Chapter 1, Introduction to Business Activities and Overview of

advertisement

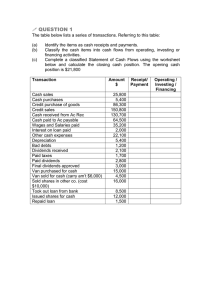

1-1 Chapter 1 -- Introduction to Business and Overview of the Financial Statements and the Reporting Process FINANCIAL ACCOUNTING AN INTRODUCTION TO CONCEPTS, METHODS, AND USES 10th Edition Clyde P. Stickney and Roman L. Weil 1-2 Learning Objectives 1. Develop a general understanding of four principal activities of business firms. 2. Develop a general understanding of the purpose and content of the three principal financial statements. 3. Develop a sensitivity to financial reporting issues. 1-3 Chapter Outline 1. Four principal activities of business. 2. The purpose and content of the three principal financial statements. 3. Financial reporting issues. Chapter Summary 1-4 1. Four principal activities of business firms: (a). (b). (c). (d). Establishing goals and strategies, Obtaining financing, Making investments, and Conducting operations. 1-5 (a). (b). (c). (d). 2. The purpose and content of the three principal financial statements: Balance sheet, Income statement, Statement of cash flows, Notes to the financial statements, including various supporting schedules, (e). Opinion of the independent certified public accountant. 1-6 3. Financial reporting issues: (a). The multiple uses of financial accounting reports, (b). The alternative approaches to establishing accounting measurement and reporting standards, (c). The role of the independent audit of a business firm’s financial statements, and (d). The role of financial reporting in an efficient capital market. 1-7 1.a. Establishing Goals and Strategies Maximize the return to owners of the firm, Provide a stimulating and stable lifetime working environment for employees, and Contribute to and integrate with national goals and policies. 1-8 1.b. Obtaining Financing There are two principal sources of financing: Owners provide funds to a firm and in return have a claim on the firm’s future increases in value. Creditors provide funds to a firm and in return typically require periodic payments including interest fees. 1-9 1.c. Making Investments Investments are the necessary items needed to carry out business activities. Investments may be tangible like land, buildings, equipment, inventories. Or investments may be intangible like patents, licenses and other rights. Other examples are common shares or bonds of other firms, inventories, accounts receivable from customers and cash. 1-10 1.d. Carrying Out Operations The operating activities of a firm: Purchasing – acquiring raw materials for use or products for sale to customers. Production – combines raw materials, labor and other assets to create the output of the firm. Marketing – selling and distribution of the product. Administration – support for the above activities. 1-11 Fig 1.1 -- Overview of Business Activities Investing Financing Operating 1-12 2.a. Balance Sheet Snapshot of the investing and financing activities at a moment in time. The Basic Accounting Equation: Assets = Liabilities + Shareholders’ Equity which is the same ideas as Investing = Financing Resources = Sources of Resources Resources = Claims on Resources 1-13 Exhibit 1.1 -Balance Sheet 1-14 2.b. Income Statement Results of the operating activities of a firm for a specific time period. Basic Income Equation: Net Income = Revenues - Expenses Revenues are the inflows of assets from selling goods and services. Expenses are the outflows of assets used in generating revenues. 1-15 Exhibit 1.2 -- Income Statement 1-16 Relation between Balance Sheet and Income Statement The income statement links the balance sheet at the beginning of the period with the balance sheet at the end of the period. Retained Earnings is increased by net income and decreased by dividends. 1-17 2.c. Statement of Cash Flows Reports details of the where cash came from and where it went to. Cash flows are classified into: Operating, Investing, or Financing. 1-18 Classification of Cash Flows Operations: cash from customers less cash paid in carrying out the firm’s operating activities. Investing: cash paid to acquire noncurrent assets less amounts from any sale of noncurrent assets. Financing: cash from issues of long-term debt or new capital less dividends. 1-19 Exhibit 1.3 -Cash Flows 1-20 Figure 1.2 -- Inflows and Outflows Inflows Operating Sales of Goods or Services to Customers Investing Sales of Noncurrent Assets Financing Issue of Debt and Shareholders’ Equity Outflows Acquisition of Goods or Services for Operations Pool of Cash Acquisition of Noncurrent Assets Dividends and Reduction in Debt or Shareholders’ Equity 1-21 Other Items in Annual Reports Supporting schedules and notes. Auditor’s opinion. Users and uses of financial reports. Authority for establishing acceptable accounting standards. The role of an audit of a firm’s financial statements. Efficiency of capital markets. 1-22 Financial Reporting in the U.S. Legal authority to set accounting standards lies with an agency of the federal government, the Securities and Exchange Commission (SEC). The SEC looks to a private body, the Financial Accounting Standards Board (FASB), for leadership in establishing standards. Pronouncements of the FASB are called Generally Accepted Accounting Standards (GAAP). Since its founding in 1973, the FASB has issued 135 statements and several conceptual papers. 1-23 An International Perspective The process of setting accounting standards vary widely around the world resulting in a diverse set of accounting principles. Globalization of economies has increased the need for comparable and understandable financial information. The International Accounting Standards Committee (IASC) issues recommendations for minimum standards. 1-24 Chapter Summary This chapter provides a broad overview of business activities and how they are reflected in the basic financial statements. The three basic financial statements are introduced. Further chapters examine the concepts and procedures that underlie each statement.