A Review of the Accounting Cycle

advertisement

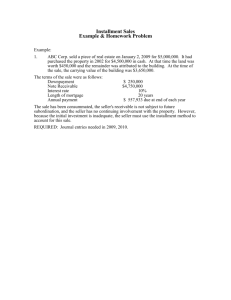

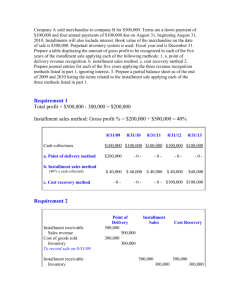

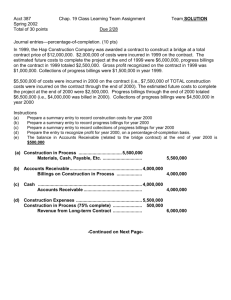

chapter 8 Revenue Recognition 1 2 Learning Objectives 1. Identify the primary criteria for revenue recognition. 2. Apply the revenue recognition concepts underlying the examples used in SAB 101. 3. Record journal entries for long-term construction-type contracts using percentage-of-completion and completedcontract methods. Continued 3 Learning Objectives 4. Record journal entries for long-term service contracts using the proportional performance method. 5. Explain when revenue is recognized after delivery of goods or services through installment sales, cost recovery, and cash methods. 4 Revenue Recognition FASB’s two criteria for recognizing revenues and gains: 1. They are realized or realizable. 2. They have been earned through substantial completion of the activities involved in the earnings process. 5 Revenue Recognition Revenue recognition most Both of these criteria often occurs when goods generally are met at the are delivered or when point of sale. services are rendered. 6 Revenue Recognition Criterion Associated With Revenue Recognition Criterion 1: The customer has provided payment or a valid promise of payment. Criterion 2: The company has provided a product or service. 7 Revenue Recognition Criterion 1 Criterion 2 Before the point of Sale EXCEPTION: Revenue can be recognized prior to the point of sale if: Customer provides a valid promise of payment AND conditions exist that contractually guarantee subsequent sale. 8 Revenue Recognition Criterion 1 Criterion 2 Point of Sale NORMALLY: Revenue is generally recognized at this point of time. Criterion 1 is typically satisfied at this point. Critical 2 is typically satisfied at this point. 9 Revenue Recognition After the Point of Sale EXCEPTION: The recognition of revenue must be deferred if: Criterion 1 Criterion 2 Customer does not provide a valid promise at time of receipt of product or service OR significant effort remains on the contract. 10 Revenue Recognition Generally, revenue is not recognized prior to the point of sale because either: • A product or service was provided without receiving a valid promise of payment from customer. • The company has not provided the product or service. An exception occurs when the customer provides a valid promise of payment and conditions exist that contractually guarantee the sale. 11 Revenue Recognition AICPA Statement of Position 97-2 gives companies more guidance through a checklist of four factors that amplify the two criteria: a. Persuasive evidence of an arrangement exists. b. Delivery has occurred. Earned c. The vendor’s fee is fixed or determinable. d. Collectibility is probable. Realised Persuasive Evidence of an Arrangement The SEC issued SAB 101 in response to specific abuses involving revenue recognition. 12 Persuasive Evidence of an Arrangement SAB 101 is in a questionand-answer format. The answers given are invariably “No.” 13 Persuasive Evidence of an Arrangement Typical questions from SAB 101 Question 1: Company May Company A requires A recognize each sale to be supported revenue in thebycurrent a written quarter salesif agreement the productsigned is delivered by an by the authorized end of the quarter representative but the sales of both Company agreement is not Asigned and theby the ENTER customer. until customer a few days after the end of the quarter? Addresses internal controls. 14 Persuasive Evidence of an Arrangement Typical questions from SAB 101 Question 2: Company Z delivers product to a customer on a consignment basis. May Company Z recognize revenue upon delivery of the product to the customer? Addresses the issue of circumventing internal controls by side agreements. 15 Delivery has occurred or service has been rendered Typical questions from SAB 101 Question 3: May Company A recognize revenue when it completes production of inventory for a customer if it segregates that inventory from other products in its warehouse? 16 Delivery has occurred or service has been rendered Typical questions from SAB 101 Question 4: Company merchandise R isaside a retailer until the that offers “layaway” customer pays thesales remainder to of customers. the sales price, A customer and takespays a portion of the possession of the sales merchandise. price, and Company When should R sets Company the… ENTER R recognize revenue? Focuses on issues centered on the “bill-and-hold” arrangements. 17 Delivery has occurred or service has been rendered “bill-and-hold” arrangements. In general, revenue should not be recognised in a bill-and-hold arrangement until the seller has transferred both legal ownership, evidence by the buyer taking title to the goods, and economic ownership, meaning that the buyer accepts responsibility for the safeguarding and preservation of the goods. 18 Delivery has occurred or service has been rendered Appropriate Layaway Accounting Receipt of $100 cash as initial layaway payment: Cash Deposit Received from Customers 100 100 Receipt of final $1,400 cash payment and delivery of goods to customer: Cash 1,400 Deposit Received from Customers 100 Sales 1,500 Cost of Goods Sold 1,000 Inventory 1,000 19 Delivery has occurred or service has been rendered 20 Delivery has occurred or service has been rendered Questions 5 & 6 – Deal with the seller receiving some up-front fee as well as subsequent periodic payments E.g. Seller Company receives $1,000 cash from a customer as the initial sign-up fee for a service. In addition to the sign-up fee, the customer is required to pay $50 per month for 100 months—which is the economic life of this service agreement. 21 Delivery has occurred or service has been rendered Receipt of $1,000 cash as initial sign-up fee: Cash 1,000 Unearned Initial Sign-Up Fees 1,000 Receipt of first monthly payment of $50: Cash 50 Monthly Service Revenue 50 Partial recognition of the initial signup fee as revenue ($1,000/100 months): Unearned Initial Sign-Up Fees 10 Initial Sign-Up Fee Revenue 10 22 Delivery has occurred or service has been rendered Questions 7 & 9 – Deal with refundable fees. In summary, the non-refundable portion of the fees can be recognized on a monthly basis if the number of refunds can be reliably estimated. 23 24 Price is fixed or determinable Typical questions from SAB 101 Question 8: Company Should Company A owns A a building estimate and leases it torevenue recognize a retailer. associated The annual leasethe with payment 1% ofissales $1.2over million $25 plus 1% of all million onthe a straight-line retailer’s sales basis in excess of $25 throughout themillion. year? ENTER Addresses the difference between estimating the future impact of past events and estimating the future impact of future events. 25 Reporting Revenue: Gross vs. Net • Gross = Sales + commission • Net = Commission only SAB 101 – Gross is inappropriate unless the seller actually took legal and economic ownership of the goods being sold. Revenue Recognition Prior to Providing Goods or Services • Completed-contract method recognizes all income when project is completed. • Percentage-of-completion method recognizes revenue throughout the term of the contract. (construction) • Proportional performance method reflects revenue earned on service contracts under which many acts of service are to be performed before the contract is complete. 26 Revenue Recognition Prior to Providing Goods or Services GAAP requires percentage-ofcompletion method unless certain criteria are not met. 27 Percentage-ofCompletion Accounting Dependable estimates of: • contract revenues • contract costs • progress toward completion Contract clearly specifies: • enforceable rights of the parties • consideration to be exchanged • manner and terms of settlement Continued 28 Percentage-ofCompletion Accounting The buyer can be expected to satisfy obligations under the contract. Contractor can be expected to perform the contractual obligation. 29 Percentage-ofCompletion Accounting Recognize revenue throughout life of the contract. Revenue recognized is a function of how complete the project is to date. Costs are charged to an inventory account: Construction in Process (CIP). Profits are charged to CIP. CIP is valued at net realizable value. Any anticipated loss is booked for the full amount of the loss when it becomes measurable. 30 Percentage-ofCompletion Accounting Input measures: Cost-to-cost method where the degree of completion is determined by comparing costs already incurred with the most recent estimates of total expected costs to complete the project. Engineers are often called in to help provide estimates. 31 Accounting for Long-Term Construction-Type Contracts Strong Construction Company was awarded a contract with a total price of $3,000,000. Strong expected to earn $400,000 profit on the contract. 32 Accounting for Long-Term Construction-Type Contracts Year Actual Cost Incurred Estimated Cost to Complete 2004 $1,040,000 2005 910,000 Total $1,950,000 650,000 2,600,000 75 2006 650,000 0 2,600,000 100 Total $2,600,000 Total Cost $1,560,000 $2,600,000 Cost Percentage 40 33 Percentage-ofCompletion Accounting 34 2004 Construction in Progress 1,040,000 Materials, Cash, etc. 1,040,000 To record costs incurred. Accounts Receivable 1,000,000 Progress Billings on Construction Contracts 1,000,000 To record billings. Cash 800,000 Accounts Receivable 800,000 To record cash collections. Percentage-ofCompletion Accounting 35 2004 Cost of Long-Term Construction Contracts 1,040,000 Construction in Progress 160,000 Revenue from Construction Contracts Actual Cost 1,200,000 $3,000,000 x .40 Percentage-ofCompletion Accounting 36 2005 Construction in Progress Materials, Cash, etc. To record costs incurred. Accounts Receivable Progress Billings on Construction Contracts To record billings. Cash Accounts Receivable To record cash collections. 910,000 910,000 900,000 900,000 850,000 850,000 Percentage-ofCompletion Accounting 37 2005 Cost of Long-Term Construction Contracts Construction in Progress Revenue from Long-Term Construction Contracts 910,000 140,000 1,050,000 ($3,000,000 x .75) – $1,200,000 Percentage-ofCompletion Accounting 38 2006 Construction in Progress 650,000 Materials, Cash, etc. 650,000 To record costs incurred. Accounts Receivable 1,100,000 Progress Billings on Construction Contracts 1,100,000 To record billings. Cash 1,350,000 Accounts Receivable 1,350,000 To record cash collections. Percentage-ofCompletion Accounting 39 2006 Cost of Long-Term Construction Contracts Construction in Progress Revenue from Long-Term Construction Contracts 650,000 100,000 750,000 $ 3,000,000 (1,200,000) (1,050,000) $ 750,000 Percentage-ofCompletion Accounting 40 2006 Construction in Progress 1,040,000 160,000 910,000 140,000 650,000 100,000 3,000,000 Progress Billings on Construction Contracts 1,000,000 900,000 1,100,000 3,000,000 Progress Billings on Construction Contracts 3,000,000 Construction in Progress 3,000,000 41 Revision of Estimates Instead of the previous illustration, assume that at the end of 2005, it was estimated that the remaining cost to complete construction was $720,000 rather than $650,000. 42 Revision of Estimates Year Actual Cost Incurred Estimated Cost to Complete 2004 $1,040,000 2005 910,000 Total $1,950,000 720,000 2,670,000 73 2006 700,000 0 2,650,000 100 Total $2,650,000 Total Cost $1,560,000 $2,600,000 Cost Percentage 40 Note that expected Items gross in blue profit changed was $400,000 from in 2004, $330,000 in 2005,the andprevious the actual illustration. was $350,000 in 2006. 43 Revision of Estimates The entries for 2004 would be the same as those shown in the previous example. 2004 44 Revision of Estimates All entries for 2005 would be the same except for the entry to record revenue and cost. 2005 45 Revision of Estimates 2005 Cost of Long-Term Construction Contracts Construction in Progress Revenue from Long-term Construction Contracts 910,000 80,000 990,000 ($3,000,000 x .73) – $1,200,000 46 Revision of Estimates 2006 Construction in Progress 700,000 Materials, Cash, etc. 700,000 To record costs incurred. Accounts Receivable 1,100,000 Progress Billings on Same Construction Contracts 1,100,000 To record billings. Cash 1,350,000 Accounts Receivable 1,350,000 To record cash collections. Same 47 Revision of Estimates 2006 Cost of Long-Term Construction Contracts Construction in Progress Revenue from Long-Term Construction Contracts 700,000 110,000 810,000 $3,000,000 (1,200,000) (990,000) $ 810,000 48 Revision of Estimates 2006 Construction in Progress 1,040,000 160,000 910,000 80,000 700,000 110,000 3,000,000 Progress Billings on Construction Contracts 1,000,000 900,000 1,100,000 3,000,000 Progress Billings on Construction Items in red are different for Contracts 3,000,000 this illustration. Construction in Progress 3,000,000 Anticipated Loss: Percentage-ofCompletion Method Assume the same facts for Strong Construction Company, except that after 2004 entries have been made, the firm determines that the total cost will be $3,250,000. The entries for 2004 would be the same, but the loss must be dealt with in 2005—in addition, the $160,000 gross profit recognized in 2004 must be eliminated. 49 Anticipated Loss: Percentage-ofCompletion Method 50 2005 Cost of Long-Term Construction Contracts Revenue from Long-Term Construction Contracts Construction in Progress 910,000 600,000 410,000 To go from a $160,000 gross profit to an anticipated $250,000 loss ($3,000,000 – $3,250,000), the Construction in Progess account needs to be credited $410,000. Accounting for Long-Term Service Contracts Most service contracts involve three types of costs: (1) Initial direct costs related to obtaining and performing initial services on the contract. (2) Direct costs related to performing the various acts of service. (3) Indirect costs related to maintaining the organization to service the contract. 51 Accounting for Long-Term Service Contracts Proportional Performance Method A correspondence school enters into 100 contracts with students for an extended writing course. The fee for each contract is $500, payable in advance. The initial direct costs related to the contracts total $5,000. Actual direct costs for lessons for the first period are $12,000. The sales value of the lessons completed is $24,000 (The total value of all lessons is $60,000). 52 Accounting for Long-Term Service Contracts Receipt of fees: Cash 50,000 Deferred Course Revenue 50,000 Initial direct costs: Deferred Liability Initial Costs 5,000 account Asset account Cash 5,000 Direct costs for lesson actually completed: Contract Costs Expense account 12,000 Cash 12,000 Continued 53 Accounting for Long-Term Service Contracts Course revenue recognized: Deferred Course Revenue 20,000 Recognized Course Revenue 20,000 Recognize contract costs from initial direct costs: $24,000 x $50,000 Contract Costs 2,000 $60,000 Deferred Initial costs 2,000 $24,000 x $5,000 $60,000 54 Revenue Recognition After Delivery 55 of Goods or Providing Service Installment Sales Method: Recognizes revenues and related expenses as cash is received (used when collection is somewhat uncertain). (Not to be confused with installment sales, which utilize accrual accounting) Cost Recovery Method: No income is recognized on sale until the cost of the item sold is recovered through cash receipts (used when collection is very uncertain). Cash Method: Recognizes all expenses immediately as incurred and all revenues only when cash is collected. Revenue Recognition After Delivery 56 of Goods or Providing Service Method Timing of Revenue Recognition Full Accrual At point of sale Installment Sales At collection of cash (portion of receipt) Cost Recovery At collection of cash (after all costs have been recovered) Cash At collection of cash Treatment of Costs Recognized at point of sale Defer and match against revenue as cash is collected Defer and match against cash receipts Charge to expense as incurred 57 Installment Sales Method The installment sales method is used most commonly in cases of real estate sales. 58 Installment Sales Method George sells merchandise on the installment basis. Uncertainty of collection makes use of the installment method necessary. Use the accompanying data to prepare George’s journal entries. 59 Installment Sales Method Sales Cost of Sales Gross Profit Gross Profit Percentage Cash Collection 2004 Sales 2005 Sales 2004 2005 $150,000 100,000 $ 50,000 $200,000 140,000 $ 60,000 33.33% 30% $ 30,000 $ 75,000 $ 70,000 60 Installment Sales Method 2004 Installment Accounts Receivable— 2004 150,000 Installment Sales 150,000 Cost of Installment Sales Inventory Cash 100,000 100,000 30,000 Installment Accounts Receivable—2004 Continued 30,000 61 Installment Sales Method 2004 Installment Sales Cost of Installment Sales Deferred Gross Profit—2004 Deferred Gross Profit—2004 Realized Gross Profit on Installment Sales 150,000 100,000 50,000 10,000 10,000 $30,000 x 33.33% Continued 62 Installment Sales Method 2005 Installment Accounts Receivable— 2005 200,000 Installment Sales 200,000 Cost of Installment Sales Inventory 140,000 Cash 145,000 Installment A/R—2004 Installment A/R—2005 Continued 140,000 75,000 70,000 63 Installment Sales Method 2005 Installment Sales Cost of Installment Sales Deferred Gross Profit—2005 200,000 140,000 60,000 Deferred Gross Profit—2004 25,000 Deferred Gross Profit—2005 21,000 Realized Gross Profit on $75,000 x 33.33% Installment Sales 46,000 $70,000 x 30% 64 Cost Recovery Method Revenue Recovered Cost Cost Assume George has to use the cost recovery method, but all sales and collections remain the same. 65 Cost Recovery Method 2005 All entries are the same except do not book the entry to gross profit. Deferred Gross Profit—2004 Realized Gross Profit on Installment Sales 5,000 5,000 66 Cost Recovery Method 2006 Deferred Gross Profit—2004 Deferred Gross Profit—2005 Realized Gross Profit on Installment Sales 30,000 10,000 40,000 67 Cash Method If the probability of recovering product or service costs is remote the cost recovery method of accounting can be used. There has to be considerable uncertainty as to ultimate collection of the contract price. chapter 8 The End 68 69