ACCOUNTING IN BUSINESS

advertisement

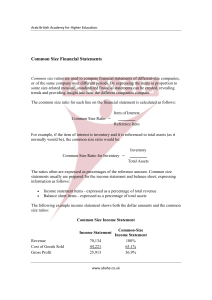

Money Management in the Organizations 1- Accounting activities: Recording and analyzing monetary information 2- Financial activities: Fund (money) raising and investing decisions Accounting Activities 1- Financial accounting: Provide financial information to external parties 2-Managerial accounting: Provide financial information to people (managers) inside the organization to plan, administer and control Comparison of Financial and Managerial Accounting Financial accounting Provides financial information to external parties The objective is to enable outsiders to evaluate organization’s performance Must use Uniform Chart of Accounts Emphasis is on summarized data such as Balance sheet, Income statement and Financial ratios Mandatory for external reports Comparison of Financial and Managerial Accounting-2 Managerial accounting Provides financial information to people inside the organization The objective is to enable managers to plan, direct and control the organizational activites in an effecient way Need not use Uniform Chart of Accounts Emphasis is on detailed departmental reports relevant with every other activity within the organization It is not mandatory Accounting Process 1- Relevant documents: collect receipts, invoices, statements as proof of organizations’ business activities 2- Transactions: Record every business activity by two sets of entries (debit and credit) based on relevant documents 3-The journal account: Enter every transaction into its relevant account in the journal in a chronological order Accounting Process-2 4-The ledger Account: Transfer every journal entry to relevant single account page in ledger 5- Financial statements: Prepare the summarized charts based on ledger accounts which shows the organization’s performance result at the end of the period (balance sheet, cash flow, income statement) 6-Financial ratios: Make analysis of the organizational performance based on financial statements (liqudity ratio, leverage ratio, activity ratio, profitability ratio) Accounting Accounting is the process of identifying, recording, summarizing, evaluating and reporting the monetary information about business activities to the interested parties. People in Accounting Accountants They are the responsible and technically equipped people who are involved in accounting activities. Chartered (certified) accountants provide services related to accounting activities such as auditing, tax work and management consulting to the general public on a fee basis. Certified(chartered ) financial consultants has assumed significant accounting and audit responsibilities of the large companies relating to tax laws and regulations. People in Accounting-2 Independent accounting and financial consultants Independent accountants They are not obligated to swear but have assumed the accounting and audit responsibilities. SOME TERMS IN ACCOUNTING TRANSACTIONS DEALS HANDLED WHEN DOING BUSINESS ACCOUNT THE SUMMARY FORM OF A RECORD OF A PARTICULAR ASSET, LIABILITY OR OWNER’S EQUITY THE JOURNAL (yd) A BOOK IN WHICH ACCOUNTANTS RECORD TRANSACTIONS IN CHRONOLOGICAL ORDER THE LEDGER (d-k) ANOTHER BOOK IN WHICH ALL SEPARATE ACCOUNTS TRANSFERRED FROM THE JOURNAL ARE RECORDED AND KEPT FINANCIAL STATEMENTS BALANCE SHEET INCOME STATEMENT CASH-FLOW STATEMENT (PROFIT AND LOSS STATEMENT) SHOWS FINANCIAL STATUS OF THE ORGANIZATION AT A PARTICULAR INSTANT DATE SHOWS REVENUES, EXPENSES AND NET INCOME(OR LOSS) OF THE ORGANIZATION OVER A PERIOD OF TIME SHOWS CASH RECEIPTS AND CASH PAYMENTS OF THE ORGANIZATION DURING A PERIOD OF TIME FINANCIAL RATIOS – I SHOW THE FINANCIAL-BASED CONNECTIONS BETWEEN THE ACCOUNTS THAT EXIST IN FINANCIAL STATEMENTS LIQUIDITY RATIOS SHOW THE ORGANIZATION’S CASH CAPABILITY TO MEET ITS SHORT-TERM LIABILITIES CURRENT RATIO=CURRENT ASSETS / CURRENT LIABILITIES QUICK RATIO = CURRENT ASSETS(LESS INVENTORY) / CURRENT LIABILITIES LEVERAGE RATIOS SHOW THE RELATIONSHIP BETWEEN ASSETS AND SOURCES OF FUNDS SUPPLIED BY THE CREDITORS AND OWNERS DEBT-TO EQUITY=TOTAL LIABILITIES /OWNER’S EQUITY DEBT-TO-TOTAL ASSETS=TOTAL LIABILITIES /TOTAL ASSETS FINANCIAL RATIOS – II SHOW THE FINANCIAL-BASED CONNECTIONS BETWEEN THE ACCOUNTS THAT EXIST IN FINANCIAL STATEMENTS PROFITABILITY RATIOS SHOW THE ORGANIZATION’S OVERALL FINANCIAL PERFORMANCE INTERMS OF PROFIT GENERATION ABILITY RETURN ON EQUITY(ROE)=PROFITS(AFTER TAX) / OWNER’S EQUITY RETURN ON INVESTMENT(ROTA)=PROFITS (AFTER TAX) / TOTAL ASSETS RETURN ON SALES(ROS)=PROFITS (AFTER TAX) / TOTAL SALES ACTIVITY RATIOS SHOW THE RELATIONSHIP BETWEEN KEY ASSETS AND SALES INVENTORY TURNOVER RAT.=COSTS OF GOODS SOLD /AVERAGE INVENTORY AVERAGE INVENTORY=(BEGINNING INVENTORY+ENDING INVENTORY) / 2 TYPES OF COSTS-I (ACCORDING TO THEIR INVOLVEMENT IN MANUFACTURING OR NON-MANUFACTURING OPERATIONS) MANUFACTURING COSTS DIRECT MATERIAL COSTS DIRECT LABOR COSTS MANUFACTURING OVERHEAD COSTS NON-MANUFACTURING COSTS MARKETTING AND SELLING COSTS ADMINISTRATIVE COSTS TYPES OF COSTS-II (ACCORDING TO THEIR RESPONDING TO CHANGES IN THE LEVEL OF BUSINESS ACTIVITY) VARIABLE COSTS FIXED COSTS (COSTS THAT VARIES IN DIRECT PROPORTION TO CHANGE IN THE LEVEL OF ACTIVITY) (COSTS THAT REMAIN CONSTANT REGARDLESS OF CHANGES IN THE LEVEL OF ACTIVITY) TYPES OF COSTS-III (ACCORDING TO THEIR BEING ASSIGNED INTO SPECIFIC COST OBJECT) DIRECT COSTS INDIRECT COSTS (COSTS DIRECTLY RELATED WITH SPECIFIC COST OBJECT AND THEREFORE BEING DIRECTLY ASSIGNED INTO THOSE) (COSTS THAT ARE NOT DIRECTLY RELATED WITH SPECIFIC COST OBJECT AND THEREFORE CANNOT BE ASSIGNED INTO THOSE SPECIFIC COST OBJECT) COSTING METHODS PROCESS COSTING SYSTEM (USED WHEN ORGANIZATIONS PRODUCE NUMEROUS UNITS OF SINGLE PRODUCTS FOR LONG PERIODS AT A TIME) UNIT COST=TOTAL MANUFACTURING COSTS /TOTAL UNITS PRODUCED JOB-ORDERING COSTING SYSTEM (USED IN COMPANIES WHERE VARIETY OF DIFFERENT PRODUCTS ARE PRODUCED EACH PERIOD) Planning and Control Cost-Volume-Profit (CVP) Analysis A tool in managerial accounting to understand the interrelationship between cost,volume and profit in the organizations. Managers primarily focus on interactions among these elements: -Price of products -Volume of activity -Variable costs per unit -Total fixed costs -Mix of products sold This is vital for planning and decision-making. Planning and Control-2 Break-even Analysis is one of the important elements in cost-volume-profit analysis. It is designed to respond to questions concerning the minimum point of total cost that organizations may suffer without losing money. This point is the break-even point and indicates where organization revenues meet and compensate the costs. This point can easily be calculated by dividing the fixed expenses by the unit contribution margin Contribution margin: A porpotion of unit price that goes into fixed expenses and is calculated by deducting the variable expense per unit from the revenue per unit. Inflation Accounting A system of accounting that tries to allow for the effects of enflation. Syf 226dan devamına bak