File - Marie Hoffman

advertisement

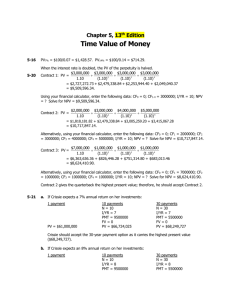

Group 1: Armijo, Hairston, Pitrone 1 Practical Exercise 2 Learning Objectives Introduction: Concept of Value History Features Theories Measures Significance Time Value of Money Basics Opportunity Cost Present vs Future Value Use in Capital Budgeting 3 Concept of Value History • Historically, based on an underlying commodity, such as gold, and the price of gold regulated the value of money, keeping it stable. • Today, the Federal Reserve regulates interest rates and it is this power that underlies the value of money. 4 Concept of Value • • • • Features The price of money is based on its purchasing power. This may or may not have anything to do with the actual prime rate, which is based on the whim of the banks. Rationally, the value of money, independent of the Fed, is based on yesterday's purchasing power. Therefore, money is based on "pre-existing prices." Since money is based on what it can buy, a preexisting price must exist for money to have value. 5 Concept of Value Measures • M1 : the amount of cash available in bank deposits. • M2 : (M1) + all savings deposits of any kind, as well as all available liquid money in money markets. • M3 : (M1 + M2) + all forms of certificates and large liquid cash investments in dollars worldwide) broadest conception, • M1 + M2 +M3 estimate of how much readily available cash exists and thus gives a rough idea of the dollar's value. 6 Concept of Value Significance • Since money is based on what it can buy, a preexisting price must exist for money to have value. The real significance here is that the value of money dictates how much your savings, earnings and debt is worth. If the value of money is low, then your salary is low, but your debts are equally low. 7 Time Value of Money Money, like all things, exists in time. Most people understand that over time, the value of $1 can change. If you can invest your dollar, even at a very low rate, it will be worth more in the future than it is now because it will earn interest. This change is known as the time value of money and is an important concept to understand as you make financial goals and plans 8 Time Value of Money Basics The time value of money is an economic concept that accounts for the difference in value certain sum of money has based on the time involved in gaining or losing it. In essence, the time value of money is a way of acknowledging the difference between being paid today and being paid at some future time, requiring a wait. For most people, waiting for money is much less desirable than having it immediately. This is because waiting involves the potential for an opportunity cost. 9 Time Value of Money Opportunity Cost An opportunity cost is a loss that results from a missed opportunity. Opportunity cost is conceptually related to the time value of money. If a person receives money sooner rather than later, they can invest or spend it and enjoy the money’s value. If they must wait, however, the money is of less value to them because they will miss out on any opportunities between the present and the time they receive the money. By determining the value of this opportunity cost, it is possible to compare the difference in the value of money lost due to waiting. Capital budgeting decisions necessarily involve the choice of one opportunity cost over another. 10 Time Value of Money Present Vs. Future Value The time value of money is usually expressed as the difference between the present value of a sum of money and that same sum’s future value. The present value is usually the outright value of the money, if paid immediately, while the future value is the amount of money plus interest. This is because receiving the same amount money in the future means the loss of an opportunity to earn interest. 11 Time Value of Money Use in Capital Budgeting Present and future values of money are critical to capital budgeting. Budgeting requires decisions to allocate or invest money. By opting to place money into an investment, an individual or a business will be denying themselves the use of that money until the investment pays off. If the investment’s value at maturity exceeds the calculated future value of the investment’s principal, this could be an excellent choice. But if the future value of the money exceeds the value of the investment, it might be better to choose another investment or keep the money in cash. As a concept, time value of money provides a means to analyze the opportunity costs of capital budgeting decisions. Using the time value of money allows these decisions to take place with a better understanding of whether or not a particular choice in allocating money is better or worse than other available choices. 12 Video Easy Quiz 13 Time Value of Money Pre-Test 1. Diane invests $500 today in an account earning 7%. How much will it be worth in 5 years? _____ 10 years? _____ 20 years? _____ 2. Same facts as #1, except Diane finds an account earning 10%. How much will it be worth in 5 years? _____ 10 years? _____20 years? _____ 3. Elaine needs to save up $4,000 in 4 years. If she can set aside $1,000 today, what rate of return does she need on her account? _____ 4. Same facts as in #3, except now Elaine can set aside $50 per month. What rate of return does she need on her account? _____ 5. Frank wants to buy a $10,000 car. The car dealer offers him financing of 60 payments at 9% interest. What will his payments be? _____ 6. Same facts as #5, except the dealer also offers 48 payments at 8%. Now what will Frank’s payments be? _____ 7. Gayle has a credit card with a $500 balance on it and a 19% interest rate. He wants to pay off his card in two years. What will his monthly payments be? _____ How much interest will he pay? _____ 14 Time Value of Money Pre-Test Diane invests $500 today in an account earning 7%. How much will it be worth in 5 years? $701 10 years? $984 20 years? $1,935 2. Same facts as #1, except Diane finds an account earning 10%. How much will it be worth in 5 years? $805 10 years? $1,297 20 years? $3,364 3. Elaine needs to save up $4,000 in 4 years. If she can set aside $1,000 today, what rate of return does she need on her account? 41% 4. Same facts as in #3, except now Elaine can set aside $50 per month. What rate of return does she need on her account? 24% 5. Frank wants to buy a $10,000 car. The car dealer offers him financing of 60 payments at 9% interest. What will his payments be? $208 6. Same facts as #5, except the dealer also offers 48 payments at 8%. Now what will Frank’s payments be? $244 7. Gayle has a credit card with a $500 balance on it and a 19% interest rate. If he wants to pay off his card in two years, what will his monthly payments be? $25.20 How much interest will he pay? $104.80 ($25.20 x 24 = $604.80, less the $500 original balance = $104.80) 15 Where to Start: The Timeline A timeline is a linear representation of the timing of potential cash flows. Drawing a timeline of the cash flows will help you visualize the financial problem. As simplistic as it sounds…it’ll keep you out of trouble down the road. 16 The Time Line Basics 0 1 2 3 CF1 CF2 CF3 I% CF0 • Tick marks designate ends of periods. • Time 0 is the starting point (the beginning of Period 1); Time 1 is the end of Period 1 (the beginning of Period 2); and so on. • Inflows are positive cash flows. • Outflows are negative cash flows identified via a “-” (minus) sign. 17 Three Rules of Time Travel Financial decisions often require combining cash flows or comparing values. Three rules govern these processes. The Three Rules of Time Travel 18 The 1st Rule of Time Travel A dollar today and a dollar in one year are not equivalent. Why? Thus, it is only possible to compare or combine values at the same point in time. Example: Which would you prefer: A gift of $1,000 today or $1,210 at a later date? To answer this, you will have to compare the alternatives to decide which is worth more. What factors do we need to consider? 19 The 2nd Rule of Time Travel To move a cash flow forward in time, you must compound it. Suppose you have a choice between receiving $1,000 today or $1,210 in two years. You believe you can earn 10% on the $1,000 today, but want to know what the $1,000 will be worth in two years. The time line looks like this: We would technically be indifferent! 20 The 2nd Rule of Time Travel Future Value of a Cash Flow FVn C (1 r ) (1 r ) (1 r ) C (1 r ) n n times 21 The Composition of Interest Over Time 22 Example Problem: Suppose you have a choice between receiving $5,000 today or $10,000 in five years. Which is the better deal (all things equal)? You believe you can earn 10% on the $5,000 today, but want to know what the $5,000 will be worth in five years. 23 Solution Solution: The time line looks like this: 1 0 $5,000 x 1.10 $5, 500 2 x 1.10 $6,050 3 x 1.10 $6,655 4 x 1.10 $7,321 5 x 1.10 $8,053 Thus in five years, the $5,000 is expected to grow to: $5,000 × (1.10)5 = $8,053, so we say the future value of $5,000 at 10% for five years is $8,053. Decision: You would be better off forgoing the gift of $5,000 today and taking the $10,000 in five years. What might alter this decision? 24 The 3rd Rule of Time Travel To move a cash flow backward in time, we must discount it. Present Value of a Cash Flow: PV C (1 r ) n C (1 r )n 25 Example Problem: Suppose you are offered an investment that pays $10,000 in five years. If you expect to earn a 10% return, what is the value of this investment today? 26 Solution Solution: The $10,000 is worth: $10,000 ÷ (1.10)5 = $6,209 27 Applying the Rules of Time Travel The Three Rules of Time Travel 28 Valuing a Stream of Cash Flows Based on the first rule of time travel we can derive a general formula for valuing a stream of cash flows: if we want to find the present value of a stream of cash flows, we simply add up the present values of each. 29 Valuing a Stream of Cash Flows Present Value of a Cash Flow Stream PV N PV (C ) n 0 n N n 0 Cn (1 r ) n 30 Future Value of Cash Flow Stream Future Value of a Cash Flow Stream with a Present Value of PV FVn PV (1 r ) n 31 The Easy Way 32 Three Methods to Work TVM Problems Solve the FV equation using a regular calculator. Use a financial calculator — that is, one with financial functions. Use a computer with a spreadsheet program such as Microsoft Excel®. 33 Regular Calculator Solution 0 1 2 3 10% -$100 $110.00 $121.00 $133.10 $100 x 1.10 x 1.10 x 1.10 = $133.10 34 Spreadsheet Solution 35 What is the PV of $100 due in three years if I = 10%? Solve FVN = PV x (1 + I )N for PV PV = FVN / (1 + I )N PV = $100 / (1.10)3 = $100(0.7513) = $75.13 If I offer you $75.13 today or $100 three years from now, which would you prefer? Spreadsheet Solution 36 Solving for I Assume that a bank offers an account that will pay $200 after five years on each $75 invested. What is the implied interest rate? Spreadsheet Solutions 37 Solving for N Assume an investment earns 20 percent per year. How long will it take for the investment to double? Spreadsheet Solutions 38 Annuities 39 Types of Annuities Three Year Ordinary Annuity 0 I% 1 2 3 PMT PMT PMT Three Year Annuity Due 0 1 2 PMT PMT 3 I% PMT 40 What is the FV of a three-year ordinary annuity of $100 invested at 10%? 0 1 2 $100 $100 3 10% $100 110 121 FV = $331 41 Spreadsheet Solutions 42 What is the PV of the annuity? 0 1 2 3 $100 $100 $100 10% $90.91 82.65 75.13 $248.69 = PV 43 Spreadsheet Solutions 44 What is the FV and PV if the annuity were an annuity due? 0 1 2 3 10% $100 ? $100 $100 ? 45 What is the FV of the annuity due? 0 1 2 $100 $100 3 10% $100 110 121 133 FV = $364 46 What is the PV of the annuity due? 0 1 2 3 10% $100 $100.00 $90.91 82.64 $273.55 = PV $100 47 Present Value & the Decision Rule 48 PV & NPV Decision Rule The net present value (NPV) of a project or investment is the difference between the present value of its benefits and the present value of its costs. NPV PV (Benefits) PV (Costs) NPV PV (All project cash flows) 49 Calculating the Net Present Value Calculating the NPV of future cash flows allows us to evaluate an investment decision. Net Present Value compares the present value of cash inflows (benefits) to the present value of cash outflows (costs). 50 The NPV Decision Rule When making an investment decision, take the alternative with the highest NPV. Choosing this alternative is equivalent to receiving its NPV in cash today. Should this ALWAYS be true? 51 The NPV Decision Rule (cont'd) Accepting or Rejecting a Project Accept those projects with positive NPV because accepting them is equivalent to receiving their NPV in cash today. Reject those projects with negative NPV because accepting them would reduce the wealth of investors. Question: What if the project is a ‘loser’ today, but creates goodwill in the community and/or preserves NFP status? 52 Choosing Among Alternatives We can also use the NPV decision rule to choose among projects. To do so, we must compute the NPV of each alternative, and then select the one with the highest NPV. This alternative is the one which will lead to the largest increase in the value of the firm. 53 Uneven Cash Flow Streams: Setup 0 10% 1 $100 2 $300 3 4 $300 -$50 $ 90.91 247.93 225.40 -34.15 $530.09 = PV 54 Spreadsheet Solutions 55 Return on Investment (ROI) The financial performance of an investment is measured by its return on investment. Time value analysis is used to calculate investment returns. Returns can be measured either in dollar terms or in rate of return terms. Assume that a hospital is evaluating a new MRI. The project’s expected cash flows are given on the next slide. 56 MRI Investment Expected Cash Flows ($$$ in K’s) 0 1 -$1,500 $310 2 $400 3 4 $500 $750 Where do these numbers come from? 57 Simple Dollar Return 0 1 2 3 -$1,500 $310 $400 $500 310 400 500 750 $ 460 = Simple dollar return 4 $750 Is this a good measure? 58 Discounted Cash Flow (DCF) Dollar Return 0 8% 1 2 3 -$1,500 $310 $400 $500 287 343 397 551 $ 78 = net present value (NPV) 4 $750 Is this a better measure? 59 Spreadsheet Solution 60 Opportunity Cost Rate To find an investment’s dollar return (NPV), we need to apply a discount rate. The discount rate is the opportunity cost rate or the rate that could be earned on alternative investments of similar risk. Typically firms apply the WACC (more later) It does NOT depend on the source of the investment funds. 61 Opportunity Cost Rate (Cont.) When calculating NPV, the discounting process automatically recognizes the opportunity cost of capital. Thus, A positive NPV means that the investment is expected to create value for the investor. A negative NPV means that the investment is expected to lose value for the investor. 62 Rate of (Percentage) Return 0 10% 1 2 3 -$1,500 $310 $400 $500 282 331 376 511 $ 0.00 = NPV, so E(R) = 10.0% . 4 $750 63 Spreadsheet Solution 64 Rate of Return (Cont.) In capital investment analyses, the rate of return often is called internal rate of return (IRR) or the percentage return expected on the investment. To interpret the rate of return, it must be compared to the cost of capital. In this example, 10 % IRR > 8% WACC, so the project is a winner. The IRR & NPV should both indicate whether a project will produce a positive result (or not). 65 Intra-Year Compounding • Thus far, all examples have assumed annual compounding. • When compounding occurs intra-year, the following occurs: – Interest is earned on interest during the year (more frequently). – The future value of an investment is larger than under annual compounding. – The present value of an investment is smaller than under annual compounding. 66 0 1 2 3 10% -100 133.10 Annual: FV3 = 100 x (1.10)3 = 133.10 0 0 1 1 2 3 2 4 5 3 6 5% -100 134.01 Semiannual: FV6 = 100 x (1.05)6 = 134.01 67 Amortization 68 Amortization Construct an amortization schedule for a $1,000, 10% annual rate loan with three equal payments. 69 Step 1: Find the required payments 0 1 2 3 PMT PMT PMT 10% -$1,000 Step 2: Find interest charge for Year 1. Step 3: Find repayment of principal in Year 1. Step 4: Find ending balance at end of Year 1. 70 Finally: Repeat these steps for Years 2 and 3 to complete the amortization table YR 1 2 3 TOTAL BEG BAL $1,000 698 366 PMT INT $402 402 402 $1,206 $100 70 36 $206 PRIN PMT END BAL $302 $698 332 366 366 0 $1,000 Note that annual interest declines over time while the principal payment increases. 71 Questions? 72