Budget and Financial Planning Update

advertisement

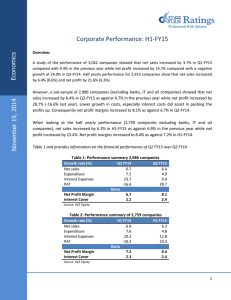

F&A Meeting Sep 30, 2014 Office of Budget and Financial Planning Increasing Fiscal Strength Revenue diversity Financial management Enrollment Student fees State support Grants (federal, state) Other (private, ESS, auxiliaries) Expenditure control Reporting Analysis Multi-year planning Asset base Financial flexibility Physical infrastructure IT infrastructure Deferred maintenance Reserves (net assets) Debt Endowment (investments) FY15 Update • Completed one-on-one VC meetings • Total proposals = $12.5 million • Multi-year forecast, capital plan to System Office (Oct 10) • FY15 recommendation to Chancellor (Oct 17) • Summit Position Management • Lessons learned from FY14 • Planning for FY16 -19 Models of Allocating Resources • Incremental (annual increments) 64% • Formula funded (inputs) 12% • Performance funded (outputs) 4% • Incentive-based (revenue and cost allocation) 20% Salary Budgeting • By employee 85% • Pooled expense 15% Responsibility Centered Management • RCM is a popular response to – – – – lower state funding reduced capacity to increase student fees continued pressure to realize greater efficiencies leaders and managers desire for greater autonomy • RCM is often cited as best practice – Cornell, Georgetown, Columbia, University of Virginia, University of New Hampshire, Rutgers Advantages • Reward for revenue generation and cost effectiveness • Greater transparency on sources and uses of resources • Greater flexibility (responsiveness to change) • More ability to plan and affect future resources • Alignment of authority and accountability Challenges • Change is difficult • Trust, collaboration and a common sense of purpose • Implementation requires ongoing conversations between academic and administrative departments – to manage changes, take advantage of opportunities, and ensure commitment to core mission and values FY14 Expense FY15 Budget Authorization FY15 Budget Proposals FY14 Lessons Learned • Timing of new buildings introduce variability • Capacity to execute, capacity to spend • Need alternative reporting; myths remain • Acknowledge variability (and opportunity); we need greater flexibility FY14 Unspent Budget Authorization Increasing Fiscal Strength • Cost – benefit on where we spend our time • Address structural revenue or expense deficit • Acknowledge variability (and opportunity)