Chapter 9 Notes

advertisement

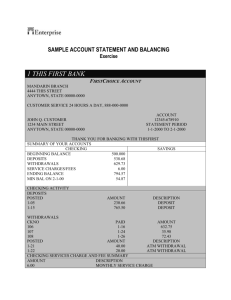

Chapter 9 Checking Accounts and Other Banking Services Lesson 9.1 Checking Accounts I. Purpose of a Checking Account A. B. Checking Account is an account that allows depositors to write checks to make payments Checks—a written order to a bank to pay the stated amount to the person named C. D. Also called Demand Deposit (withdrawn “on demand”) Financial institutions usually charge a fee, or require minimum deposits II. How a Check Travels A. B. C. D. Your payee cashes the check at his/her bank That bank returns it to your bank Your bank withdraws the money from your account and sends it to the other bank Your bank stamps the back of your check (cleared the system) E. Canceled Check—a check that bears the bank’s stamp, it has been paid 1. Use as proof of payment 2. Save as part of your record keeping system F. Advantages of a checking account 1. Provides convenient way to pay bills 2. Safer than using cash (major purchase, pay bills, send in mail) 3. Built-in record keeping system, use to track expenses, create budgets 4. As a customer, you have access to other bank services G. 1. 2. 3. 4. Responsibilities of a Checking Account Write checks carefully and keep accurate records Verify the accuracy of the bank statement monthly (reconcile) Keep canceled checks with your permanent records Truncation—when a bank does not return canceled checks 5. Maintain sufficient funds a. Overdraft—a check written for more money than your account contains b. NSF (not sufficient funds) checks get returned (bounced) c. Bank charges an overdraft fee, can affect credit d. Floating a check—“post-dated check” write a check before the deposit has cleared, illegal and dangerous e. Writing NSF checks can result in fine, imprisonment, or both III. Opening a Checking Account A. Fill out and sign a signature authorization form 1. Bank can compare your signature to the one on the check 2. Some have joint accounts B. Secret question—mother’s maiden name, used for identification IV. Parts of a check A. B. C. D. Check number—pre-numbered by bank ABA Number—(American Bankers Association) identifies the location and district of your bank Maker’s preprinted name and address (drawer), do not print SS number Date—banks may not honor checks over 6 months old E. Payee—the person to whom the check is made payable F. Numeric amount—amount of dollars and cents to be paid, in figures 1. Start close to $ 2. Raise cents above the line of writing G. H. I. Written amount—amount to be paid, written in words 1. Begin writing at far left of line 2. Draw wavy line from cents to “dollars” Signature—bank can compare to signature card Account and Routing Numbers— appears in bank coding at the bottom of each check J. K. Memo—provides place to write the purpose of the check Can purchase blank checks from bank or printing company V. Using Your Checking Account A. Writing Checks 1. Always use a pen—blue or black ink 2. Write legibly 3. Sign your name exactly as it appears on the signature card 4. Avoid mistakes—void (cancel) the check and write a new one. Write the word VOID in large letters across the face of the check, save for your records 5. Have adequate funds in your account B. Paying Bills Online 1. Must register at your bank’s Web site 2. Receive PIN (personal identification number) or password to enter your account 3. Set up a list of payees, enter payment amount. Bank will deduct amount from your checking account and transfer to the payee 4. Be sure to enter in check register 5. Some banks have fees and restrictions-shop around C. Making Deposits 1. a. b. c. d. e. 2. Complete a deposit slip Insert date, write in amount of cash, checks (identify w/ABA number), sub total deposit, subtract cash received, fill in total deposit. Sign if you will be receiving cash back Keep copy of deposit slip as proof of amount of deposit Count money carefully Properly endorse all checks Can make deposits at ATM machines D. 1. 2. 3. 4. Using a Checkbook Register Checkbook register—a booklet used to record checking account transactions Record current amount in balance column Record transaction as soon as you write check or make deposit or payment Write in check number, date, name of payee, purpose 5. Write amount in Payment/Debit column if it reduces balance (checks, online bill payments, debit card purchases, withdrawals, check fees, service charges) 6. Write amount in Deposit/Credit column if it will add to balance (deposits, interest earned) 7. Repeat the amount under the last balance 8. Subtract or add to balance and write in new balance E. Reconciling Your Checking Account 1. 2. Reconciliation—match your checkbook register with the bank statement Do the reconciliation immediately upon receipt of the bank statement to correct any errors made by you or the bank VI. Endorsing Checks A. Blank endorsement—signature of the payee written exactly as it appears on the front of the check. Anyone can cash it if it is lost. B. Special Endorsement—endorsement in full. Transfers the right to cash the check to someone else. “Pay to the Order of [new payee’s name] and the signature of the original payee C. Restrictive Endorsement—restricts or limits the use of the check. “For Deposit Only” Check can only be deposited. Safer than the blank endorsement. VII.Types of Checking Accounts A. Joint Accounts 1. Opened by two or more individuals, survivorship account because if one person dies, the survivor becomes the sole owner 2. “Or” account—either can write checks 3. “and” account—both have to sign B. Special Accounts—small or no fee, fee for services used C. D. E. Standard Accounts—set monthly service fee, but no per-check fee Interest-Bearing Accounts—usually must have minimum balance Share Accounts—from credit unions Lesson 9.2 Other Banking Services I. Guaranteed-Payment Checks A. Certified check—a personal check that the bank guarantees to be good 1. Take your personal check to your bank 2. Bank officer will deduct amount from account and stamp “certified” 3. Service fee--$2.50 to $5.00 B. C. D. Cashier’s check—bank draft. Check by the bank on it’s own funds. Check is guaranteed, you can remain anonymous, banks charge a fee. Money Orders—people who do not wish to use cash, but do not have a account Debit Cards—allow immediate deductions from a checking account to pay for purchases; similar to writing a check E. F. G. H. Bank Credit Cards—VISA, MasterCard Automated Teller Machines—ATM. Most banking transactions can be made through EFT (electronic funds transfer). Must have a PIN number Online and Telephone Bank Stop Payment Orders—request that a bank not cash a specific check. Usually when check has been lost or stolen. Fee--$20 or more I. Safe Deposit Boxes—used to store valuable small items or documents. Rental fees $25--$100 year. 1. Birth, marriage, death certificates 2. Deeds and mortgages 3. Stocks and bonds 4. Jewelry, coin collections J. H. I. Loans and Trusts—cars, homes, vacations, home improvements, college Trustee—a person or institution that manages property for the benefit of someone else under a special agreement Financial Services—purchasing or selling savings bonds, investment services. II. Bank Fees A. B. Banks charge fees to their customers to help cover their operating costs Banks make a lot of money from charging fees, shop around The End!