Chapter 1

advertisement

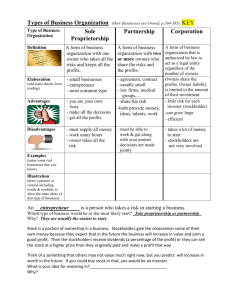

CHAPTER 1 INTRODUCTION TO ACCOUNTING 1-1 LEARNING OBJECTIVE 1 DESCRIBE THE PURPOSE OF ACCOUNTING. 1-2 THE PURPOSE OF ACCOUNTING TO PROVIDE: FINANCIAL INFORMATION ABOUT THE CURRENT OPERATIONS AND FINANCIAL CONDITION OF A BUSINESS TO INDIVIDUALS AND ORGANIZATIONS Keep track of and present financial info $$$$$$$$ 1-3 WHO ARE THE USERS OF ACCOUNTING INFORMATION? Anyone who cares about keeping track of $ 1-4 LEARNING OBJECTIVE 2 DESCRIBE THE ACCOUNTING PROCESS. 1-5 THE ACCOUNTING PROCESS ACCOUNTING IS A SYSTEM OF: GATHERING FINANCIAL INFORMATION ABOUT A BUSINESS AND REPORTING THIS INFORMATION TO USERS 1-6 STEP ONE ANALYZING LOOKING AT EVENTS THAT HAVE TAKEN PLACE AND THINKING ABOUT HOW THEY AFFECT THE BUSINESS 1-7 STEP TWO RECORDING ENTERING FINANCIAL INFORMATION ABOUT EVENTS INTO THE ACCOUNTING SYSTEM 1-8 STEP THREE CLASSIFYING SORTING AND GROUPING SIMILAR ITEMS TOGETHER RATHER THAN MERELY KEEPING A SIMPLE, DIARYLIKE RECORD OF NUMEROUS EVENTS 1-9 STEP FOUR SUMMARIZING THE AGGREGATION OF MANY SIMILAR EVENTS TO PROVIDE INFORMATION THAT IS EASY TO UNDERSTAND 1-10 STEP FIVE REPORTING TELLING THE RESULTS 1-11 STEP SIX INTERPRETING DECIDING THE MEANING AND IMPORTANCE OF THE INFORMATION IN VARIOUS REPORTS 1-12 THE ACCOUNTING PROCESS: SIX MAJOR STEPS ANALYZING RECORDING 1-13 THE ACCOUNTING PROCESS: SIX MAJOR STEPS CLASSIFYING SUMMARIZING 1-14 THE ACCOUNTING PROCESS: SIX MAJOR STEPS REPORTING INTERPRETING 1-15 LEARNING OBJECTIVE 3 DEFINE GAAP AND DESCRIBE THE PROCESS USED BY FASB TO DEVELOP THESE PRINCIPLES. 1-16 GAAP GENERALLY ACCEPTED ACCOUNTING PRINCIPLES DEVELOPED BY THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB) PROCEDURES AND GUIDELINES TO BE FOLLOWED IN THE ACCOUNTING AND REPORTING PROCESS 1-17 LEARNING OBJECTIVE 4 DEFINE THREE TYPES OF BUSINESS OWNERSHIP STRUCTURES. 1-18 THREE TYPES OF OWNERSHIP STRUCTURES SOLE PROPRIETORSHIP PARTNERSHIP CORPORATION 1-19 SOLE PROPRIETORSHIP ONE OWNER OWNER ASSUMES ALL RISK OWNER MAKES ALL DECISIONS 1-20 PARTNERSHIP TWO OR MORE PARTNERS PARTNERS SHARE RISKS PARTNERS MAY DISAGREE ON HOW TO RUN THE BUSINESS 1-21 CORPORATION STOCKHOLDERS STOCKHOLDERS HAVE LIMITED RISK STOCKHOLDERS MAY HAVE LITTLE INFLUENCE ON BUSINESS DECISIONS http://www.citmedialaw.org/legalguide/forming-corporation-california 1-22 LEARNING OBJECTIVE 5 CLASSIFY DIFFERENT TYPES OF BUSINESSES BY ACTIVITIES. 1-23 TYPES OF BUSINESSES SERVICE BUSINESS MERCHANDISING BUSINESS MANUFACTURING BUSINESS 1-24 SERVICE BUSINESS A BUSINESS THAT PROVIDES A SERVICE TRAVEL AGENCY PHYSICIAN COMPUTER CONSULTANT 1-25 MERCHANDISING BUSINESS A BUSINESS THAT BUYS A PRODUCT FROM ANOTHER BUSINESS TO SELL TO CUSTOMERS PHARMACY DEPARTMENT STORE JEWELRY STORE 1-26 MANUFACTURING BUSINESS A BUSINESS THAT MAKES A PRODUCT TO SELL FURNITURE MAKER AUTOMOBILE MANUFACTURER TOY FACTORY 1-27