THE COST OF CAPITAL The Cost of Capital

advertisement

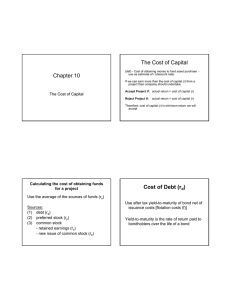

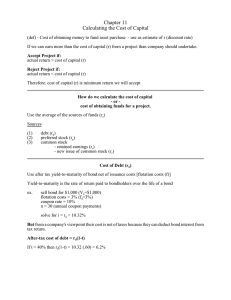

CHAPTER 9: THE COST OF CAPITAL 2 The Cost of Capital: Chapter Outline: 3 The Purpose of the Cost of Capital Capital Components Calculating Component Costs of Capital Calculating the WACC Factors that affect the cost of capital Problem areas in cost of capital The Purpose of the Cost of Capital: 4 The cost of capital—the average rate paid for the use of capital. Primarily used in capital budgeting Used as the ‘hurdle rate,’ or benchmark for projects Compare IRR to this rate Discount cash flows at this rate to find NPV If a project cannot earn above this return, it is not worthwhile The Purpose of the Cost of Capital: 5 It is important to estimate the cost of capital as accurately as possible in order to effectively manage the firm Firm’s cost of capital can be viewed as its required rate of return on projects of average risk Required Rate of Return (Opportunity Cost Rate): 6 The return that must be raised on invested funds to cover the cost of financing such investments Capital Components: 7 Components of firm’s capital are: Debt: Borrowed money, either loans or bonds Common equity: From sale of common shares or from retained earnings Preferred shares: Cross between debt and common equity Capital Components: 8 Capital structure is mix of three capital components Target Capital Structure Mix of capital components that management considers optimal and strives to maintain Basic Definitions: 9 Capital Component: Types of capital used by firms to raise money kd = before tax interest cost kdT = kd(1-T) = after tax cost of debt kps = cost of preferred stock ke = cost of retained earnings ks = cost of issuing new stocks Basic Definitions: 10 WACC: Weighted Average Cost of Capital Capital Structure: A combination of different types of capital(debt and equity) used by a firm Flotation costs 11 DEFINITION of 'Flotation Cost' The costs incurred by the company when it issues new securities. Flotation costs are paid by the company that issues the new securities and includes expenses such as underwriting fees, legal fees and registration fees. Flotation costs: 12 Flotation costs depend on the risk of the firm and the type of capital being raised. The flotation costs are highest for common equity. However, since most firms issue equity infrequently, the per-project cost is fairly small. After-Tax Cost of Debt: 13 The relevant cost of new debt and Used to calculate the WACC. After-tax Cost of Debt = Befor- tax Cost of Debt * (1 - Tax Rate) Taking into account the tax deductibility of interest Cost of Debt: 14 kdT = kd (1-T) kdT = 10% (1 - 0.40) = 6% Use nominal rate. Flotation costs are small, so ignore them. Cost of debt example 15 Cost of debt 16 Nper Pmt Pv Fv Type a\ maturity coupon rate * face value - Debt * (1- floatation) face value 0 Cost of Preferred Stock: 17 Rate of return investors require on the firm’s preferred stock After tax cost of preferred = Dividents / ( price *(1-folatation) ) k ps D ps NP D ps P0 Flotation costs D ps P0 (1 F ) Cost of Preferred Stock: 18 Cost of Retained Earnings: 19 Cost of retained earnings (ks) is the return stockholders require on the company's common stock. Why there is a cost for retained earnings? 20 Earnings can be reinvested or paid out as dividends. Investors could buy other securities, earn a return. If earnings are retained, there is an opportunity cost (the return that stockholders could earn on alternative investments of equal risk). ks is the cost of retained earnings Investors could buy similar stocks and earn ks. Firm could repurchase its own stock and earn ks. Three ways to determine the cost of retained earnings: 21 The CAPM Approach. The Discounted Cash Flow Approach. The Bond-Yield-Plus-Premium Approach. The CAPM Approach: 22 k s k RF + ( kM - kRF )bs ks = kRF + (kM – kRF) β = 7.0% + (6.0%)1.2 = 14.2% The Discounted Cash Flow Approach: 23 Price and expected rate of return on a share of common stock depend on the dividends expected on the stock. P 0 D̂ 1 1 1 + k s D̂ + 2 1 + k s D̂ t t t 1 1 + k s 2 ++ D̂ 1 + k s The Discounted Cash Flow Approach: 24 P 0 D̂ 1 1 1 + k s + D̂ 2 1 + k s 2 ++ D̂ 1 + k s D̂ D̂ t 1 if g is constant t k g t 1 s 1 + k s D̂ 1 k k̂ +g s s P 0 The Discounted Cash Flow Approach: 25 ks = D1 / P0 + g = $4.3995 / $50 + 0.05 = 13.8% The Bond-Yield-Plus-Premium Approach: 26 ks= long-term bond yield + risk premium ks = kd + RP ks = 10.0% + 4.0% = 14.0% k Bon dyi e l d+ Ri sk pre m i u m s 10% + 4% 14% Cost of Newly Issued Common Stock: 27 External equity, ke Based on the cost of retained earnings Adjusted for flotation costs (the expenses of selling new issues) ((Dividends / price) *(1-flotation) ) + growth rate D̂ D̂ 1 1 k + g + g s NP P 1 F 0 28 Cost of Newly Issued Common Stock: 29 The Weighted Average Cost of Capital—The WACC: A firm’s WACC is the average of the costs of the separate sources weighted by the proportion of each source used WACCfirm n weight sourcecost source source 1 To compute a WACC, we need two things: the mix of the capital components in use and the cost of each component Weighted Average Cost of Capital, WACC: 30 A weighted average of the component costs of debt, preferred stock, and common equity Proportion After - tax Proportion Cost of Proportion Cost of cost of + of preferred preferred + of common common of debt debt stock stock equity equity wd k dT + w ps k ps + ws ks Example 15.1: Computing the WACC: 31 Q: Calculate the WACC given the following capital structure. Capital Component Example Debt Value $60,000 Cost 6% Preferred shares 50,000 4 Common shares 90,000 10 $200,000 A: First calculate the capital structure weights. For debt this weight is $60,000 $200,000 = 30%. Next, multiply each component’s cost by its weight. Capital Component Weight Cost $60,000 30% 6% 1.8% Preferred shares 50,000 25% 4 1.0% Common shares 90,000 45% 10 4.5% $200,000 100% Debt Value WACC = 7.3%