Foreclosure Laws - North Carolina Land Title Association

advertisement

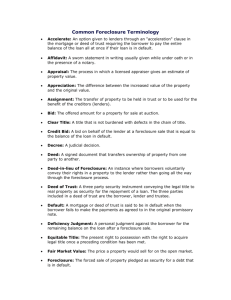

Foreclosure Laws: NC vs. SC Question How are mortgage liens treated? How are mortgages/deeds foreclosed? What are the legal instruments that establish a mortgage? How long does it take to foreclose a property? NC North Carolina is generally known as a title theory state where the property title remains in trust until payment in full occurs for the underlying loan. The document that secures the title is usually called a deed of trust and in North Carolina the mortgage serves the same purpose and generally contains the same terms as a deed of trust and serves the same function in a judicial foreclosure. The primary method of foreclosure in North Carolina involves what is known as non-judicial foreclosure. This type of foreclosure does not involve court action but requires notice commonly called a sale under the power of sale. When the mortgage is initially signed it will usually contain a provision called a power of sale clause which upon default allows an attorney to foreclose on the property in order to satisfy the underlying defaulted loan which is sometimes referred to as a bond. Because this is a non-judicial remedy there are very stringent notice requirements and the legal documents are required to contain the power of sale language in order to use this type of foreclosure method. In North Carolina, the lenders can also go to court in what is known as a judicial foreclosure proceeding where the court must issue a final judgment of foreclosure. This process is called foreclosure by action. The property is then sold as part of a publicly noticed sale by the sheriff. A complaint is filed in court along with what is known a lis pendens. A lis pendens is a recorded document that provides public notice that the property is being foreclosed upon. The documents are known as the mortgage or in a commercial transaction, a security agreement. Sometimes the mortgage document is combined with the security agreement. A mortgage is filed to evidence the underlying debt and terms of repayment, which is set forth in the note. Depending on the timing of the various required notices, it usually takes approximately 90-120 days to effectuate an uncontested nonjudicial foreclosure. This process may be delayed if the borrower contests the action in court, seeks delays and adjournments of sales, or files for bankruptcy. SC South Carolina is known as a lien theory state where the property acts as security for the underlying loan. The document that places the lien on the property is called a mortgage. In South Carolina, the lenders go to court in what is known as a judicial foreclosure proceeding where the court must issue a final judgment of foreclosure. The property is then sold as part of a publicly noticed sale. The court with jurisdiction over a foreclosure is known as the Circuit Court. A complaint is filed in court along with a lis pendens. Same as NC Depending on the court schedule, it usually takes approximately 150180 days to effectuate an uncontested foreclosure. This process may be delayed if the borrower contests the action, seeks delays and adjournments of hearings, or files for bankruptcy. Borrowers must receive a notice of sale which must be published for at least three (3) consecutive weeks in a newspaper of general circulation. This notice includes posting at the courthouse and other locations at least three (3) weeks before the sale. South Carolina has a process called an Is there a right of redemption? Are deficiency judgments permitted? What statutes govern foreclosures? Yes. North Carolina has a very short statutory right of redemption, which would allow a party whose property has been foreclosed to reclaim that property by making payment in full of the sum of the unpaid loan plus costs within ten (10) days of the sale through the upset bid process, where any bidder can increase the sale bid by 5% in order to become the winning bidder at the sale. Yes. A deficiency judgment may be obtained when a property in foreclosure is sold at a public sale for less than the loan amount which the underlying mortgage secures. Deficiency judgments are referenced in North Carolina General Statutes, Chapter 45, Article 2B §45-21.36 and the mortgagor has the right to prove the fair value of the property as a defense to any deficiency based on the sale price. The laws that govern North Carolina non-judicial foreclosures are found in North Carolina General Statutes, Chapter 45 (Mortgages and Deeds of Trust), Article 2, Article 2A as referenced in §45-4 to §4521.38 application for an order of appraisal. A borrower usually requests this process where an independent appraiser determines the high value of the property which may be substituted for the sale amount if the lender is seeking a deficiency. Unless the property is a residence or the subject of a consumer credit transaction these appraisal rights may be waived. No. South Carolina does not have a statutory right of redemption, which allows a party whose property has been foreclosed to reclaim that property by making payment in full of the sum of the unpaid loan plus costs. Yes. A deficiency judgment may be obtained when a property in foreclosure is sold at a public sale for less than the loan amount which the underlying mortgage secures. This means that the borrower still owes the lender for the difference between what the property sold for at auction and the amount of the original loan. Deficiency judgments are subject to appraisal rights as noted above. The laws that govern South Carolina foreclosures are found in South Carolina Code of Laws (2004) Title 29 (Mortgages and Other Liens), Chapter 3, Article 7 (Foreclosures) (Section 29-3-610 et. seq.).