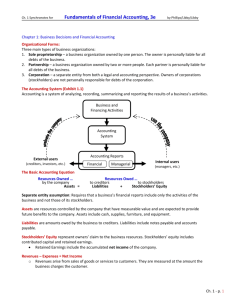

Chapter 5

Financial Reporting and Analysis

PowerPoint Authors:

Brandy Mackintosh

Lindsay Heiser

McGraw-Hill/Irwin

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Learning Objective 5-1

Explain the needs of financial

statement users.

5-2

The Needs of Financial

Statement Users

5-3

Learning Objective 5-2

Describe the environment for

financial reporting, including

the Sarbanes-Oxley Act.

5-4

Accounting Fraud

5-5

Possible Incentives to Commit

Fraud

5-6

Opportunity to Commit Fraud

Internal controls are the methods that a

company uses to protect against theft of assets,

to enhance the reliability of accounting

information, to promote efficient and effective

operations, and to ensure compliance with laws

and regulations.

5-7

Character to Rationalize and

Conceal Fraud

Most fraudsters have a

sense of personal

entitlement, which

outweighs other moral

principles, such as

fairness, honesty, and

concern for others.

5-8

The Sarbanes-Oxley (SOX) Act

5-9

Learning Objective 5-3

Prepare a comparative

balance sheet, multistep

income statement, and

statement of stockholders’

equity.

5-10

Financial Reporting in the U.S.

Enhance

financial

statement

format

Fiscal

Year End

Obtain

independent

external

audit

Release

additional

financial

information

Preliminary

Release of

Key Results

Final

Release of

Annual

Report

Finalize External Audit

Finalize Financial Statements

December

31, 2013

5-11

Middle of

February,

2014

End of

February,

2014

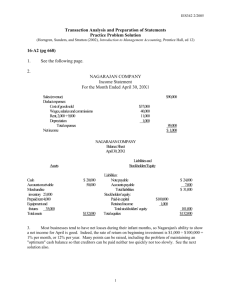

Comparative Financial Statements

ACTIVISION BLIZZARD, INC.

Balance Sheet

(in millions of U.S. dollars)

December 31,

2010

Assets

Current Assets

Cash

Short-term Investments

Accounts Receivable

Inventories

Other Current Assets

Total Current Assets

Property and Equipment, net

Other Noncurrent Assets

Goodwill

Total Assets

Liabilities and Stockholders’ Equity

Current Liabilities:

Accounts Payable

Unearned Revenue

Accrued and Other Liabilities

Total Current Liabilities

Other Noncurrent Liabilities

Total Liabilities

Stockholders’ Equity

Contributed Capital

Retained Earnings (Accumulated Deficit)

Total Stockholders’ Equity

Total Liabilities and Stockholders’ Equity

5-12

December 31,

2009

$ 2,812

696

640

112

1,125

5,385

169

720

7,132

$13,406

$ 2,768

477

739

241

1,104

5,329

138

1,121

7,154

$13,742

$

$

363

1,726

818

2,907

296

3,203

10,146

57

10,203

$13,406

302

1,426

779

2,507

479

2,986

11,117

(361)

10,756

$13,742

A comparative

format reveals

changes over

time.

Multistep Income Statements

ACTIVISION BLIZZARD, INC.

Income Statement

(in millions of U.S. dollars)

Year Ended December 31,

2008

2010

2009

Sales and Service Revenues

Expenses:

Production

Research and Development

Marketing and Sales

General and Administrative

Total Operating Expenses

Income (Loss) from Operations

Revenue from Investments

Income (Loss) before Income Tax

Income Tax Expense (Recovery)

Net Income (Loss)

5-13

$ 4,447

$ 4,279

$ 3,026

2,126

642

520

690

3,978

469

23

492

74

$ 418

2,307

627

544

827

4,305

(26)

18

(8)

(121)

$ 113

1,839

592

464

364

3,259

(233)

46

(187)

(80)

$ (107)

Statement of Stockholders’ Equity

ACTIVISION BLIZZARD, INC.

Statement of Stockholders’ Equity

For the Year Ended December 31, 2010

(in millions of U.S. dollars)

Contributed

Capital

Balances at December 31, 2009

Net Income

Dividends Declared

Issued Shares of Stock

Repurchased Shares of Stock

Balances at December 31, 2010

5-14

Retained

Earnings (Deficit)

$ 11,117

$

(361)

418

(0)

73

(1,044)

$ 10,146

$

57

Learning Objective 5-4

Describe other significant aspects

of the financial reporting process,

including external audits and the

distribution of financial

information.

5-15

Independent External Audit

Auditors are Certified Public Accountants who are

independent of the company.

5-16

Unqualified

Audit Opinion

Qualified

Audit Opinion

Financial

statements are

presented in

accordance with

GAAP

Financial

statements fail to

follow GAAP or not

able to complete

needed tests

Preliminary Releases

Most public companies

announce quarterly and

annual earnings through

a press release that is

sent to news agencies.

5-17

Financial Statement Release

5-18

Securities and Exchange

Commission (SEC) Filings

Public companies are required to electronically

file certain reports with the SEC, including Form

10-K, Form 10-Q, and Form 8-K.

SEC

Filing

Description

Form 10-K Annual filing of financial information

Form 10-Q Quarterly filing of financial information

Form 8-K Reports significant business events

5-19

Learning Objective 5-5

Explain the reasons for, and

financial statement

presentation effects of,

adopting IFRS.

5-20

Globalization and IFRS

International Financial Reporting Standards

(IFRS) are accounting rules established by the

International Accounting Standards Board for

use in over 100 countries around the world.

In 2008, the SEC announced a plan to allow

some U.S. companies to use IFRS in 2009. In

2012, the SEC is still weighing their options as

to whether or not they will require mandatory

use of IFRS and when.

5-21

IFRS Formatting of Financial

Statements

5-22

A side-by-side

comparison of a

balance sheet

prepared using

GAAP and a

statement of

financial position

prepared using

IFRS.

5-23

Learning Objective 5-6

Compare results to common

benchmarks.

5-24

Comparison to Common

Benchmarks

To help interpret amounts on the financial

statements, it’s useful to have points of

comparison or “benchmarks.”

5-25

Prior Periods

Competitors

Time series analysis

compares a company’s

results for one period to

its own results over a

series of time periods.

Cross-sectional analysis

compares the results of

one company with those

of others in the same

section of the industry.

Time Series Analysis Chart

5-26

Cross-Sectional Analysis

5-27

Learning Objective 5-7

Calculate and interpret the

debt-to-assets, asset turnover,

and net profit margin ratios.

5-28

A Basic Business Model

Most businesses can be broken down into 4 elements:

(1) Obtain financing from lenders and investors, which is used to

invest in assets,

(2) Invest in assets, which are used to generate revenues,

(3) Generate revenues, which produce net income,

(4) Produce net income, which is needed to satisfy lenders and

investors.

(2) Assets

generate

(3) Revenues

Investing

(1) Debt & Equity

Financing

5-29

Financing

Operating

(4) Net Income

Financial Statement Ratios

In addition to making it possible to compare

companies of different sizes, a benefit of ratio

analysis is that it enables comparisons between

companies reporting in different currencies

(dollars vs. euros).

5-30

Financial Statement Ratios

The debt-to-assets ratio provides the percentage of

assets financed by debt. A higher ratio means

greater financial risk.

5-31

Financial Statement Ratios

The asset turnover ratio measures how well assets

are used to generate sales. A higher ratio means

greater efficiency.

5-32

Financial Statement Ratios

The net profit margin ratio measures the ability to

generate sales while controlling expenses. A higher

ratio means better performance.

5-33

How Transactions Affect Ratios

Three-step process:

1. Analyze the transaction to determine its effects on the

accounting equation.

2. Relate the effects in step 1 to the ratio’s components,

to determine whether each component increases,

decreases, or stays the same.

3. Evaluate the combined impact of the effects in step 2

on the overall ratio.

5-34

Chapter 5

Solved Exercises

M5-4, M5-5, M5-9, M5-10, E5-8,

E5-11

McGraw-Hill/Irwin

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

M5-4 Preparing and Interpreting a Multistep Income Statement

Nutboy Theater Company reported the following single-step income

statement. Prepare a multistep income statement that distinguishes

the financial results of the local theater company’s core and

peripheral activities. Also, calculate the net profit margin using the

company’s core revenues and compare it to the 8 percent earned in

2012. In which year did the company generate more profit from each

dollar of sales?

5-36

M5-4 Preparing and Interpreting a Multistep Income Statement

NUTBOY THEATER COMPANY

Income Statement

For the year ended December 31, 2013

Revenues

Ticket Sales

Concession Sales

Total Sales Revenues

Operating Expenses:

Salaries and Wage Expense

Advertising Expense

Utilities Expense

Total Operating Expenses

Income from Operations

Other Revenue (Expense):

Interest Revenue

Other Revenue

Income before Income Tax Expense

Income Tax Expense

Net Income

$ 50,000

2,500

52,500

30,000

8,000

7,000

45,000

7,500

$

200

50

7,750

2,500

5,250

Net Profit Margin = Net Income/Total Sales Revenues

= $5,250 / $52,500

= 10%

5-37

M5-5 Preparing a Statement of Stockholders’ Equity

On December 31, 2011, WER Productions reported $100,000 of

contributed capital and $20,000 of retained earnings. During 2012, the

company had the following transactions. Prepare a statement of

stockholders’ equity for the year ended December 31, 2012.

a. Issued stock for $50,000.

b. Declared and paid a cash dividend of $5,000.

c. Reported total revenue of $120,000 and total expenses of $87,000.

5-38

M5-5 Preparing a Statement of Stockholders’ Equity

WER PRODUCTIONS

Statement of Stockholders’ Equity

For the Year Ended December 31, 2012

Balances at December 31, 2011

Net Income

Dividends Declared

Issued Shares of Stock

Balances at December 31, 2012

5-39

Contributed

Capital

Retained

Earnings

Stockholders'

Equity

$100,000

$ 20,000

33,000

(5,000)

$120,000

33,000

(5,000)

50,000

$198,000

50,000

$150,000

$ 48,000

M5-9 Determining the Effects of Transactions on Debt-toAssets, Asset Turnover, and Net Profit Margin

Using the transactions in M5-8, complete the following table by

indicating the sign of the effect (+ for increase, - for decrease, NE for

no effect, and CD for cannot determine) of each transaction.

Consider each item independently.

Transaction

Asset Turnover

Net Profit Margin

a.

Issued 10,000 shares of stock for

$90,000 cash.

-

-

NE

b.

Equipment costing $4,000 was

purchased by issuing a note

payable.

+

-

NE

Recorded depreciation of $1,000 on

the equipment.

+

+

c.

5-40

Debt-to-Assets

-

M5-10 Preparing Comparative Financial Statements

Complete the blanks in the following comparative income

statements, statement of stockholders’ equity, and balance sheets.

(a) Income from Operations

(b)Income before Income Tax Expense

(c) 100

5-41

M5-10 Preparing Comparative Financial Statements

(d) 480

(e) 80 (from December 31, 2012, Balance Sheet)

(f) 120

5-42

M5-10 Preparing Comparative Financial Statements

(g) 480

(h) 180

5-43

End of Chapter 5

5-44