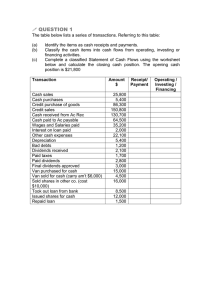

Accounting Lecture 15-Financial Reports (Part 4) Cash Flow Statement Accounting This lecture will cover the following issues: The need to report for cash Cash…..what is it? What is the Cash Flow Statement is used for Purpose of the Cash Flow Statement Classification of cash flows The most important cash flow Format of the Cash Flow Statement • categories of adjusting entry The need to report for cash Owners must have accurate information and revenues and expenses (and therefore profit) if they are to improve the financial performance of their firm. Cash and profit are different measures of performance, and there are many possible reasons why a business that is generating a profit can experience a cash shortage. For example, selling goods to customers on credit 3 Cash…..what is it? Cash refers to money that the business has on hand or in the bank (notes, coins, deposits in bank accounts) Any cash equivalents (investments easily converted to cash e.g. investment in marketable securities) Definition A statement of cash flows shows all inflows (cash receipts) and outflows (cash payments) of cash during the reporting period and the cash balance at the end (a surplus or a deficit). Purpose The purpose is to show the business entity’s ability to pay its debts (i.e. its liquidity) and to finance future growth. • The objective of every business is profit. To determine whether a business earned a profit or incurred a loss, we look to the income statement. • While profit is the objective, cash flow is vital to business success. Indeed, an expression often used is “cash is king”. Cash is the “lifeblood” of business and its efficient management is vital to the continued success of a business. The Cash Flow Statement reports the source of cash and how it was spent over a time period. It measures cash surplus/deficit during the period, which is different from accrual profit/loss. It also complements the two-accrual based financial statements showing financial performance and financial position. What is a Cash Flow Statement used for? It is used for: • evaluating an entity’s ability to generate cash • evaluating management decisions • predicting ability to meet obligations and pay dividends • explaining the difference between accrual accounting profit or loss for the period and changes in cash resources • comparing the operating performance of different entities. Unlike Accrual Accounting, the Cash Flow Report measures cash when it is received. • Cash surplus/deficit will be different to profit and loss reported in accrual accounting. • Cash Flow is important because it determines how the business pays it’s bills, and whether or not it requires credit or a loan to do so. • A healthy cash flow means the business can service it’s own debts without having to borrow money. Cash Flow • Must involve a movement of cash – buying/selling on credit would NOT be reported • Must involve an external party – transfers of cash from one account to another; depreciation; bad debt expense would NOT be reported as they do not result directly in cash flows Summary of Financial Reports: The financial reports companies (and many other businesses) prepare include: Balance Sheet – shows the financial position of the business at a particular date. Contains A, L and OE items Income (Profit and Loss) Statement – shows the financial performance (net profit/loss) of the business for a particular period of time. Contains R and E items. Statement of Cash Flows/Cash Flow Statement – shows the cash inflows and outflows of the business for a particular period. Contains operating, investing and financing items Classification Three types of classification known as “activities” in this statement: 1.Operating 2.Investing 3.Financing Operating (O) Normal regular cash inflows and outflows associated with running the business. Cash in from: • Selling goods, providing services • Interest received on investments • Dividends received on investment (profits earned from investment in shares of another company) Operating (O) Cash out from: •Paying for goods and services •Paying employees (staff) •Paying taxes •Paying interest to lenders (banks) Operating items affect profit/loss amounts (R – E) and usually come from the Income Statement. Operating Activities Cash inflows from Selling goods and services Fees and commissions Interest received Dividends received and Outflows from payments for goods and services payments to employees government charges and taxation interest paid to creditors Operating Activities Operating activities • • • • • • • • • Regular cash inflows/outflows associated with running the business, including: cash collected from selling goods and services cash received for royalties, fees, commissions interest received dividends received payments for goods and services payments to employees payments to government for income and other taxes interest paid to lenders. A large positive operating cash flow is good. This is because it means that the business is collecting more cash than it is paying out from its trading activities. Investing (I) Acquisition (buying) or the disposal (selling) of non-current assets. Cash in (proceeds) from: • Disposal (selling) NCAs • Selling investments in other businesses (SHARES IN OTHER COMPANY) • Collecting loan repayments* Investing (I) Cash out from: • Buying Non Current Assets (NCAs) • Investing in other businesses (BUYING SHARES IN OTHER COMPANY) • Lending money Investing items affect NCAs and usually come from the Balance Sheet. Investing Activities • Cash inflows from – Disposal of assets and investments – Receiving repayment on loans given to others Cash outflows from - Purchasing assets and investments - Lending money to others Financing (F) Cash flows that related to changes in noncurrent liability and equity (i.e. obtain the cash from investors & lenders and paying them back) Cash in (proceeds) from: • Issuing (selling) shares for our company (OE) • Borrowing from banks/others (loans) Financing (F) Cash out from: • Repaying long term loans • Payment of dividends (from retained profits) to our shareholders (OE ) Financing items affect debt (L) and equity (OE) and usually come from the Balance Sheet. Financing Activities • Cash inflows from – Issuing shares in the business – Borrowings Cash outflows from - Repayment of loans - Payment of dividends Financing Activities Financing activities Financing cash inflows/outflows are related specifically to the financing of the business, including cash from investors/banks to establish or support the business, including: • cash received from issuing shares • cash borrowed from banks or others • repayment of long term loans • payment of dividends Format of the Cash Flow Statement • The Direct Method lists all cash flows occurring during the period, classified into the previous three categories: Operating Investing Financing Indirect Method: Reconciliation of Net Cash Flows Please note I will only teach you the Direct Method (Cash Flow Statement format). You will learn how to do the Indirect Method (Cash Flow Statement format) when you go to University. The Cash Flow Statement Cash refers to money that the business has on hand (notes, coins, deposits in bank accounts), any cash equivalents (investments easily converted to cash e.g. deposits) A statement of cash flows shows all inflows (cash receipts) and outflows (cash payments) of cash during the reporting period and the cash balance at the end. The purpose of the statement of cash flows/cash flow statement is to show the business entity’s ability to pay its debts (i.e. its liquidity) and to finance future growth. 25 The Cash Flow Statement For transactions or items to be regarded as a cash flow and be reported in the statement of cash flows: The transaction must involve a movement of cash – transactions like buying/selling goods and services on credit, and purchasing or selling non-current assets on credit would NOT be reported in the statement. The Cash Flow Statement: Direct Method Format of the Cash Flow Statement All cash inflows/outflows that occurred during the period are listed and classified into the previous three categories. The result is a clear picture of how management has been generating and using cash. Greensborough Motorcycles Ltd. Statement of Cash Flows – Year Ended 30 June 2017 Cash flow from operating activities: Receipts: Collections from customers Payments: To suppliers of inventory (70,240) To employees (44,110) For utilities ( 6,430) For insurance ( 5,760) For supplies (11,140) For interest ( 8,970) For advertising ( 7,120) For income taxes ( 6,200) Total cash payments Net cash inflow from operating activities Cash flow from investing activities: Purchase of plant assets (53,500) Sale of plant assets 8,190 Net cash outflow from investing activities Cash flow from financing activities Proceeds from share issue 25,000 Proceeds from loans 32,000 Repayment of long-term loans (20,470) Payment of dividends ( 5,000) Net cash inflow from financing activities Net increase in cash held Cash balance 1 July 2016 Cash balance 30 June 2017 $177,650 ($159,970) $ 17,680 ($ 45,310) $31,530 $ 3,900 $11,700 $15,600 The most important CF Cash flow from operating activities is the most important. This is because it shows the cash provided by the business’ operations. The source of cash is generally considered to be the best measure of a business’ ability to generate sufficient cash to continue into the future Check the journal entry! • Dr Cash • Cr Sales revenue • This one is part of the cashflow and is included • Dr Accounts receivable • Cr Sales revenue • This one is not part of the cashflow and is removed Check the journal entry! • Dr Cash • Cr Accounts receivable • This one is part of the cash flow • Dr Inventory • Cr Accounts payable • This one is not part of the cashflow Check the journal entry • Dr Cash = part of the cashflow Cr Cash = part of the cashflow • Dr Inventory • Cr Cash • Dr Accounts payable • Cr Cash • Dr Prepayment • Cr Cash Check the journal entry • Dr Any other account • Cr Cash • ~ Is an outflow of cash during the period • Dr Cash • Cr Any other account • ~ Is an inflow of cash during the period • Cash accounting, not • Accrual accounting Class Exercise: Direct Method Prepare a classified Statement of Cash Flows for The Great Outdoors Ltd for the year ended 30 June 2018. Cash at 1 July 2017 was $9 245. Assume non-current assets were bought and sold using cash. Class Exercise Solution The Great Outdoors Ltd Statement of Cash Flows for year ended 30 June 2018 $ Cash flows from operating activities: Receipts: Cash Sales 90 000 Collection from customers 32 000 Commission received 1 000 Total cash receipts Payments: To suppliers To employees For electricity For interest For advertising 123 000 (54 (32 (1 (1 (6 040) 060) 150) 660) 450) Total cash payments (95 360) Net cash inflow from operating activities Cash flows from investing activities Proceeds from sale of vehicle Purchase of office equipment Purchase of vehicle 27 640 5 500 (12 300) (23 000) Net cash outflow from investing activities Cash flows from financing activities Proceeds from loan Payment of dividends Repayment of loan Net cash outflow from financing activities Net decrease in cash Bank Balance 1 July 2017 Bank Balance 30 June 2018 $ (29 800) 13 000 (17 900) (4 700) (9 600) (11 760) 9 245 ($ 2 515)