Citi-Presentation-Sep-9

advertisement

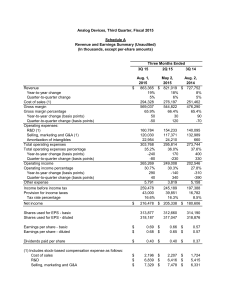

Citi Global Technology Conference Mark Thompson, Chairman, President & CEO September 9, 2015 Notes on Forward Looking Statements and Non-GAAP Measures • Comments in this presentation other than statements of historical fact may constitute forward looking statements and are based on Fairchild’s management’s estimates and projections and are subject to various risks and uncertainties • These risks and uncertainties are described in the Company’s periodic reports and other filings with the Securities and Exchange Commission (see the Risk Factors section) and are available at http://sec.gov and investor.fairchildsemi.com • Actual results may differ materially from those projected in the forward looking statements • Some data in this presentation may include non-GAAP measures that we believe provide useful information about the operating performance of our businesses that should be considered by investors in conjunction with GAAP measures that we also provide. You can find a reconciliation of non-GAAP to comparable GAAP measures at the Investor Relations section of our web site at http://investor.fairchildsemi.com Recent additions to our website at http://investor.fairchildsemi.com Updated Financials (through current quarter with segment revenue/gross margin breakouts) • Quarterly Fact Sheet with current quarter highlights • This investor presentation 2 Agenda Current Demand Environment Q3 Guidance Update Operating Expense Reduction Program Levers to Improve Gross & Operating Margins 3 Current Demand Environment Lower than expected demand from large Asian mobile customer Incrementally weaker demand from China Previous sales guidance for Q3 assumed POS flat to Q2…now trending down 4 – 5% QoQ QTD Book-to-Bill roughly at parity 4 Q3 Guidance Update Sales Gross Margin OPEX Update ≈$340M Previous $355 - 375M 34.0 - 35.0% 34.0 - 35.0% $90 - 92M $95 - 97M 5 Operating Expense Reduction Program $30 - 34M annualized savings across both SG&A and R&D Program implemented by mid-Q4 2015 Drives OPEX to our target of no more than 25% of sales at current levels 6 Levers to Improve Gross & Operating Margins Manufacturing footprint consolidation completed on schedule 80% 70% 60% 50% Greater use of subcons at lower cost 40% Higher ratio of 8” wafers 20% More variable cost structure 75% 30% 10% 0% 40% 35% 7% External Fab 2H14 2H15 40% 20% External A&T % of Wafer Starts in 8" Improved product mix – fastest growing businesses have highest margin OPEX reductions improve operating margin by >200 bps at current revenue levels 7 Key Points Decisive actions taken to reduce OPEX to target at current level of sales Updated sales guidance reflects incrementally weaker demand Factory consolidation completed…significant improvement in Mfg costs Continue to return 100% of excess FCF through stock buybacks 8 THANK YOU