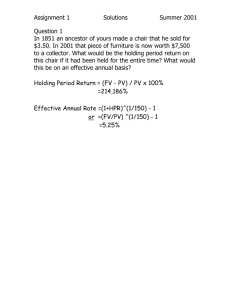

Interest Rates

The Effective Annual Rate (EAR)

◦ Indicates the total amount of interest that will be earned at the end of one year

◦ The EAR considers the effect of compounding

Also referred to as the effective annual yield (EAY) or annual percentage yield (APY)

Adjusting the Discount Rate to Different

Time Periods

◦ If 5% is the effective annual rate what is the 6month rate?

◦ Earning a 5% return annually is not the same as earning 2.5% every six months.

n

(1

r n

)

1

(1.05) 0.5

– 1= 1.0247 – 1 = .0247 = 2.47%

Note: n = 0.5 since we are solving for the six month

(or 1/2 year) rate

Problem

◦ Suppose your bank account pays interest monthly with an effective annual rate of 5%. What is the interest you will earn in one month? What is the interest you will earn in two years?

◦ We know from above that a 5% EAR is equivalent to earning (1.05) 1/12 -1 = .4074% per month.

◦ We can use the same formula to find the two year rate (1.05) 2 – 1 = 10.25% (in particular, not 10%).

The annual percentage rate (APR), indicates the amount of simple interest earned in one year.

◦ Simple interest is the amount of interest earned without the effect of compounding.

◦ The APR is typically less than the effective annual rate (EAR).

◦ APR is simply a communication device.

The APR itself cannot be used as a discount rate (except by accident).

◦ The APR with k compounding periods each year is simply a standardized way of quoting the actual interest earned each compounding period:

Interest Rate per Compounding Period

APR k periods / year

Converting an APR to an EAR

1

EAR

1

APR k

k

◦ The EAR increases with the frequency of compounding.

Continuous compounding is compounding every instant.

◦ If the APR is 6% what are the EARs for different compounding intervals?

Annual compounding: (1 + 0.06/1) 1 – 1 = 6%

Semiannual compounding: (1 + 0.06/2) 2 – 1 = 6.09%

Monthly compounding: (1 + 0.06/12) 12 – 1 = 6.1678%

Daily compounding: (1 + 0.06/365) 365 – 1 = 6.1831%

A 6% APR with continuous compounding results in an

EAR of approximately 6.1837%. This is an abstraction we will not make much use of in this course.

You are offered a chance to buy a perpetuity paying a $100 per year (beginning in one year) for $1,650 today. You are able to borrow and lend money at a 6% APR with monthly compounding. Should you buy the perpetuity?

First we must find the EAR since the perpetuity makes annual payments. The effective annual rate is (1+0.06/12) 12 – 1 = 6.16778%.

The value of the perpetuity is $100/0.0616778

= $1,621.33.

Inflation and Real Versus Nominal Rates

◦ Nominal Interest Rate: The rates quoted by financial institutions and used for discounting or compounding cash flows

◦ Real Interest Rate: The rate of growth of your purchasing power, after adjusting for inflation

Growth in Purchasing Power

1

r r

1

r

1

i

Growth of Money

Growth of Prices

The Real Interest Rate r r

1

1

r i r

i

1

i

r

i

Problem

◦ In the year 2006, the average 1-year Treasury rate was about 4.93% and the rate of inflation was about 2.58%.

◦ What was the real interest rate in 2006?

Solution

◦ Using the equation given above, the real interest rate in

2006 was:

(4.93% − 2.58%) ÷ (1.0258) = 2.29%

Which is approximately equal to the difference between the nominal rate and inflation: 4.93% – 2.58% = 2.35%

An increase in interest rates will typically reduce the NPV of an investment.

◦ Consider an investment that requires an initial investment of $3 million and generates a cash flow of $1 million per year for four years. If the interest rate is 4%, the investment has an NPV of:

NPV 3

1

1

1

1

2 3

(1.04) (1.04) (1.04) (1.04)

4

$0.629 million

◦ Recall the number $0.629 million means something very specific. What is it?

If the interest rate jumps to 15%, the NPV of this investment becomes negative and we would not undertake such a project.

NPV 3

1

1

1

1

2 3

(1.15) (1.15) (1.15) (1.15)

4

$0.145 million

Term Structure: The relationship between the investment term and the interest rate

Yield Curve: A graph of the term structure

When the yield curve is not flat we must discount future cash flows at the appropriate rates.

◦ Compute the present value of a risk-free three-year annuity of $500 per year, given the following yield curve:

January-07

Term (Years)

1

Rate

5.06%

2

3

4.88%

4.79%

Solution

◦ Each cash flow must be discounted by the corresponding interest rate:

PV

$500

$500

$500

2

1.0506

1.0488

1.0479

3

PV

$475.92

$454.55

434.52

$1, 364.99

◦ It is very important to note that even though this is a

3-year annuity, we cannot use the annuity formula to find its present value.

The shape of the yield curve is influenced by interest rate expectations.

◦ An inverted yield curve indicates that interest rates are expected to decline in the future.

Because interest rates tend to fall in response to an economic slowdown, an inverted yield curve is often interpreted as a negative forecast for economic growth.

Each of the last six recessions in the United States was preceded by a period in which the yield curve was inverted.

The shape of the yield curve is influenced by interest rate expectations.

◦ A steep yield curve generally indicates that interest rates are expected to rise in the future.

The yield curve tends to be sharply increasing as the economy comes out of a recession and interest rates are expected to rise.

Risk and Interest Rates

◦ U.S. Treasury securities are considered “risk-free.”

All other borrowers have some risk of default, so investors require a higher rate of return.

◦ The yield curve is commonly presented in terms of risk free yields but one can also examine a AAA or

AA yield curve at any point in time.

When computing the present value of future cash flows that are risky we adjust the discount rate to account for the risk.

Taxes reduce the amount of interest an investor can keep, and we refer to this reduced amount as the after-tax interest rate.

r

r (1

)

Opportunity Cost of Capital: The best available expected return offered in the capital market on an investment of comparable risk and term (investment horizon) to the cash flow being discounted

◦ Also referred to as Cost of Capital