Becker CPA Review - Becker Professional Education

advertisement

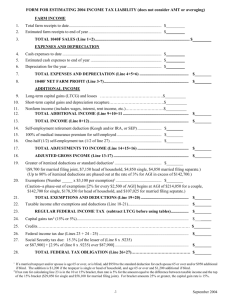

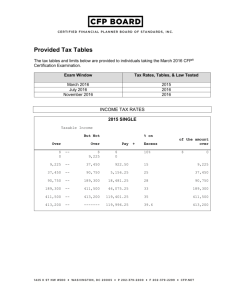

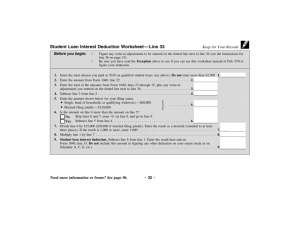

Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition Note to Students: The items listed below are updates to your materials for the IRS amounts applicable to 2013. CPA Exam questions generally do not focus on concepts and amounts that are specific to an individual tax year, but instead focus on the broader concepts and calculations. However, these updates have been provided so that you have the most current information. Page and Item Number Update R1 Individual Tax–Income R1-4, Exemption amount at the bottom of the page. R1-10,Item I. R1-11, Item II. R1-12, Item B.2. For 2013, the personal exemption amount is $3,900. R1-7, Item I.A.2.B. For 2013, the gross income amount referenced here is $1,000. R1-10, Item I. R1-12, Item B.2. Personal Exemption Phase-out returns in 2013. The phase-out starts when AGI exceeds $300,000 for married filing jointly and surviving spouses, $275,000 for heads of households, $250,000 for single taxpayers, and $150,000 for married filing separately. The personal exemption is reduced by 2% for every $2,500 or portion thereof (2% for each $1,250 for married couples filing separately) by which the taxpayer’s AGI exceeds the previously mentioned amounts. R1-19, Item g.(3) The value of employer provided parking is $245 per month for 2013. R1-19, Item g.(4) The value of employer provided transit passes is $245 per month for 2013. R1-20, Item i.(1) The maximum contribution to an FSA for 2013 is $2,500. R1-22, Item 2.c.(2) For 2013, the phase-out begins at $74,700 for single and head of household and $112,050 for married filing jointly. 1 Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition The basic standard deduction for a child is $1,000 in 2013. All amounts in this line that read $950 should be $1,000 for 2013. Also the items that read $1,900 should be $2,000 for 2013. The tax brackets for 2013 for a child's unearned income are: R1-22 and R1-23, Item 3. $0 - $1,000 $1,001 - $2,000 $2,001 and over 0% Child's rate Parent's rate The qualified dividend rate and capital gains rate for most taxpayers is still 15% for 2013. But for certain high income taxpayers, it is increased to 20%. R1-24, Item a.(2)(c) and R1-69, Item E.1.a.(2) Starting in 2013, certain unearned income is subject to a new 3.8% Medicare Tax. The tax is levied on the lesser of (1) the taxpayer's net investment income, or (2) the excess of MAGI for the tax year over the threshold amount of $200,000 ($250,000 for married filing jointly, and $125,000 for married filing separate). MAGI is a taxpayer's AGI adjusted for certain foreign income exclusions. (Add in the blank space at the bottom of page R1-24.) R1-24, New Item 3. R1-28, Item 2.e. For 2013, the standard mileage rate is 56.5 cents per mile. R1-29, Item 4.a.(2)(a) and (c) The Social Security Wage Base increased to $113,700 in 2013. R1-40, Item c.(3) The exception for medical expenses is amounts in excess of 10% of AGI for most taxpayers starting in 2013. R1-47, Item P.7. For 2013, the amount excludable from income goes to $97.600. R2 Individual Tax–Adjustments, Deductions and Credits R2-3, Item II.A. and R2-11, Item E. The Tuition and Fee Deduction has been extended through 12/31/13. R2-4, Item B. The Educator Expenses Deduction has been extended through 12/31/13. R2-5, Item c.(1) For 2013, the phase-out for Single/HH is $59,000-$69,000 and Joint is $95,000-$115,000. 2 Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition R2-5, Item c.(2)(b) For 2013, the phase-out for an individual who is not an active participant in an employer sponsored retirement plan, but whose spouse is, increases to $178,000-$188,000. R2-6, Item d.(1) and (2) For 2013, the maximum IRA deduction has increased to $5,500 for a single taxpayer and $11,000 for married taxpayers. For 2013, the phase-out for Joint is $95,000-$115,000. R2-6, Notes on bottom of page For 2013, the phase-out for an individual who is not an active participant in an employer sponsored retirement plan, but whose spouse is, increases to $178,000-$188,000. R2-7, Item d. For 2013, the Roth IRA contribution limits have increased to $5,500 for a single taxpayer and $11,000 for married taxpayers. R2-7, Item 3.e. The 2013 phase-out for Roth Contributions increases to $112,000$127,000 for Single and HH, and $178,000-$188,000 for Joint filers. R2-8, Item 4.a.(1) For 2013, the Non-Deductible IRA contribution limit increases to $5,500. R2-10, Item D.2. The 2013 phase-out for student loan interest for joint filers changes to $110,000-$140,000. Single filers changes to $55,000-$70,000. R2-11, Item F.1. For 2013, pre-tax contributions increase to $3,250 ($6,450 for families). R2-11, Item F.3. For 2013, a high deductible plan must have at least a $1,250 deductible ($2,500 for families). R2-12, Item F.3.a. For 2013, the out of pocket limitation is $6,250 for individuals and $12,500 for families. R2-12, Item 4.c. For 2013, $3,100 goes to $3,200 and $6,300 goes to $6,450. R2-12, Item 4.d. For 2013, $2,100 goes to $2,150, both $4,200 numbers go to $4,300, and $7,650 goes to $7,850. R2-13, Item 3.a.(1) For 2013, the standard moving mileage rate is 24 cents per mile. 3 Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition R2-13, Item J.1. For 2013, the $50,000 deductible amount increases to $51,000. R2-14, Item J.2. For 2013, the $50,000 additional amount above the deductible amount increases to $51,000. R2-16, Item III.A. For 2013, the standard deduction for single goes to $6,100, Head of Household $8,950, Married filing joint $12,200, and Married filing separately $6,100. R2-17, Item B.1. Itemized Deduction Phase-out returns in 2013. The phase-out starts when AGI exceeds $300,000 for married filing jointly and surviving spouses, $275,000 for heads of households, $250,000 for single taxpayers, and $150,000 for married filing separately. The itemized deductions are reduced by 3% of the amount which the taxpayer’s AGI exceeds the previously mentioned amounts. The itemized deductions may not be reduced below 80% of the amount allowed before the phaseout. R2-20, Item c. and R2-21, Item g. For 2013, the medical expense AGI limitation has been increased to 10% of AGI. However, it remains at 7.5% of AGI for any individual who is age 65 or over. R2-20, Item d.(5)(b) For 2013, the standard medical mileage rate is 24 cents per mile. R2-22, Item (4) The sales tax deduction has been extended through 2013. R2-23, Item (3) The mortgage insurance premium deduction has been extended through 2013. R2-29, Item (2) For 2013, the standard mileage rate is 56.5 cents per mile. R2-39, Item D.1. All amounts indicated for 2011 and 2013 remain unchanged for 2013. R2-40, Item II.D.2.e. For 2013, the credit phase-out begins with MAGI exceeding $53,000 ($107,000 on a joint return), with full phase-out at $63,000 ($127,000 for joint returns). R2-41, Item F.1. The adoption credit goes to $12,970 for 2013. 4 Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition R2-41, Item F.2. For 2013, the phase-out for the adoption credit goes to $194,580$234,580. R2-42, Item 3.d. For adoption assisted programs the 2013 amount goes from $12,650 to $12,970 and the phase-out goes to $194,580-$234,580. R2-42, Item 5. The credit for 2013 is $12,970. R2-46, Item 4.a. For 2013, the maximum credit is $487. R2-46, Item 4.b. For 2013, the maximum credit is $3,250. R2-46, Item 4.c. For 2013, the maximum credit is $5,372. R2-46, Item 4.d. For 2013, the maximum credit is $6,044. R2-46, Item 5. For 2013, the disqualified income amount is $3,300. R2-48, Item R. For 2013, Residential energy credits have been extended. R2-52, Item B. For 2013, the exemption amounts are $80,800 for married filing jointly, $51,900 for single, and $40,400 for married filing separately. For 2013, the phase-out thresholds start at $153,900 for married filing jointly, $115,400 for single, and $76,950 for married filing separately. R2-54, Item G. The reduction of AMT liability by the full amount of nonrefundable personal tax credits has been extended permanently. 5 Becker CPA Review Regulation Course Textbook and Lecture Tax Update 2013 Exam Edition R3 C Corporation and S Corporation Taxation Item C. Expense Deduction in Lieu of Depreciation (Section 179) covers the 2012 and 2013 Section 179 rules prior to the American Taxpayer Relief Act of 2012. The following covers the rules in effect after the passage of the act: For tax years 2012 and 2013, the taxpayer can expense up to $500,000 of the cost of qualifying property. This maximum expensing amount is reduced dollar for dollar if the taxpayer purchases and places in service during the year more than $2,000,000 of qualifying property. R3-28, Item C. Bonus depreciation is extended through 2013. The depreciation rate is 50% for assets placed in service before September 9, 2010. The rate is increased from 50% to 100% (full write-off) for new, qualified assets acquired and placed in service after September 8, 2010, and before January 10, 2012. The depreciation rate is 50% for assets placed in service after December 31, 2011, and before January 1, 2014. The $8,000 additional first-year depreciation for vehicles on which bonus depreciation has been claimed continues through 2013. Bonus depreciation is not an adjustment for, or a preference for, AMT purposes. Bonus depreciation is claimed after the depreciation expense deduction. The 100% exclusion for qualified small business stock has been extended for stock acquired through December 31, 2013. R3-51, Item E. R4 Partnership Taxation, Estate & Gift Taxation, and Additional Tax Topics R4-22, Items D.1.c. and D.2.b. R4-30, Item III.A. R4-31, Bottom of chart R4-33, Items E.1., E.2., & E.3. R4-38, Item V. For 2013, the "applicable exclusion amount" increases from $5,120,000 to $5,250,000. This amount provides for a unified estate and gift tax credit of $2,045,800 for 2013. R4-35, Item IV. and R4-38, Item G. For 2013, the per-year-per-donee exclusion increases to $14,000 per done and $28,000 for married couples who elect gift splitting. R4-38, Item V. With respect to the generation-skipping transfer tax, the maximum total exemption for married couples is $10,500,000 for 2013. 6