Lecture 11

advertisement

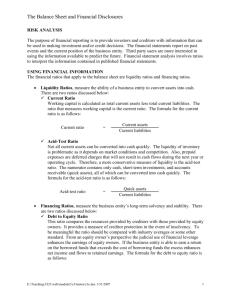

Lecture 11 emad@iqraisb.edu.pk Accounting & Finance. • Accounting is the process of – – Collecting, measuring & recording raw financial data. Organising this data using agreed upon accounting rules and methods to create useful information and communicating the results of the analysis in financial reports and statements. • Finance is the set of activities a company engages in to decide how to – raise, use, and invest money so it generates more cash, profit and capital in the future. • Business finance is about increasing the rate of return on a company's capital to maximize – the market value of stockholders equity. • All of a company's stakeholders are vitally interested in the financial statement that result from the work of the accounting function – • The and the manner in which accountants follow agreed upon rules to prepare those statements. information contained within these statements allows both inside and outside stakeholders to evaluate company performance. • GAAP > Generally Agreed Accounting Principles • Used for ensuring accounting info is reported honestly and accurately. • GAAP is a set of rules & procedures developed over time by accounting experts. • Companies usually employ two different types of accountants: – Internal and – External. • External accountants audit the work of the internal accountant to ensure the company is performing as claimed. • There are three main kinds of financial statement. – A company's balance sheet (statement of financial condition). – Its income statement. – Its statement of cash-flow. • The balance sheet is a summary of the financial position of a business at the end of a specific reporting period. • It reports the main types of assets owned by the company, its liabilities or what it owes and its stockholders equity or what its worth. • The basic equation of accounting is : Assets – Liabilities = Owners Equity • The purpose of the income statement is to summarize and report the results of a company's profit making activities in a specific period. • It is also called a profit and loss statement. • The basic equation used to calculate a company's bottom line profit, the amount of net income or profit company reports on the bottom line of its income statement, is Revenues - Expenses = Profit (or loss) • A company's cash-flow must be managed to ensure the firms short and long term survival. • It shows how much cash a company generates during a specific financial period, where it came from and how the company used it. • In accounting cash refers to the value of a company's asset that can be converted to cash immediately. • Together the – Balance sheet – Income statement – Cash flow statement • Provide the information necessary for stakeholders to analyze the company's performance and the way in which its assets, liabilities, profit and loss are being made and lost, i.e. how it is changing. • Financial ratios are useful because they benchmark the company's performance over time and against the performance of others. • The three main types of ratios utilised are – Liquidity ratios – Asset management ratios – Profitability ratios • Liquidity ratios measure a company's ability to pay its bills when they are due. • A vital short term measure of performance. Current Ratio = Current Assets/Current Liabilities Quick Ratio = Cash + Receivables/Current Liabilities • Asset management ratios measure whether managers have created a business model that will give it the ability to efficiently generate increasing profits over time. Inventory Turnover Ratio = Cost of Good Sold/Inventory Asset Turnover Ratios = Sales/Total Assets • Profitability ratios compare the profit with some other variable such as sales or equity to measure how effectively managers using a company's capital to create profit and cash. Gross Margin Ratio = Gross Profit (Sale – COGS) / Sales * 100 Profit Margin Ration = Net Income/ Sales * 100 • Return on Invested Capital (ROIC) is the ratio most financial analysts use to get a good picture of a company's present and future profitability. ROIC = Net Income/Total Capital Invested • All investments must be compared in terms of their relative risks and returns. The higher the risk the higher the payoff. • Business finance is about increasing the rate of return on a company's capital to maximize the market value of stockholders equity. • Capital investing and budgeting involve developing a plan and budget to manage capital so that it leads to a high ROIC. • A break-even analysis forecasts the revenues and costs associated with a project to locate the point at which the project's sales just cover all of its costs without a profit being earned. • After the break-even point the revenues and profits usually increase quickly. • The goal of capital financing is to obtain the money a company needs to fund its activities at the lowest possible cost. • Securities are investment documents that give investors a legal claim against the assets of a company. • Debt securities are investment documents that provide evidence of a company's legal obligation to repay within a certain amount of time the money it has borrowed, as well as the interest upon it. • Equity securities are the capital stock certificates a company issues giving the owners of the certificates the legal right to a company's assets and the right to receive dividends from any profits the company makes. • An initial public offering (IPO) is the first time the owners of a company offer their stock for sale to the general public. • Four main types of stock are – Blue-chip stocks (prestigious company's stocks IBM, P&G, etc) – Income stocks (low risk and a tradition of high dividends paid to investors) – Growth stocks (potential to generate high dividends in the near future) – Speculative stocks (low sales with potential). • And that’s a basic introduction to the world of business....