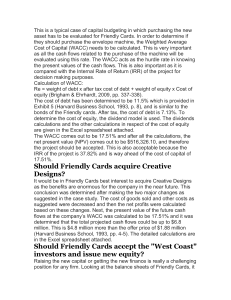

Cost of Capital Analysis: Limitations & WACC

Cost of capital analysis limitations

Cost of capital is the weighted average cost of capital of a company which is composed cost of debt, cost of equity and cost of preferred shares. Let’s analyze each one of them.

Cost of equity uses projected dividends, growth rate and current value of shares. The output is as good as input so if any of the above variables is not correct the cost will not be correct. Projections are based on current economic situation and depend on various statistical models used which might not hold relevant in future. It also uses current value of shares which may not reflect the true value of company because of market factors outside the control of company. The cost of debt uses the existing debt but the new debt might be issued at more favorable or unfavorable terms and hence cost of debt will change accordingly. Preferred shares might be cumulative or non cumulative and hence an adjustment need to be made to WACC for that also.

As the leverage of company changes the cost of debt or equity might change because with more leverage the risk of equity shareholder increases and they expect more return.

The cost of additional debt will also increase the new debt holders will have their claims subdued to existing claims. The risk of the new project might also be different than the existing projects and the existing WACC will not hold good.

These limitations do not invalidate the cost of capital analysis because company still needs an estimate of its cost for accepting new projects and WACC provides the best idea about it. Without the WACC the company will be lost in bidding for new projects and might also accept the projects which will result in loss of shareholder’s wealth.