Part 1

advertisement

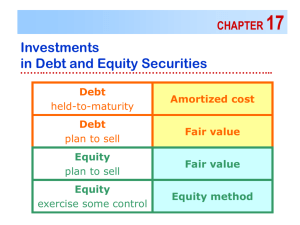

chapter 14 Investment in Debt and Equity Securities 1 Learning Objectives 1. Determine why companies invest in other companies. 2. Understand the varying classifications associated with securities. 3. Account for the purchase of debt and equity securities. 4. Account for the recognition of revenue from investments. Continued 2 Learning Objectives 5. Account for the change in value of securities. 6. Account for the sale of investment securities. 7. Record the transfer of securities between categories. 8. Explain the proper classification and disclosure of investments in securities Continued 3 Time Line of Business Issues Involved with Investment Securities 1. DETERMINE purpose of investment 2. CLASSIFY investments 3. PURCHASE securities 4. EARN AND RECOGNIZE a return 5. MONITOR changes in value 6. SELL securities 7. TRANSFER securities between categories 8. DISCLOSE status of portfolio at the end of the period 4 Why Companies Invest in Other Companies •Safety Cushion •Cyclical Cash Needs •Investment for a Return •Investment for Influence •Purchase for Control 5 Investment in Debt and Equity Securities—2001 Company Berkshire Hathaway Microsoft Coca-Cola Citigroup AT&T Verizon Total Investment (in billions) $69.0 17.7 5.4 160.8 24.5 10.2 Percentage of Total Assets 42.4% 34.7 24.2 15.3 14.8 6.0 6 Classification of Investment in Securities Debt securities typically have the following characteristics: 1. A maturity value, representing the amount to be repaid to the debt holder at maturity. 2. An interest rate that specifies the periodic interest payments. 3. A maturity date, indicating when the debt obligation will be redeemed. 7 Classification of Investment in Securities Equity securities represent ownership in a company. These shares of stock typically carry with them the right to collect dividends and vote on corporate matters. Equity securities have the potential for significant increases in price. 8 Classification of Investment in Securities Debt/Equity Securities Held-toMaturity Securities purchased with the intent to hold until maturity. Trading Securities purchased for sale in the near future. Availablefor-sale Securities not classified as trading or held-to-maturity. 9 Classification of Investment in Securities Debt Held-tomaturity Availablefor-sale Cost Method Equity Trading Equity Method 10 Equity Method Securities These are securities purchased with the intent to control or At least 20 percent of the significantly influence the outstanding voting stock operations of the investee. must be owned to have this significant influence or control. Even then, there may be evidence to support the fact that even a 20 percent investment does not have significant influence. 11 Different Accounting Treatments Classification of Securities Held to maturity Available for sale Trading Equity method Types of Securities Disclosure on the Balance Sheet 12 Treatment of Temporary Changes in Value Debt Amortized cost Not recognized Debt/equity Fair market value Reported in stockholders’ equity Debt/equity Fair market value Reported on the income statement Equity Historical cost Not recognized adjusted for changes in the assets of the investee Purchases of Debt Securities On May 1, Douglas Company purchases $100,000 in U.S. Treasury notes at 104¼, including brokerage fees. Interest is 9% payable semiannually on January 1 and July 1. The debt securities are classified by the purchaser as trading securities. Accrued interest on May 1 is $3,000, calculated as follows: $100,000 x .09 x 4/12 = $3,000 13 Purchases of Debt Securities Asset Approach Always includes brokerage fees Purchase date: May 1 Investment in Trading Securities 104,250 Interest Receivable 3,000 Cash 107,250 Continued 14 Purchases of Debt Securities Revenue Approach Purchase date: May 1 Investment in Trading Securities 104,250 Interest Revenue 3,000 Cash 107,250 Continued 15 Purchases of Debt Securities Receipt of semiannual payment: Asset Approach July 1 Cash 4,500 Interest Receivable Interest Revenue 3,000 1,500 Revenue Approach July 1 Cash Interest Revenue 4,500 4,500 16 Purchase of Equity Securities Available for Sale (AFS)/Trading Purchased 1,000 shares of AB Company’s common shares at $2 per share. Investment in Available-for-Sale*/Trading Securities - AB Company 2,000 Cash 2,000 * - would be so classified if management has no intention of holding them for a long period of time and will sell them as soon as it is economically advantageous 17 Purchase of Equity Securities – Equity Method Citty Co. purchased 100,000 shares of AB Company common shares at $2 per share. Assume that the 100,000 shares purchased represents 20 % of the outstanding voting stock of AB Company. This investment gives the investor significant influence over AB Company. 18 Purchase of Equity Securities - – Equity Method Purchased 100,000 shares of Dave’s Deli common shares at $2 per share. Equity Method Securities Investment in AB Company Stock 200,000 Cash 200,000 19 Recognizing Revenue from Debt Securities On January 1, 2004, Silmaril Technologies purchased 5-year, 10% bonds with a face value of $100,000 and interest payable semiannually on January 1 and July 1. The market rate on bonds of similar quality and maturity is 8%. 20 PV/Price of Debt Securities Present value of principal: FV = $100,000; N = 10; I = 4% Present value of interest payments: $ 67,556 PMT = $5,000; N = 10; I = 4% Total present value of the bonds 40,554 $108,110 Investment in Trading Securities Cash OR 108,100 108,100 Investment in Held-to-Maturity Securities 108,100 Cash 108,100 21 Interest Revenue for Debt Securities (Trading) When the first interest payment is received from Silmaril, the following entry would be made: July 1 Cash Interest Revenue 5,000 5,000 22 Interest Revenue for Debt Securities (Held-to-Maturity) When the first interest payment is received from Silmaril, the following entry would be made: July 1 Cash 5,000 Interest Revenue 4,324 Investment in Held-toMaturity Securities 676 23 Recognizing Revenue for Equity Securities depends on the Appropriate Accounting Method Account for as trading or available-for-sale Equity method and consolidation Equity procedures Ownership method Percentage No significant influence 0% 20% Significant influence Control 50% 100% 24 Determining the Appropriate Accounting Method Ownership Interest More than 50% 20% to 50% Less than 20% Control or Degree of Influence Control Accounting Method Equity method and consolidation procedures Significant Equity method influence No Account for as significant trading or influence available for sale 25 Applicable Standard APB Opinion #18 FASB Exposure Draft APB Opinion #18 FASB Statement No. 115 Revenue for Equity Securities Classified as Trading and AFS AB Company announces dividends of $0.25 per share. Assume that Citty Co. owns 10,000 of AB’s 200,000 shares (which represents 5%) Cash 2,500 Dividend Revenue 2,500 26 Revenue for Equity Securities Classified as Equity Method Securities AB Company announces dividends of $0.25 per share. Assume that Citty Co. owns 100,000 which represents 50 % of the outstanding voting stock. Cash 25,000 Investment in AB Company Stock 25,000 27 Revenue for Equity Securities Classified as Equity Method Securities AB Company reports an income of $250,000 for the year. Again, assume that Citty Co. owns 50 % of the outstanding voting stock. Investment in AB Company Stock 125,000 Income from Investment in AB Company Stock 125,000 28 Accounting for Temporary Changes in Value of Securities (an extract of slide 12) Classification of Security Disclosed at Report FMV Change On Trading Fair market value Income statement Availablefor-sale Fair market value Stockholder’s equity Held-tomaturity Amortized cost Not recognized 29 Accounting for Temporary Changes in Value of Securities 30 Eastwood Inc. bought the following securities on March 23, 2005. Security Classification Cost($) FMV 31/12/05($) 1 Trading 8,000 7,000 2 Trading 3,000 3,500 3 Available for Sale 5,000 6,100 4 Available for Sale 12,000 11,500 5 Held to Maturity 20,000 19,000 Accounting for Temporary Changes in Value of Securities Initial Purchase Entry Investment in Trading Securities Investment in Available-for-Sale Securities Investment in Held-to-Maturity Securities Cash Continued 11,000 17,000 20,000 48,000 31 Accounting for Temporary Changes in Value of Securities 32 By the end of the year, the value of the trading securities decreased from $11,000 to $10,500. A contra account to the “investment account” December 31, 2005: Unrealized Loss on Trading Securities Market Adjustment—Trading Securities 500 500 Included in net income Accounting for Temporary Changes in Value of Securities 33 By the end of the year, the value of the available-for-sale securities increased from $17,000 to $17,600. Included in stock holder’s equity => Comprehensive income December 31, 2005: Market Adjustment—Available-for-Sale Securities Unrealized Increase/Decrease in Value of Available-for-Sale Securities 600 600 Accounting for Temporary Changes in Value of Securities Partial Balance Sheet for Eastwood Inc. Assets Invest. in trading securities $11,000 Market adjustment—trading sec. (500) $10,500 Invest. in available-for-sale sec. $17,000 Market adjustment 600 17,600 Invest. in held-to-maturity sec. 20,000 $48,100 Stockholders’ Equity Add unrealized increase in available-for-sale securities $ 600 34 Accounting for Temporary Changes in Value of Securities Partial Income Statement for Eastwood Inc. Other expenses and losses: Unrealized loss on trading securities $500 35