Page 1 of 1

Gleim CMA Review

Updates to Part 1

16th Edition, 1st Printing

February 2013

NOTE: Text that should be deleted from the outline is displayed with a line through the text.

New text is shown with a blue background.

Study Unit 1 – Ethics for Management Accountants and Cost Management Concepts

Page 32, Subunit 1.6, 3.c.: This edit clarifies allocation of manufacturing costs using activity-based

costing.

c. Activity-based costing (ABC) attaches costs to activities rather than to physical goods first

assigns resource costs to activities. These activity costs are then assigned to physical

goods.

1) ABC is a response to the distortions of product cost information brought about by

peanut-butter costing, which is the inaccurate averaging or spreading of costs like

peanut butter over products or service units that use different amounts of resources.

a) A major cause of the problems associated with peanut-butter costing is the

significant increase in indirect costs brought about by the increasing use of

technology.

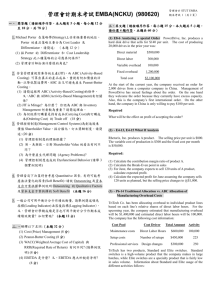

Study Unit 7 – Cost and Variance Measures

Page 267, Subunit 7.6, 2.3): This edit removes the word “efficiency” from the total.

Variable Overhead Variances

Static budget variable overhead

Flexible budget variable overhead

Actual variable overhead

Units

18,000

16,500

16,500

Machine

Hours

1.2

1.2

1.3

Variable overhead spending variance

AQ × (AP − SP)*

Variable overhead efficiency variance

SP × (AQ − SQ)**

Total variable overhead efficiency variances

Actual

Quantity

21,600

19,800

21,450

Rate

$ 8.00

$ 8.00

$10.00

Total

$172,800

$158,400

$214,500

$42,900 U

13,200 U

$56,100 U

*21,450 × ($10 − $8)

**$8 × (21,450 − 19,800)

Page 273, Subunit 7.8: This update corrects the multiple-choice question numbers for Study Unit 7.8.

Stop and review! You have completed the outline for this subunit. Study multiple-choice

questions 84 through 99 beginning 37 and 38 on page 288.

Copyright © 2013 Gleim Publications, Inc. and/or Gleim Internet, Inc. All rights reserved. Duplication prohibited. www.gleim.com