Additional information from the bank statement

advertisement

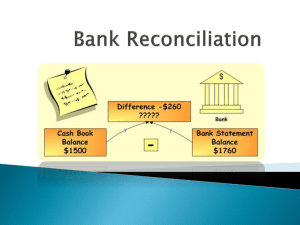

You are given the following information for River Adventures Company: The adjusted cash balance per bank agreed with the cash balance per books at April 30, 2008. The May bank statement showed the following: Additional information from the bank statement: 1. The deposit of $1,650 on May 13 is an electronic transfer from a customer in payment of its account. The amount includes $35 of interest, which River Adventures Company had not previously accrued. 2. The NSF for $440 is for a $425 cheque from a customer, Ralph King, in payment of his account, plus a $15 processing fee. 3. SC represents bank service charges for the month. 4. The bank made an error when processing cheque #564. The company also made two errors in the month. All cheques were written to pay accounts payable; all cash receipts were collections of accounts receivable. The company's cash payments and cash receipts for the month were as follows: Instructions (a) Calculate the unadjusted cash balance in River Adventures' general ledger at May 31. (b) Prepare a bank reconciliation and the necessary adjusting journal entries at May 31. Solution: (a) Book balance, May 1 (per Apr. 30 bank reconciliation) ...........................$ 7,776 Add: Cash receipts ................................................................................................ 6,825 Less: Cash payments .............................................................................................. 13,526 Unadjusted cash balance, May 31 .......................................................................... $ 1,075 (b) RIVER ADVENTURES COMPANY Bank Reconciliation May 31, 2008 Cash balance per bank statement .................................................................................... Add: Deposits in transit................................................................ $1,286 Error in cheque 564 ($603 - $306) ...................................... 297 $4,308 1,583 5,891 Less: Outstanding cheques No. 533 ......................................................................... $279 No. 555 ......................................................................... 79 No. 558 ......................................................................... 943 No. 560 ......................................................................... 890 No. 566 ......................................................................... 950 3,141 Adjusted cash balance per bank...................................................................................... $2,750 Cash balance per books .................................................................................................. $1,075 Add: EFT proceeds ($1,615 + $35) .............................................. Error in May 26th deposit ($980 - $890) ................................................................ Error in cheque #563 ($2,887 - $2,487) .......................................................... $1,650 90 400 2,140 3,215 Less: NSF cheque ......................................................................... $ 440 Bank service charges ........................................................... 25 Adjusted cash balance per books .................................................................................... 465 $2,750 May 31 31 Cash .................................................................... 1,650 Accounts Receivable ..................................... 1,615 Interest Revenue ............................................ 35 Cash .................................................................... 90 Accounts Receivable ..................................... 31 Cash ..................................................................... 90 400 Accounts Payable .......................................... 31 Accounts Receivable—R. King ........................... 400 440 Cash............................................................... 31 Bank Charges Expense ........................................ Cash............................................................... Check: $1,075 + $1,650 + $90 + $400- $440 - $25 = $2,750 adjusted cash balance 440 25 25