exchange rate forecasts

September 2014

EXCHANGE RATE

FORECASTS

DOLLAR STILL HAS ROOM TO TREND STRONGER IN 2015-

2016 AFTER 2013-2014’S LARGE GAINS

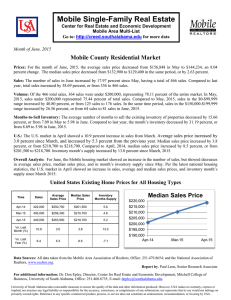

U.S. Dollar: U.S. economic growth gained momentum in spring

2014 after a weather-related slowdown in the 2013-2014 winter months: Job growth was faster in the first half of 2014 than in 2013, and various business and consumer sentiment indicators reached recovery-to-date highs at mid-year. Against this strengthening economic backdrop, the Federal Reserve continues to taper its quantitative easing program, and will likely cease net new purchases of bonds at the October 2014

Federal Open Market Committee meeting; PNC Economics forecasts that the Fed will make an initial Federal Funds rate hike in the second half of 2015. Surprisingly, in the first half of

2014, the dollar index was unaffected by the strengthening economy and evidence that U.S. interest rates will rise next year – but then shot up in the month of August as the dollar strengthened suddenly against the euro, pound, yen, peso, and

Loonie. While August’s sharp gains seem a little overdone, the dollar does seem likely to continue to trend stronger against most currencies in 2015 and 2016 as the U.S. unemployment rate falls further and U.S. interest rates rise.

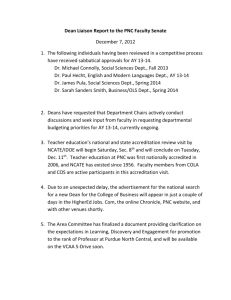

Australian Dollar: The Aussie dollar strengthened in the second quarter of 2014 on stronger Chinese activity indicators, but signs of a deepening housing correction in China mean this tailwind for the currency will likely be short-lived. Domestically, the economic outlook is little changed from earlier in 2014: moderate growth that will leave the unemployment rate elevated by historical standards, muting domestic sources of inflation and justifying the Reserve Bank of Australia’s expectations for a continuing “period of stability” in its benchmark cash rate, currently 2.5 percent. Australian monetary policy will likely stay on hold in 2015 as central banks in the U.S., U.K., and Canada begin to hike rates. As rate hikes draw nearer in the U.S. and other stronger advanced economies, the Aussie dollar will likely depreciate.

105

104

103

102

101

100

99

98

97

96

95

U.S. dollar broad index, Jan. 1997 = 100

PNC Forecast

1.15

1.10

1.05

1.00

0.95

0.90

0.85

0.80

U.S. dollars per Australian dollar

PNC Forecast

EXCHANGE RATE FORECASTS

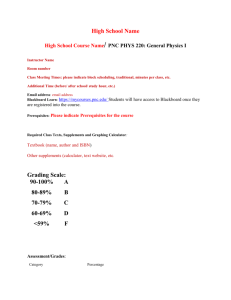

Canadian Dollar: As in the U.S., economic reports in Canada in the spring of 2014 have shown the winter slowdown to be mostly an artifact of harsh weather, rather than a sign of more fundamental economic weakness. Activity indicators, including indicators for manufacturing, energy production, and housing, improved in the second quarter from the first quarter’s weak levels, as did unemployment claims. The unemployment rate should begin to fall in the second half of 2014, and wage growth should pick up as well as slack in the Canadian labor market is absorbed. The Bank of Canada (BoC) has under Governor

Stephen Poloz made its policy stance neutral and its next move data-dependent; stronger labor market indicators should point to this move being an Overnight Rate hike, which we forecast for the third quarter of 2015. As evidence grows that a BoC rate hike is approaching, the Canadian dollar should continue to retrace some of its unjustifiedly large depreciation of late 2013 and early 2014.

1.15

1.10

1.05

1.00

0.95

0.90

0.85

Canadian dollars per U.S. dollar

PNC Forecast

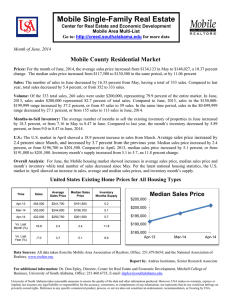

Chinese Yuan: China’s exchange rate regime continues to evolve: the yuan’s old pattern of on-again, off-again appreciation against the U.S. dollar was in 2014 replaced by its largest depreciation in 20 years. In the near term, a substantial appreciation in the final months of 2014 seems likely. Official

Chinese government communications typically describe exchange rate movements in annual, December 31 to December

31 terms and the next G20 meeting would be quite embarrassing for China’s leaders if they have to explain why the yuan closed 2014 weaker than the 6.05 at which it began the year. In addition, China’s trade surplus is widening in the second half of 2014. Exports to advanced economies are improving, and the investment which fuels demand for China’s commodity imports is weak. In 2015, trend appreciation will likely be replaced by larger short-term fluctuations of the exchange rate around a more or less stable long-term level, as the government follows through on its March 15, 2014 decision to widen the daily range in which the currency is allowed to trade.

Brazilian Real: With the World Cup in the rear mirror, it is a struggle to come up with anything nice to say about the Brazilian economy: Inflation is stubbornly stuck at the top of the central bank’s 2.5-6.5 percent target range, real GDP contracted in the first half of 2014, and business sentiment is worse in mid-2014 than at the trough of the global recession in 2009. So what could possibly explain why the real is still on the stronger side of the

2.2-2.4 per U.S. dollar range it has established since mid-2013?

Politics. Following the sudden and tragic death of Socialist Party

Presidential candidate Eduardo Campos in July, the new Socialist candidate, Marina Silva, looks to have a shot at beating Worker’s

Party incumbent Dilma Rousseff in the October 5 election.

Capital markets, fairly or otherwise blaming Rousseff for Brazil’s stagflation, have been cheered by the prospect of change. This political optimism seems a bit naïve: the Socialist Party’s politics are close to the Worker’s Party’s – dramatic pro-growth economic reforms are unlikely either way. On balance, the real seems likely to average weaker in coming quarters as optimism toward Brazilian politics yields to disappointment, and as the Fed finishes tapering and begins to raise rates.

6.5

6.4

6.3

6.2

6.1

6.0

2.6

2.4

2.2

2.0

1.8

1.6

Chinese yuan per U.S. dollar

Brazilian real per U.S. dollar

PNC Forecast

PNC Forecast

EXCHANGE RATE FORECASTS

Euro: The euro broke lower in mid-2014 after the European

Central Bank set a negative deposit rate, effectively charging commercial banks a penalty for excess reserves held at the central bank, and announced plans to extend additional longterm loans to Eurozone commercial banks through Targeted

Long Term Refinancing Operations, to be conducted quarterly beginning in September 2014. Recent economic indicators suggest that the ECB will eventually have to launch a more substantial quantitative easing program as well: Eurozone real

GDP growth was a tepid 0.6 percent annualized in the first half of 2014, and CPI inflation of 0.6 percent in year-ago terms in the first eight months of 2014 is below the ECB’s target of below but close to two percent. With unemployment high and recovery slow, monetary policy will stay highly expansionary in the Eurozone well after the Fed starts to normalize U.S. interest rates, likely leading to a weaker euro in coming quarters.

Indian Rupee: The rupee presents a dilemma for market positioning: The dollar-rupee rate moved above its 200 day moving average in August for the first time since February

2014, a technical development that preceded several multimonth rupee depreciations over the last decade. On a multiquarter time horizon, by contrast, fundamentals support a stronger currency: accelerating real GDP growth, cooling inflation, and improving business and consumer confidence.

These bi-directional risks suggest that the most likely trajectory for the rupee is slightly weaker through year-end 2014, and then stronger in 2015 and 2016.

Japanese Yen: The yen’s depreciation against the U.S. dollar resumed in August 2014 after a long pause in the first half of

2014. Some of the yen’s weakness might be explained by the depth of the economy’s contraction in the second quarter of

2014, but consensus forecasts all seemed prepared for a sharp downturn after the April 1, 2014 value added tax hike. More likely, the yen’s change in direction in August reflected market recognition that monetary policy in Japan, like in the Eurozone, was about to diverge from U.S. policy: the Bank of Japan will likely continue with its highly expansionary Quantitative and

Qualitative Easing policy through 2016, cushioning the economy through a second value added tax hike in 2016 and helping to entrench positive inflation expectations. The divergence between U.S. and Japanese monetary policy should encourage a trend depreciation in the yen, which will likely continue until the second half of 2016. If the Bank of Japan is successful in raising inflation expectations by 2016 as we forecast, the exit strategy for Japan’s QE-squared program will start being discussed around then, likely curtailing the yen’s weakening trend.

1.3

1.2

1.1

1.5

U.S. dollars per euro

1.4

PNC Forecast

72

68

64

60

56

52

48

44

40

Indian rupees per U.S. dollar

PNC Forecast

115

110

105

100

95

90

85

80

75

Japanese yen per U.S. dollar

PNC Forecast

EXCHANGE RATE FORECASTS

Korean Won: Real GDP growth was a disappointing 0.6 percent (not annualized) in the second quarter, as consumption and especially tourism spending slumped after the Sewol ferry disaster in April. In response to slowing growth (and perhaps also to its falling approval ratings), the Korean government announced a stimulus program of one percent of GDP in public spending and 2 percent in central bank-supplied credit in late

July; the Bank of Korea also chipped in with a 25 basis point cut to the benchmark Base Rate, lowering the rate to 2.25 percent on August 14. The growth outlook is still solid – consensus forecasts are for 3.5-3.8 percent real GDP growth in 2014,

2015 and 2016 – but CPI inflation, most recently 1.6 percent in year-ago terms in July 2014, is well below the Bank of Korea’s

2.5-3.5 percent target range, and held down by low import prices. The won, a riskier, high-yield currency, has broken through the historically strong level of 1,020 per U.S. dollar since June 2014, and will likely weaken in 2015 and 2016 as the Fed’s taper quenches foreign investors’ thirst for yield.

1,225

1,200

1,175

1,150

1,125

1,100

1,075

1,050

1,025

1,000

Korean won per U.S. dollar

PNC Forecast

Mexican Peso: 2014 has turned into another year of underwhelming growth for Mexico. While real GDP growth picked up in the second quarter to a 4.2 percent annualized increase on stronger construction output and continued strength in manufactured exports, labor market slack is substantial and is holding wage increases roughly even with inflation. The Bank of Mexico cut its growth forecast for 2014 in

May, then made a surprise 50 bps cut to its benchmark interbank rate to 3.0 percent on June 6. The Mexican rate cut was less a reaction to the domestic outlook than to the external environment: continued low interest rates, low capital market volatility, and ample liquidity for emerging markets. The

Mexican central bank will likely keep its interbank rate at a 3.0 percent premium to the Federal Funds Rate, in the base case making a first rate hike in the second half of 2015. Continued capital inflows, spurred by global investors’ eagerness to participate in Mexico’s energy sector reforms, will be reinforced by a stable rate premium paid on Mexican assets, likely supporting a modest trend appreciation of the peso vis-à-vis the U.S. dollar.

Pound Sterling: The pound briefly pushed above U.S. $1.70 at mid-year 2014 on Bank of England commentary that made clear that the U.K. would be the first major advanced economy to hike interest rates in 2015; PNC’s current forecast is for a

Bank Rate hike at the March 2015 Monetary Policy Committee

(MPC) meeting. After two MPC members voted for an immediate rate hike at the August 7 decision, a hike earlier in the first quarter also looks possible. Nevertheless, the pound plummeted in August on slower than expected wage growth and a dip in inflation to 1.6 percent. The pound’s August drop seems slightly overdone, especially with such strong evidence of a Bank Rate hike impending. Over the next few quarters, the pound is likely to average in the $1.65-$1.70 range it has established in 2014; the May 2015 parliamentary election may roil markets if the new government looks likely to follow through on current Prime Minister Cameron’s pledge to hold a referendum on Britain’s membership in the European Union.

14.50

14.25

14.00

13.75

13.50

13.25

13.00

12.75

12.50

12.25

12.00

11.75

1.75

1.70

1.65

1.60

1.55

1.50

1.45

Mexican pesos per U.S. dollar

U.S. dollars per

U.K. pound sterling

PNC Forecast

PNC Forecast

EXCHANGE RATE FORECASTS

Table and chart sources: Reserve Bank of Australia, Bank of Canada, China Foreign Exchange Trading

Center, Banco Central do Brasil, Bank of Japan, European Central Bank, Reserve Bank of India, Bank of Korea, Bank of England, CEIC, The PNC Financial Services Group

Visit http://www.pnc.com/economicreports to view the full listing of economic reports published by PNC’s economists.

Disclaimer: The material presented is of a general nature and does not constitute the provision of investment or economic advice to any person, or a recommendation to buy or sell any security or adopt any investment strategy. Opinions and forecasts expressed herein are subject to change without notice. Relevant information was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy. You should seek the advice of an investment professional to tailor a financial plan to your particular needs. © 2014 The PNC Financial Services Group, Inc. All rights reserved.