The Measurement

Fundamentals of Financial

Accounting

Presentations for Chapter 3 by Glenn Owen

Key Points

Four basic assumptions of financial accounting.

The markets in which business entities operate and the valuation

basis used on the balance sheet.

The principle of objectivity and how it determines the dollar

values that appear on the financial statements.

The principles of matching, revenue recognition, and

consistency.

Two exceptions to the principles of financial accounting

measurement: materiality and conservatism.

Basic Assumptions

Economic entity

Fiscal period

Going concern

Stable dollar

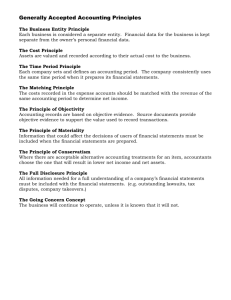

Economic Entity

A company is assumed to be a separate

economic entity that can be identified and

measured.

This concept helps determine the scope of

financial statements.

Examples — Disney and ABC, General

Electric and NBC.

Fiscal Period

It is assumed that the life of an economic

entity can be broken down into accounting

periods.

The result is a trade-off between objectivity

and timeliness.

Alternative accounting periods include the

calendar or fiscal year.

Going Concern

The life of an economic entity is assumed to

be indefinite.

Assets, defined as having future economic

benefit, require this assumption.

Stable Dollar

The value of the monetary unit used to measure an

economic entity’s performance and position is

assumed stable.

If true, the monetary unit must maintain constant

purchasing power.

Inflation, however, changes the monetary unit’s

purchasing power.

This is considered an unrealistic assumption and

thus places a limit on the financial statements as a

tool for analysis.

Valuations on the

Balance Sheet

Input market

– Purchase of materials, labor, overhead

Output market

– Sales of services or inventories

Alternative valuation bases

– Present value

– Fair market value

– Replacement cost

– Original cost

Present Value

as a Valuation Base

Discounted future cash inflows and

outflows

For example, the present value of a notes

receivable is calculated by determining the

amount and timing of its future cash inflows

and adjusting the dollar amounts for the

time value of money.

Fair Market Value

as a Valuation Base

Sales price or the value of goods and

services in the output market.

For example, accounts receivable are valued

at net realizable value which approximates

fair market value.

Replacement Cost

as a Valuation Base

Current cost or the current price paid in the

input market.

For example, inventories are valued at

original cost or replacement cost, whichever

is lower.

Original Cost as a

Valuation Base

Input price paid when originally purchased.

For example, land and property used in a

company’s operations are all valued at

original cost.

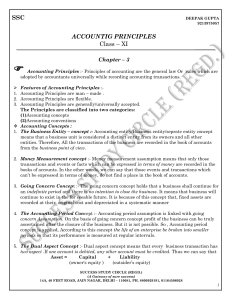

Principles of Financial

Accounting Measurement

Objectivity

Matching

Revenue recognition

Consistency

The Objectivity Principle

This principle requires that the values of

transactions and the assets and liabilities

created by them be verifiable and backed by

documentation.

For example, present value is only used

when future cash flows can be reasonably

determined.

The Revenue

Recognition Principle

This principle determines when revenues can be

recognized.

This principle triggers the matching principle,

which is necessary for determining the measure of

performance.

The most common point of revenue recognition is

when goods or services are transferred or provided

to the buyer.

Revenue Recognition

Current

Period

Decide when

revenue is to be

recognized?

Revenue

1. Significant portion of

production and effort

complete?

2. Amount of revenue

objectively measured?

3. Major portion of costs have

been incurred?

4. Collection of cash reasonably

assured?

YES

NO

Future

Period

Revenue

The Matching Principle

This principle states that the efforts of a

given period should be matched against the

benefits they generate.

For example, the cost of inventory is

capitalized as an asset on the balance sheet

and not recorded in Cost of Goods Sold

until sold.

The Matching Process

Incur cost in

current period

to generate

revenue

Current

Period

If current period,

then expense cost

in current period

Decide what

period revenue is

to be recognized?

Revenue

Future

Period

Revenue

Expense

Expense

If future period, then

capitalize cost on the

balance sheet and

expense in future periods

The Consistency Principle

Generally accepted accounting principles

allow a number of different, acceptable

methods of accounting.

This principle states that companies should

choose a set of methods and use them from

one period to the next.

For example, a change in the method of

accounting for inventory would violate the

consistency principle.

Exceptions to the

Basic Principles

Materiality

– Only transactions with amounts large enough to make a

difference are considered material.

– Nonmaterial transactions are ignored

Conservatism

– When in doubt

Understate assets

Overstate liabilities

Accelerate recognition of losses

Delay recognition of gains

COPYRIGHT

Copyright © 2003, John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written permission of the copyright owner is unlawful.

Request for further information should be addressed to the

Permissions Department, John Wiley & Sons, Inc. The purchaser

may make back-up copies for his/her own use only and not for

distribution or resale. The Publisher assumes no responsibility

for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.