Fourth Quarter 2014 Market Commentary

Doug Ramsey, CFA, CMT

Chief Investment Officer

Last year marked the sixth consecutive annual gain for the S&P 500, a feat not accomplished

since the 1990s. The character and leadership of last year’s stock market certainly fit the pattern of an

aging cyclical bull market, with Large Cap stocks in economically defensive sectors emerging as the big

winners (Consumer Staples, Health Care, and Utilities). Small Caps—which entered 2014 at a record

valuation premium in relation to Large Caps—trailed the S&P 500 by almost 10 percentage points for

the year, while foreign stocks also lagged, thanks in part to a second-half surge in the U.S. dollar.

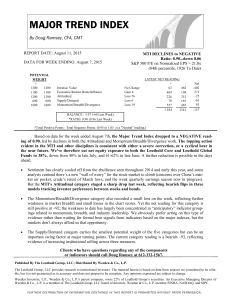

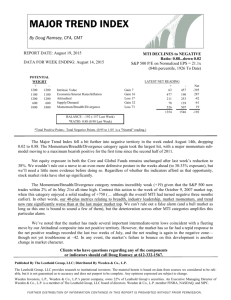

After having been bullish for most of the past six years, our Major Trend Index (MTI) and other

market tools now point to an environment of elevated risks. The MTI has spent the last three months

in “neutral” territory, prompting us to hold our tactical accounts’ net equity exposure at a below-average allocation of 50%. We suspect the next move in the MTI will be a decline into negative territory,

which would trigger an additional reduction in net equity exposure, likely to the 30-35% range. But

the bull market has surprised us before: over the past couple years, every time it’s looked a bit ragged,

it’s found a way to rejuvenate itself. Reaching a bull market top can be an extended process, and we’ll

need more decisive bearish evidence from our quantiative work before further reducing net equity

exposure in tactical accounts.

Our Intrinsic Value work suggests that U.S. equities remain moderately overvalued, with valuations on the “median” or “typical” stock more inflated than those for the capitalization-weighted

market averages. For example, the median Normalized P/E ratio on the 3000 stocks in the Leuthold

domestic stock universe is 24.9x, well above that of the cap-weighted S&P 500 (20.9x P/E ratio). Typically, the median stock trades at a small P/E discount to the S&P 500. Mid and Small Cap U.S. stocks

could therefore prove especially vulnerable during the next major market decline.

On the positive side, valuation risks for foreign stocks look considerably lower after another

year of underperformance. The MSCI World Ex-USA Index trades about four P/E points below the

U.S. (at 16.8x Normalized EPS), and Emerging Markets are even cheaper (12.1x EPS).

Our quantitative equity strategies had strong results in 2014, with our equity industry group

work locking in some of the year’s best-performing themes (including Airlines, Managed Health Care,

and several industry group winners within the Technology sector). Our analyses of valuations and capital spending trends support the potential for a multi-year phase of stock market leadership from the

Technology sector. Among our current equity industry positions are Semiconductors and the Technology Hardware & Storage group.

(Continued)

Leuthold Weeden

1

Capital Management

Fourth Quarter 2014 Market Commentary

(continued)

Our equity industry analysis in 2014 was also notable for helping us to avoid certain areas, specifically, the Energy and Materials sectors, where the inflated capital spending levels (we’ve warned of in recent years) finally culminated in a broad-based commodity price collapse in 2014’s second half. We believe

global production capacity for most commodities remains too high, but admit that valuations in some of

these groups (particularly within the Energy sector) now look appealing. We’ll be watching our industry

models closely for a buying opportunity, perhaps later this year or early 2016.

Fixed income exposure in our tactical funds remains low, at 20%, reflecting a lack of value (and

yield, for that matter) across most sectors of the global bond market. But the lack of value and lack of yield

is nothing new. We felt much the same way a year ago when the yield on the 10-year U.S. Treasury bond

hit 3%, yet to our surprise, fixed income played a valuable supporting role in our tactical portfolios during

2014 as long-term Treasury yields fell sharply. Following last year’s strong bond rally, we’ve cut the average

maturities of our fixed income holdings to about 4.5 years, and continue to focus on high quality credit.

As we begin the new year, our portfolios are positioned in areas that we believe are apt to best withstand the challenges of a late stage bull market, and we're confident that our disciplines will direct us to

make adjustments, when needed, as the year progresses.

Please feel free to contact us if you have any questions. Thank you for your support.

Sincerely,

Doug Ramsey, CFA, CMT

Chief Investment Officer

Leuthold Weeden

2

Capital Management

ageme

Other Market Notes

Sentiment: Frothier Than You Think

Last year will certainly go down

as the bull market year in which investors were finally retrained to buy the

dips (as they usually are, late in every

bull market). Most of our Attitudinal

measures—ranging from option activity and bear fund assets, to surveys of

investor sentiment—show retail investors finally shaking off the worry that

gripped them for most of the bull market’s first five years.

Certain sentiment readings have been notable not just for their levels, but their persistence. This is evidenced by Investor’s Intelligence weekly survey of market newsletter writers, where the 2014 annual “average”

level of bullish sentiment was the second-highest in the survey’s 51-year history.

It’s well known that sentiment extremes (especially optimistic ones) can

persist for long periods before an eventual mean-reversion kicks in. However, we

found that average annual readings from this survey possess (as theory would suggest) a healthy negative correlation (-0.35) with the subsequent year’s action in the

S&P 500. The correlation grows even more powerful at major sentiment extremes

(such as the current one). Table 1 shows the ten highest “average sentiment” years

since 1964; of the nine years prior to 2014, three of the years were followed by an

annual gain of just 3% or less (about flat)—and three of the years were followed

by years experiencing double digit losses. The overall average gain of all years’

results was just +0.1%; none of these high sentiment years was followed by a truly

great year for stocks.

At the other end of the spectrum are the ten years with the lowest annual

average sentiment readings. A quick scan of Table 2 shows that many of these

low confidence years are, as expected, associated with bear markets. However, the

lowest average sentiment reading occurred in 1994, a flat year for the blue-chip

averages (which of course provided the springboard for the 1995 market blast-off).

The return profile for years following these low sentiment reading years is excellent, with only a single loss (1968), and an average S&P 500 gain of +17.4%.

The Investor’s Intelligence survey used in this study is reviewed within our

Major Trend Index, along with about 30 other Attitudinal inputs on a weekly basis. But, we wonder if we should attach more weight to the persistence of a given

sentiment condition, considering that behaviors which ultimately undermine an

economic recovery and bull market (economic malinvestment, heavy issuance of

high yield debt/leveraged loans, etc.) require a sustained period of confidence to

foment. Optimists might claim we’ve just entered such a phase; our work suggests

this phase is well-advanced.

Leuthold Weeden

3

Capital Management

Table 1

Table 2

Other Market Notes

Years Ending In “Five”-- An Anomaly We Can't Explain

We’ve written periodically about the Presidential Election Cycle in relation to stock prices, sheepishly acknowledging both the persistence of the pre-election year effect and its pervasiveness across many markets. Since

1898, the DJIA has produced an average gain of 12.3% in years preceding a presidential election year, versus an

average 7.6% gain for all years. Results are even better if years prior to WWII are ignored.

A possible explanation for the pre-election phenomenon would be a ramp-up in stimulus supporting reelection efforts. But there’s no rationale for the anomaly we’ve heard mentioned frequently in recent weeks: the

bullish “Year Ending In Five” effect. Yes, such years have tended to be great ones in the stock market, with an average DJIA gain of 34.6% (though the pattern failed in 2005, with a DJIA loss of 0.6%).

33 S. 6th Street, Suite 4600

Minneapolis MN 55402

612.332.9141

info@LWCM.com

www.LWCM.com

!

"

#

ties and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. DOFU: 1.28.15

Leuthold Weeden Capital Management is the adviser to Leuthold Funds. Distributor: Rafferty Capital Markets, LLC, Garden City, NY, 11530; Copyright © 2015 by The Leuthold Group. All Rights

Reserved.

Leuthold Weeden

4

Capital Management