing or reconciling your account Confirm transactions 21 Account Reconciliation Make adjustments – Record any maintenance fees/interest earned in check register! What if the bank made an error? File your records – Canceled checks proof of transaction – Make get back or copy of 23 Do Checking Simulation 1 24 Identity Theft Social Security • Keep confidential Number Tips See flier & booklet • Don’t make it easy to get your number • Don’t give it to anyone • Don’t carry your SS card with you • Report immediately Federal Trade Commission Video & make flier 25 Uses of Electronic Funds Direct deposit Automatic Payment ATM Point of Sale Transaction Stored-value cards Prepaid cards Debit Card Cyberbanking 26 Automated Teller Machines (ATMs) EFT: electronic funds transfer Your ATM card and PIN ATM transactions – savings/checking – ATM deposit – ATM withdrawal Fees Use ATMs responsibly 27 Act: Understanding ATM Fees Internet Search Consumer Protection and Responsibilities Electronic Fund Transfer Act (EFTA) • Requires banks to inform customers of fees • Offer receipt • If lose card, must report 2 days lose up to $50 max • If after 2 days, max. $500 • After 60, you responsible for all loss 28 Different Checks for Different Purposes Certified checks Cashier’s checks Money orders Traveler’s checks 29 Make fliers of different types Certified Check Personal check signed and stamped by bank Guaranteed to have enough money in account to cover check Written to specific payee Low risk Fee: $5-$20 EX: buying 1st house or automobile Taken out of your account & no longer have access to 30 31 Cashier’s Check Bank’s OWN personal check singed by the bank Request amount then pay bank and small service charge Fee approx. $25 Sometimes called bank money order or treasurer’s check Do not need to have checking account EX: buying 1st house or other property 32 33 Money Order Check that draws on money of bank or other financial institution that issued it Different than cashiers – Companies, not just banks, issue – Your name, not the bank, appears on check Fee: $1-$10 Ex: utility payment, phone bill 34 35 Traveler's Check Form of payment often bought before going on trip – $20, $50, $100, and $500 denominations Signed twice before being cashed Safer to use when traveling than cash or personal check Never expire Fee: 1% of amount of checks Can be replaced if lost or stolen 36 Other Services Wire transfers – – – – – Electronic communication Moves money from one acct to another Large sums of money Emergencies Fee: $20-$40 Safe deposit boxes – – – – Individual boxes you rent from bank Store valuables (car titles, birth certificate) Fee: $30-$40 year ID, sign, and have your key and obtain bank’s key to access 37 Do checking simulation 2 and WB, QZ, Review, Test